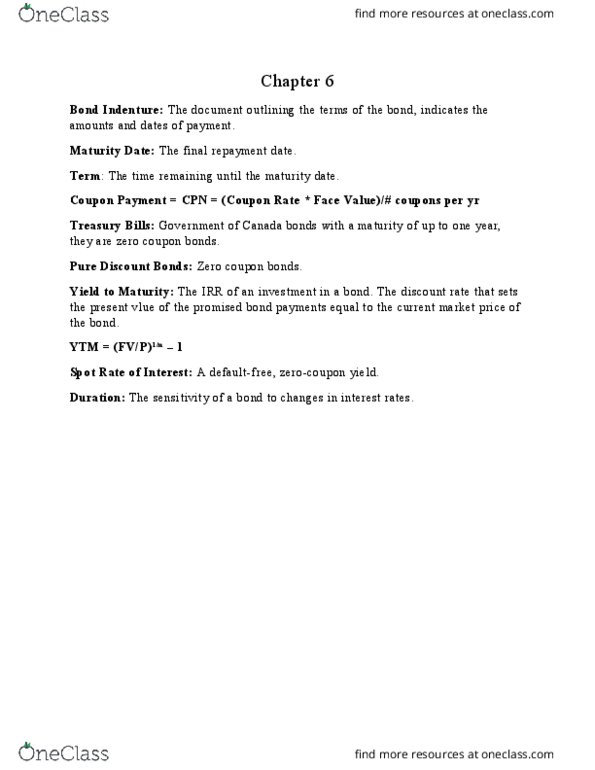

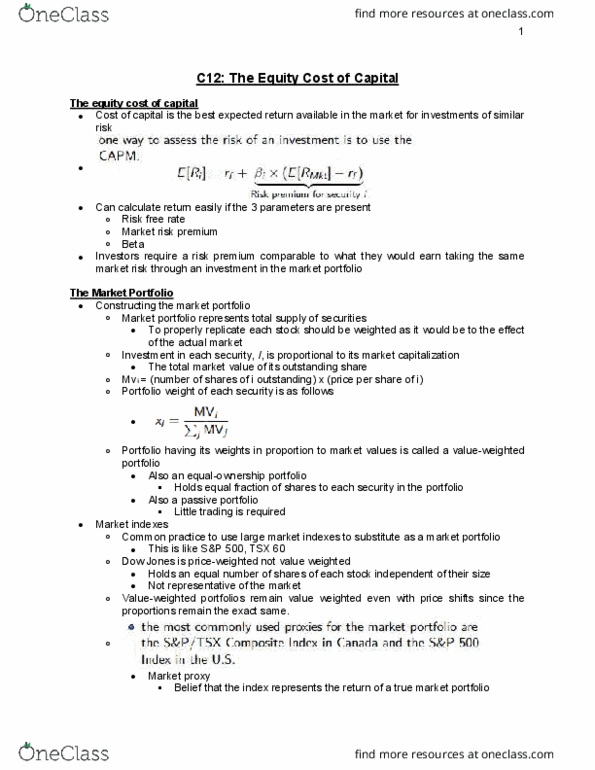

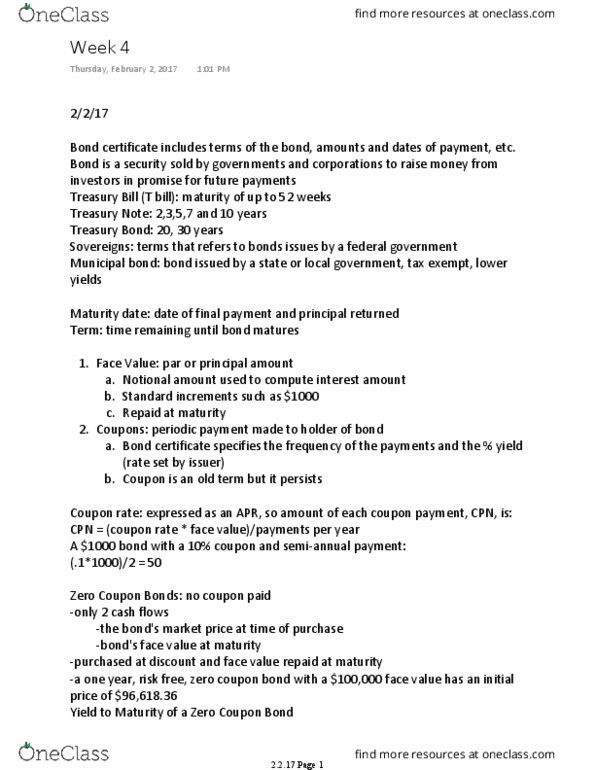

AFM273 Chapter Notes - Chapter 6: Spot Contract, Ytn, Cash Flow

47 views4 pages

13 Oct 2018

School

Department

Course

Professor

Document Summary

Face value (principle): amount used to compute coupon payments: repaid at maturity, usually a denomination of increments. Zero-coupon bonds: does not make coupon payments, treasury bills. Irr of the bond: (cid:1839)= (cid:4672)(cid:4673)(cid:3117) (cid:883, (cid:1870)(cid:3041)=(cid:1839)(cid:3041) If you purchased the bond for . 14 and sold it for . 53 five years later, the irr is. Discounts and premiums: coupon bonds may trade at, par (price equal to their face value, coupon rate is equal to yield to maturity, discount (price less than the face value) Investor earns a return on both receiving the coupons and receiving a face value that exceeds the price paid for the bond: yield to maturity exceeds coupon rate, premium (price greater than their face value) Investor"s return from the coupons is diminished by receiving a face value less than the price paid: yield to maturity is less than the coupon rate.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers