AFM291 Chapter Notes - Chapter 5: Bank Reconciliation, Cash Flow, Accounts Payable

10 Oct 2018

School

Department

Course

Professor

Document Summary

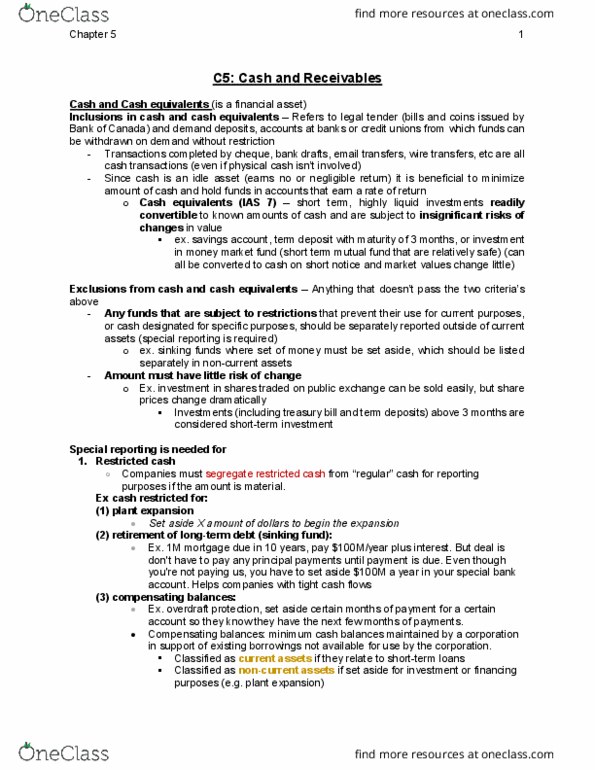

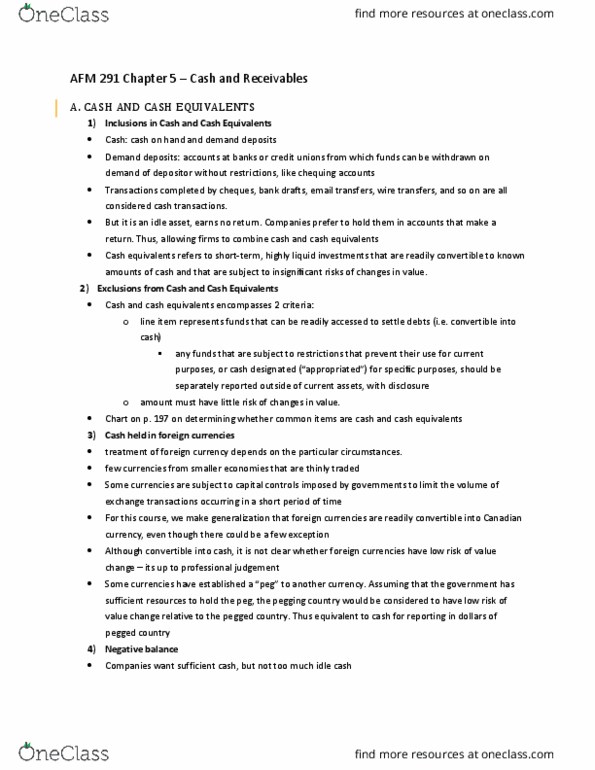

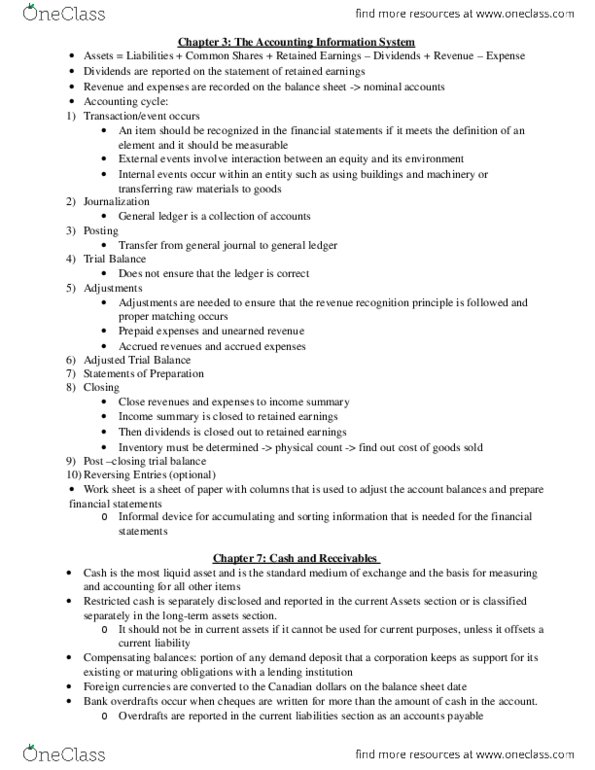

Subject to insignificant risks of change in value: e. g. savings account, term deposit with maturity of three months or less, two criteria. Funds that are readily accessed to settle debts: no restrictions on purpose. Little risk of changes in value: exclusions, cash designated for a specific purpose. Bank reconciliation: ties the amount of cash according to a company"s records and the amount according to the bank that holds its funds, reasons to prepare a bank reconciliation, understand why the two sets of records differ. Identify bookkeeping errors by either entity: contribute to internal control over cash, two steps, begin with the bank balance and adjust for reconciling items to arrive at the corrected cash balance. Add deposits in transit, subtract cheques: begin with the company"s balances and adjust for reconciling items to arrive at the corrected cash balance. Transactions that affect cash that have not yet been recorded by the reporting entity.