ARBUS102 Chapter Notes - Chapter 12: Retained Earnings, International Financial Reporting Standards, Accrual

16 Feb 2017

School

Department

Course

Professor

Document Summary

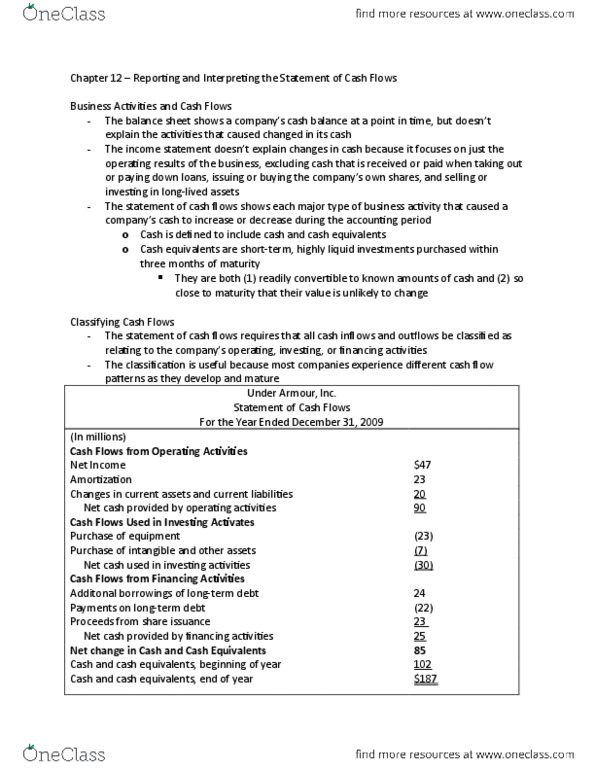

Accrual accounting: reports revenues when they are earned and expenses when they are incurred. Both require every company to report a statement of cash flows. The statement of cash flows shows each type of business activity that caused a company"s cash to increase or decrease during the accounting period. Cash equivalents are short-term, high liquidity investments purchased within three months of maturity. They are considered equivalent to cash because they are both 1) readily convertible to known amounts of cash and 2) so close to maturity that their value is unlikely to change. The statement of cash flows requires that all cash inflows and outflows be classified as relating to the company"s operating, investing, or financing activities. The classification of cash flows is useful because most companies experience different cash flow patterns as they develop and mature. Cash flows from operating activities: cash inflows and outflows related to components of net income.