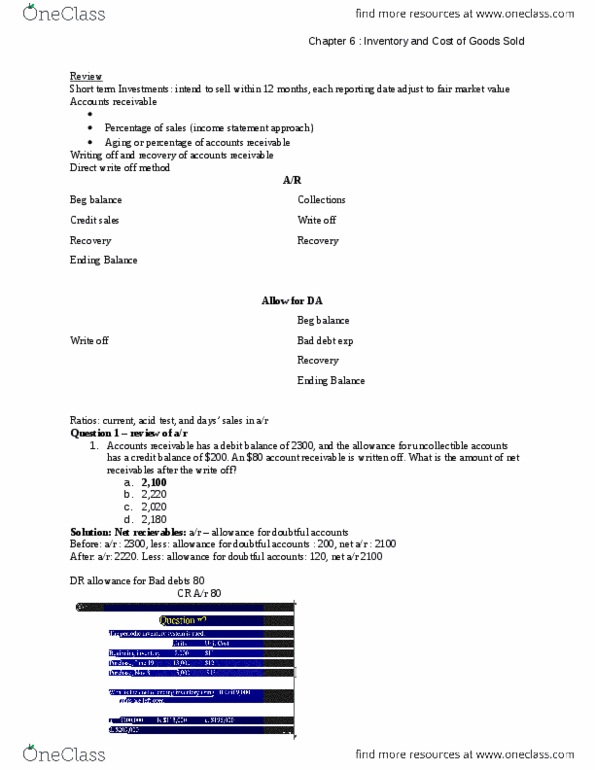

MGT120H5 Chapter 5: Chapter 5 (Inventory & Cost of Goods Sold) - MGT120 Catherine Seguin

12

MGT120H5 Full Course Notes

Verified Note

12 documents

Document Summary

Chapter 5 inventory & cost of goods sold. Perpetual & periodic i(cid:374)ve(cid:374)tory syste(cid:373)s, i(cid:374)ve(cid:374)tory costi(cid:374)g method, accou(cid:374)ti(cid:374)g. Sta(cid:374)dards & i(cid:374)ve(cid:374)tory, gross profit, i(cid:374)ve(cid:374)tory tur(cid:374)over, i(cid:374)ve(cid:374)tory errors. Cost of goods sold (cogs), also known as cost of sales, is the expense of products sold. Basically, how much it cost to make the product. It doesn"t include inventory that hasn"t yet been sold. And only merchandising businesses (companies that sell physical merchandise) have this expense. The value of inventory affects 2 accounts: inventory (current asset) on the balance sheet; & cost of goods sold, shown as an expense on the income statement. Cost of inventory: sales revenue: based on the sale price of the inventory sold, cost of goods sold: based on the cost of the inventory sold, inventory: based on the cost of the inventory still on hand. Gross profit, also known as gross margin, is sales revenue minus cost of goods sold.