COMM321 Chapter Notes - Chapter 8: Perpetual Inventory, Retained Earnings, Gross Profit

16 Apr 2017

School

Department

Course

Professor

Document Summary

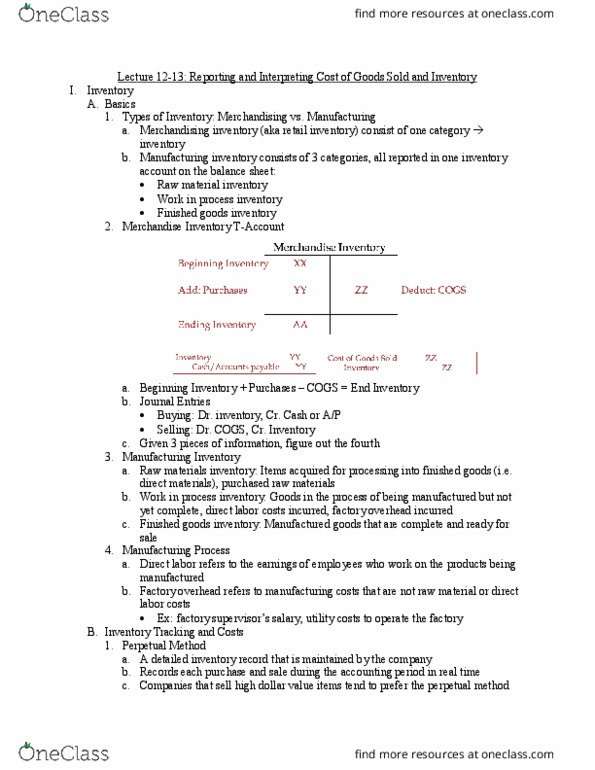

Inventory system: perpetual vs. periodic, inventory issues: How to distinguish between costs included in i/s and costs included in b/s? (i. e. , what cost formula should be used?: impact of errors in inventory. Purchases and sales of inventory, freight, purchase returns or discounts recorded directly to. Cost of goods sold (cogs) is debited and inventory is credited for each sale. Periodic inventory counts still required to ensure reliability. Any differences in counted and recorded quantities are posted to a separate account . Inventory over and short (or may be recorded as an adjustment to cost of goods sold) Inventory purchases recorded as a debit to purchases account. Freight, purchase returns and discounts are recorded in separate accounts. The quantity and cost of inventory on hand is determined by taking a physical inventory count. Cost of goods sold is determined at the end of the period. The inventory account remains unchanged during the year.