AFM102 Chapter 5: C5 Job-Order Costing Process Costing

30 Jan 2016

School

Department

Course

Professor

Document Summary

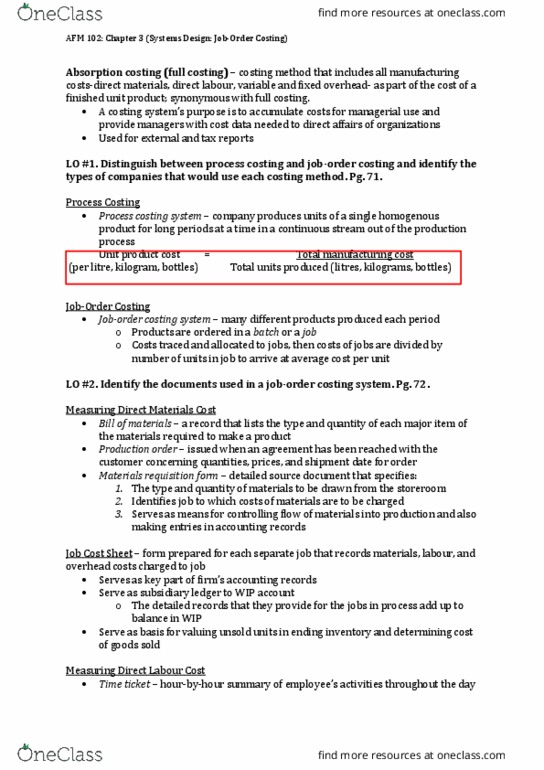

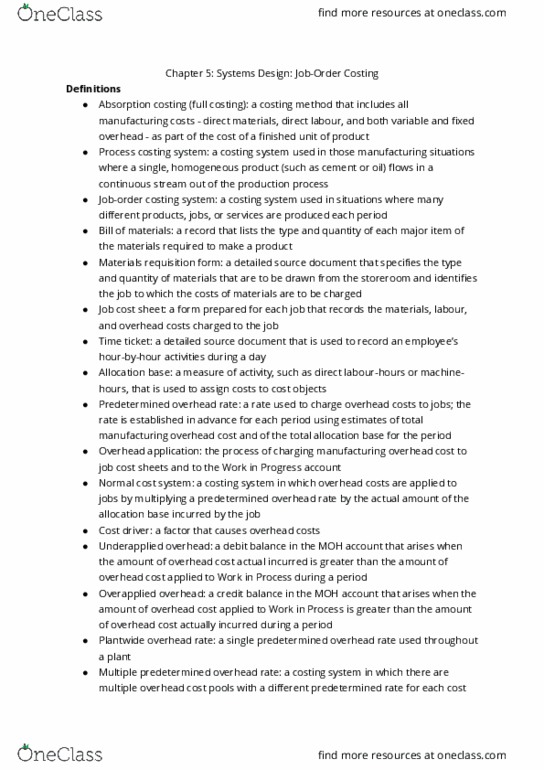

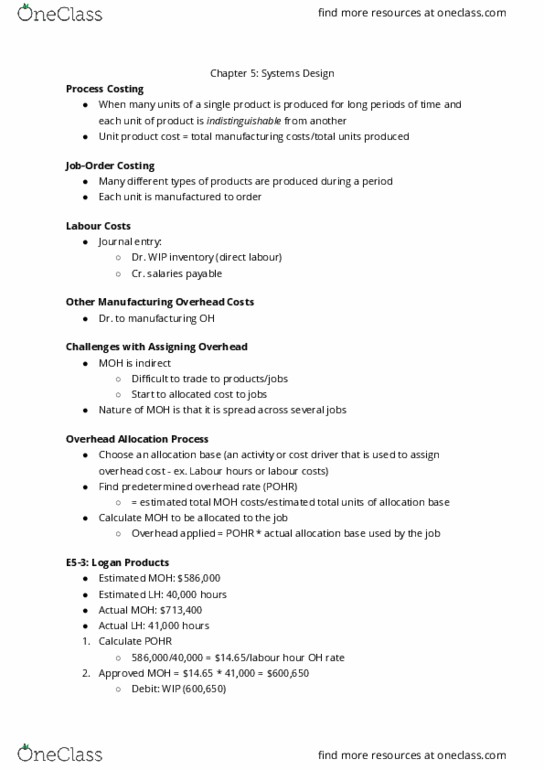

Absorption costing (full costing): all manufacturing costs, fixed and variable, are assigned to units of product. Process costing system: used in situations where the company produces many units of a single product for long periods at a time and each product is indistinguishable from another. Homogenous product that flows evenly through the production process on a continuous basis. Accumulate costs in particular operation for an entire period (total moh), then divide total cost by the number of units produced during the period. Total units measured in litres, km, bottles: job-order costing. Job-order costing system: situations where many different g/s are produced each period. Ex. different jeans for men and women, broadcasts of sporting events. Costs are traced and allocated to jobs, and then the costs of the jobs are divided by the number of units in the job. Documents for a job order costing: sales order, production order, job cost sheet.