AFM101 Chapter Notes - Chapter 8: Liquid Oxygen, Perpetual Inventory, Financial Statement

7 Jun 2018

School

Department

Course

Professor

AFSA Education

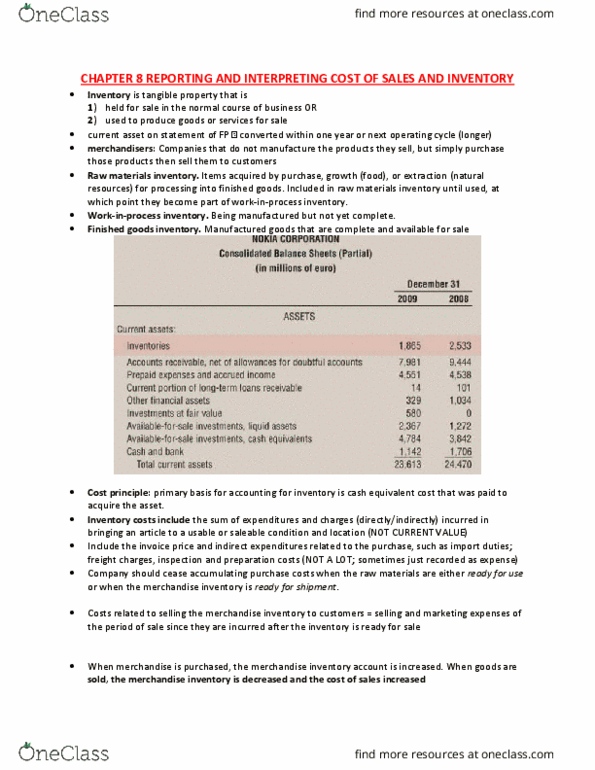

(4) COST OF SALES

Cost of Sales (COS) directly related to Sales Revenue.

o Sales Revenue = [# of units sold] * [sale price].

o Cost of sales = [# of units sold] * [unit costs OR cost per unit].

Includes all costs of the merchandise purchased of the finished goods sold

during the period.

Inventory (Balance Sheet) and Cost of Sales (Statement of Earnings):

o BI = Beginning inventory; stock of finished goods inventory.

o P = New purchases that are added to inventory.

o Cost of goods available for sale = [cost of BI] + [cost of purchases (or additions

to finished goods) for the period].

o EI = Ending inventory; what remains unsold at the end of the period ending

inventory of finished goods is reported on the Statement of Financial Position.

EI for one accounting period is the BI for the next accounting period.

o Cost of sales = portion of cost of goods available for sale that are actually sold

becomes the Cost of Sales on the Statement of Earnings.

o Cost of Sales Equation: BI + P – EI = COS.

o Cost of goods available for sale Equation: BI + P = COG available for sale.

o Example: Merchandise inventory T-Account.

LO2 Compare methods for controlling and keeping track of inventory, and analyze the effects of

inventory error on the financial statements.

(1) INTERNAL CONTROL OF INVENTORY

Inventory 2nd most vulnerable to theft, after cash.

Efficient management of inventory to avoid (1) cost of stock-outs & (2) overstock

situations.

Controls to safeguard inventories:

1. Separation of responsibilities (inventory accounting & physical handling).

2. Storage of inventory protect from theft & damage.

3. Limit access to inventory to authorized employees.

4. Maintaining perpetual inventory records.

5. Comparing perpetual records to periodic physical counts of inventory.

(2) PERPETUAL & PERIODIC INVENTORY SYSTEMS

Amounts of COS and EI can be determined using 2 different inventory systems:

(a) PERPETUAL

Detailed inventory record is maintained, recording each purchase and sale during the

accounting period.

Maintained through a transaction-by-transaction basis.

Gives Cost of EI and COS at any point in time.

Purchase transactions are directly recorded in an inventory account.

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

Cost of sales (cos) directly related to sales revenue: sales revenue = [# of units sold] * [sale price], cost of sales = [# of units sold] * [unit costs or cost per unit]. Includes all costs of the merchandise purchased of the finished goods sold during the period. Lo2 compare methods for controlling and keeping track of inventory, and analyze the effects of inventory error on the financial statements. (1) internal control of inventory. Inventory 2nd most vulnerable to theft, after cash. Efficient management of inventory to avoid (1) cost of stock-outs & (2) overstock situations. Amounts of cos and ei can be determined using 2 different inventory systems: (a) perpetual. Detailed inventory record is maintained, recording each purchase and sale during the accounting period. Gives cost of ei and cos at any point in time.