AFM101 Chapter Notes - Chapter 9: Cash Flow, The Purchase Price, Title Insurance

6 Dec 2016

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

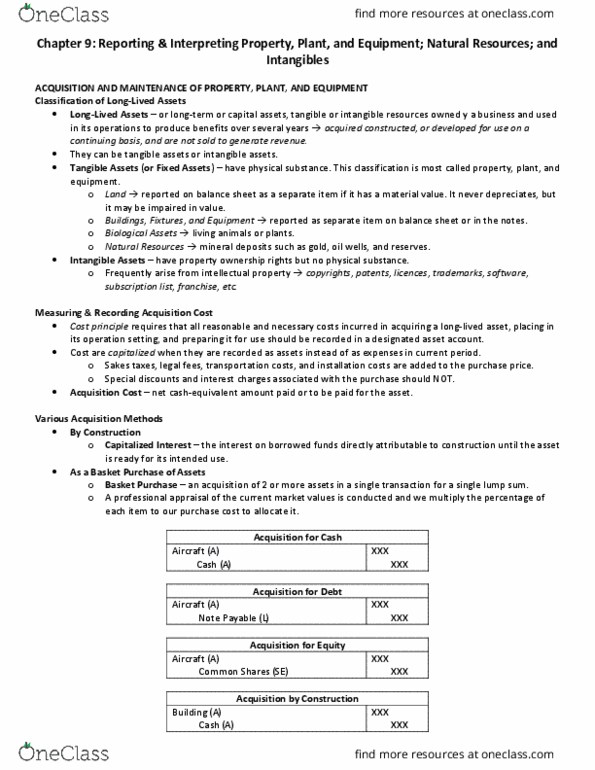

Chapter 9: reporting and interpreting property, plant, and equipment; natural. Long-lived (or long-term or capital) assets: tangible or intangible resources owned by a business and used in its operations to produce benefits over several years. Capitalized interest: represents interest on borrowed funds directly attributable to construction until the asset is ready for its intended use. Basket purchase: an acquisition of two or more assets in a single transaction for a single lump sum. Ordinary repairs and maintenance: expenditures for normal operating upkeep of long-lived assets. Revenue expenditures: maintain the productive capacity of the asset during the current accounting period only and are recorded as expenses. Extraordinary repairs: infrequent expenditures that increase the asset"s economic usefulness in the future. Betterments: costs incurred to enhance the productive or service potential of a long-lived asset. Capital expenditures: increase the productive life, operating efficiency, or capacity of the asset and are recorded as increases in asset accounts, not as expenses.