AFM391 Chapter Notes - Chapter 13: Book Value, Operating Expense, Retained Earnings

8 Dec 2017

School

Department

Course

Professor

Document Summary

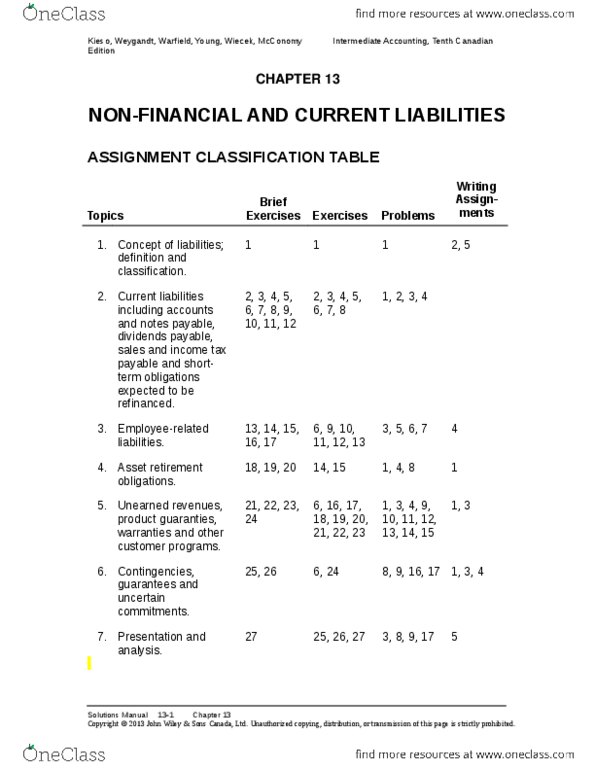

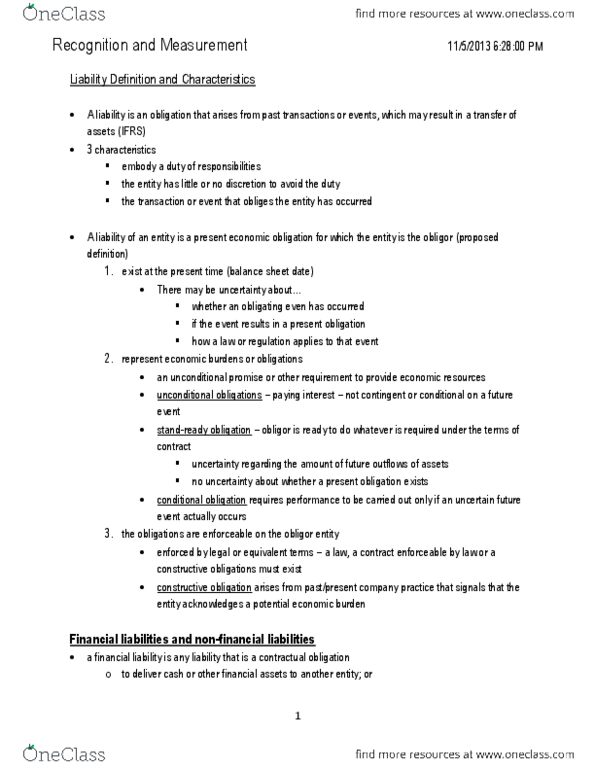

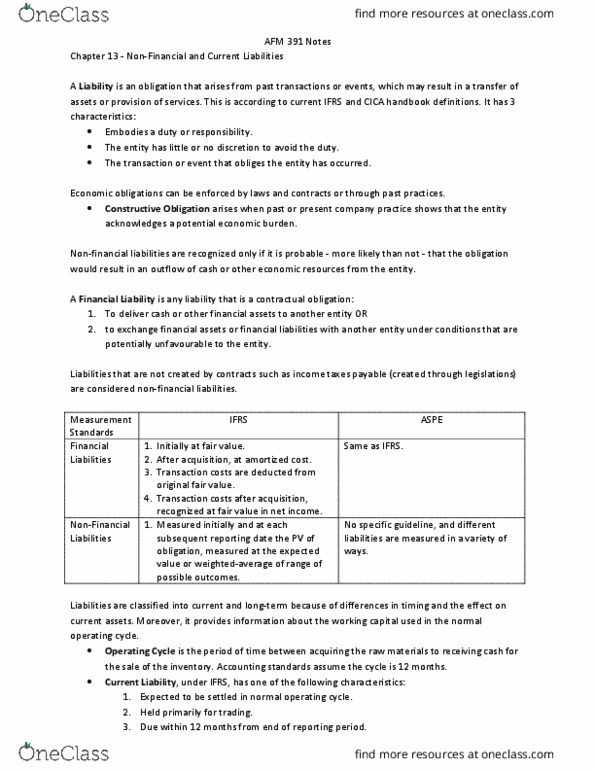

Afm 391 chapter 13: non-financial and current liabilities. Under recognition requirements, non-financial liabilities recognized only if probable that obligation results in outflow of cash or resources. Financial liabilities: are recognized initially at fv, then at amortized cost, short-term liabilities usually accounted for at maturity value (fv & maturity not big difference) Non-financial liabilities: aspe does not separately address non-financial liabilities, so measured in various ways. Ifrs measured initially and at each subsequent reporting date at best estimate of amount the entity would rationally pay at date of statement of financial position to settle present obligation. Common periods for extended credit are 30 to 60 days long. Non-interest-bearing note issued: borrower receives present value of note and pays back larger maturity. Long-term indebtedness that matures within 12 months from statement of financial position are current liabilities: only the maturing potion of principal of ltd is reported as current liability.