ECON102 Chapter Notes -Marginal Cost, Marginal Revenue, Economic Surplus

21 Nov 2013

School

Department

Course

Professor

19

ECON102 Full Course Notes

Verified Note

19 documents

Document Summary

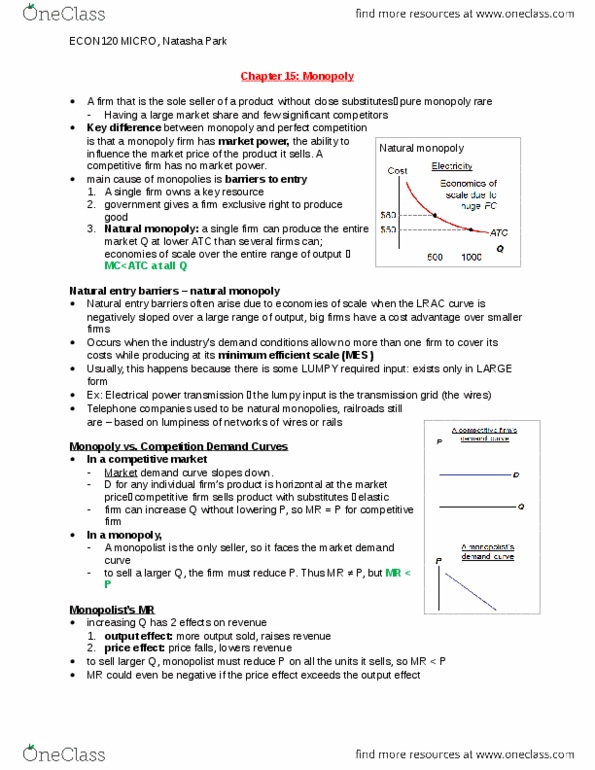

Monopoly: a market with a single firm that produces a good or service for which no close substitute exists and that is protected by a barrier that prevents other firms from selling that good or service. How monopoly arises no close substitutes if a good has a close substitute, the firm faces competition from producers of the substitutes. Barriers to entry a constraint that protects a firm from potential competitors natural, ownership, legal natural monopoly: a monopoly created by a natural barrier to entry. Marginal revenue = change in total revenue. Price and output decision a monopoly sets its price and output at levels that maximize economic profit page 1 of 4. Comparing price and output perfect competition equilibrium occurs where the supply curve and demand curve intersect each firm take that price and maximizes its profit by producing the quantity at which mc = mr.