AFM101 Chapter 4: Adjustments, Financial Statements, and Quality of Earnings

25 Oct 2016

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

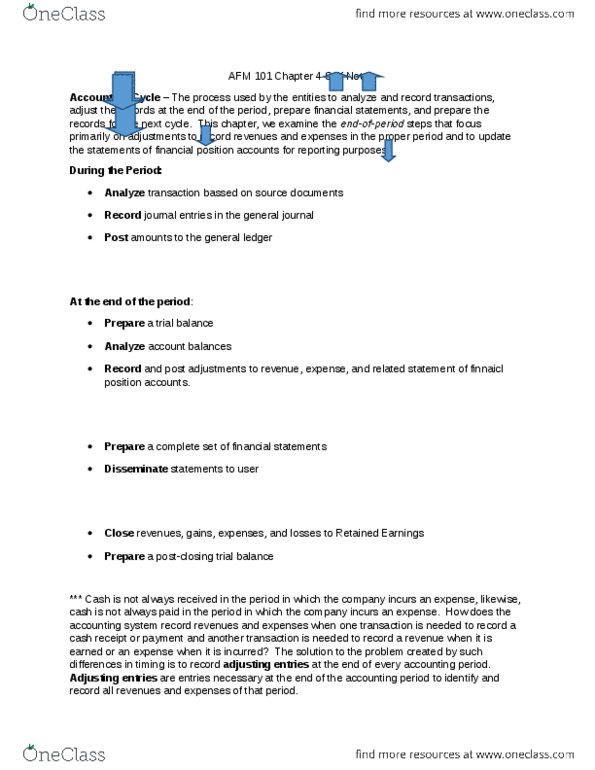

Chapter 4: adjustments, financial statements, and the quality of earnings. Accounting cycle the process used by entities to analyze and record transactions, adjust the records at the end of the period, prepare financial statements, and prepare the records for the next cycle. Record journal entries in the general journal. Prepare a complete set of financial statements. Close revenues, gains, expenses, and losses to retained earnings. Cash it not always received/paid in the period where the company earns revenue or incurs expenses. Adjusting entries entries necessary at the end of the accounting period to identify and record all revenues and expenses of that period. Companies wait until the end of the accounting period to adjust their accounts because adjusting the records daily would be costly & time-consuming. Required every time a company wants to prepare financial statements for external users. Cash is never adjusted adjusting journal entry involves a balance sheet & an income statement account.