ACTSC231 Chapter 8: Chapter_8_solutions_-_Theory_and_Practice20120913_5051d355e96ee.pdf

23 Feb 2015

School

Department

Course

Professor

Document Summary

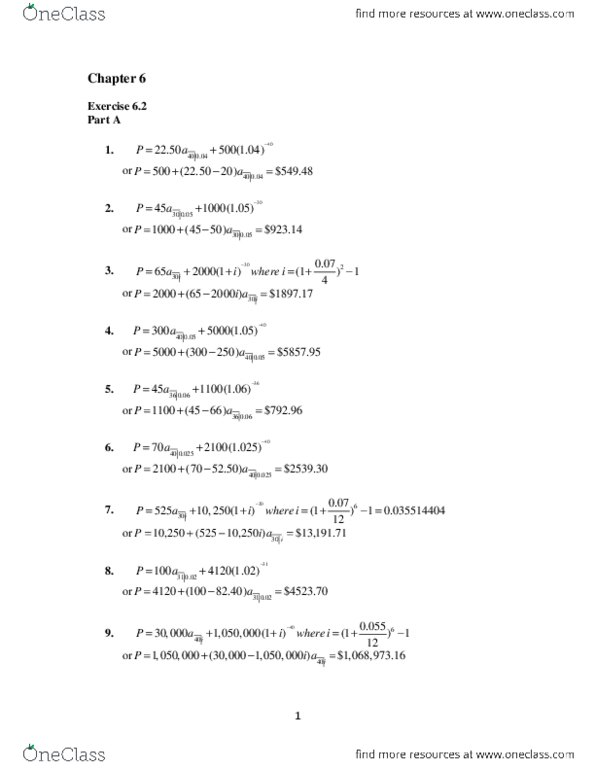

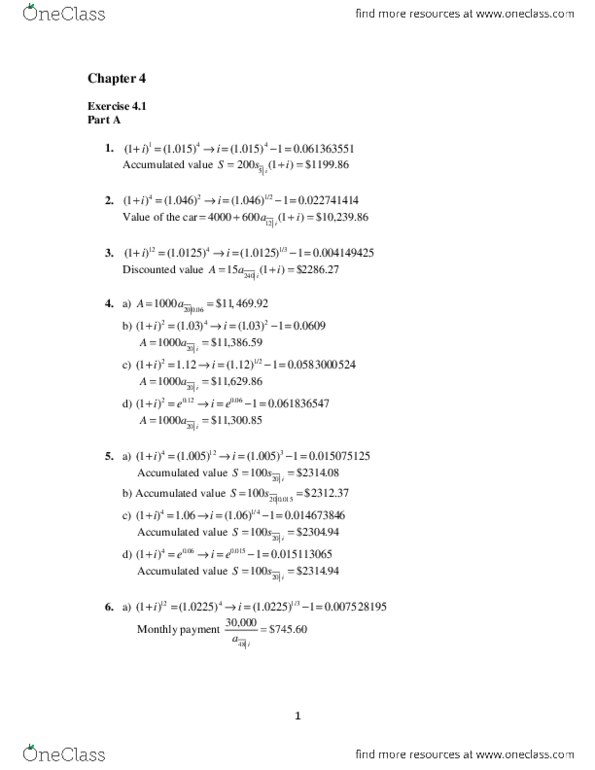

Part a: a) since the coupon rate is equal to the interest rate, the price of the 10-year bond is its redemption value, that is, b) after 4 years, the semi-annual effective interest rate is i(2)/2 = 2. 25%. Therefore, the sale price of the bond is. = . 11 c) the annual yield i over the 4 years is such that p1 (1+i)4 = p2, which solves for (1+i)4 = 1. 07811 and thus i = 1. 8980: a) 90a. . 001 c) solving the quadratic, d) as expected, the yield rates lie between 3. 5% and 4% since these are the spot. 3. 986% rates for the first and second years respectively: s (1+ s5)5. = 10225. 36 c) we want 10,225. 36 = 500a. Using the ti ba ii-plus calculator, i = 4. 38%. wp. 1s = 0. 01995 or 2. 00% per half year yp. 94. 501 = 2. 439 + 2. 403 +102. 50(1+ s3) 3 (1+ s3) 3. 3s = 0. 0456 or 4. 56% per half year.