ACTSC371 Chapter Notes - Chapter 7: Risk Premium, Market Risk, Market Portfolio

14 Apr 2016

School

Department

Course

Professor

Document Summary

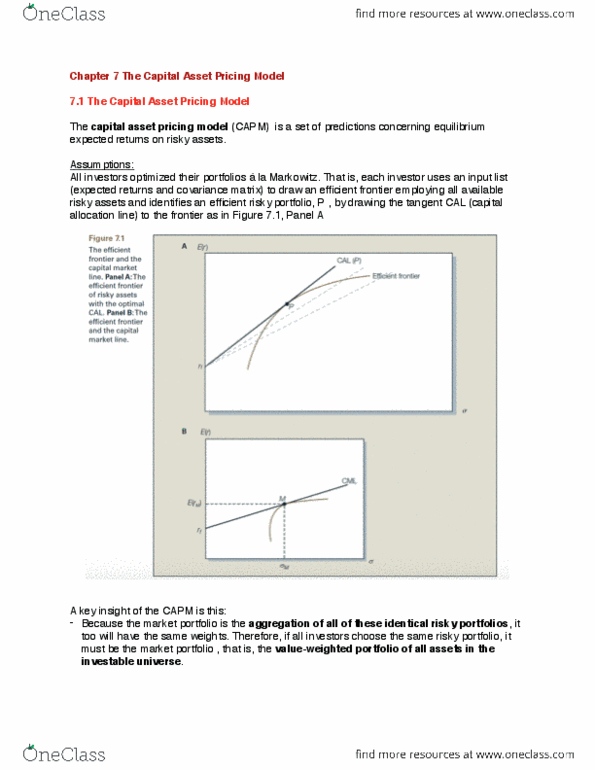

Capital asset pricing model (capm: set of predicions concerning equilibrium expected returns on risky assets, equilibrium model that underlies all modern inancial theory. We look at it in staionary way. We all setle on what"s best: derived using principles of diversiicaion with simpliied assumpions, markowitz, lintner and mossin are researchers credited with its development. We all have the same data: same risk free rate, tangent cal and risky porfolio, market porfolio is aggregaion of all risky porfolios and has same weights. Market porfolio is a construct not real. How much to put in risky assets compared to risk free assets. Not stable because market cap changes, etc. The passive strategy is eicient: someimes call this result a mutual fund theorem. Slope and market risk premium: m = the market porfolio, rf = risk free rate, e(rm) rf = market risk premium, (e(rm) rf)/sigmam = slope of the cml. The eicient fronier and the capital market line.