ACCT 2230 Chapter Notes - Chapter 2: Variable Cost, Direct Labor Cost, Employee Benefits

65 views8 pages

12 Sep 2017

School

Department

Course

Professor

Document Summary

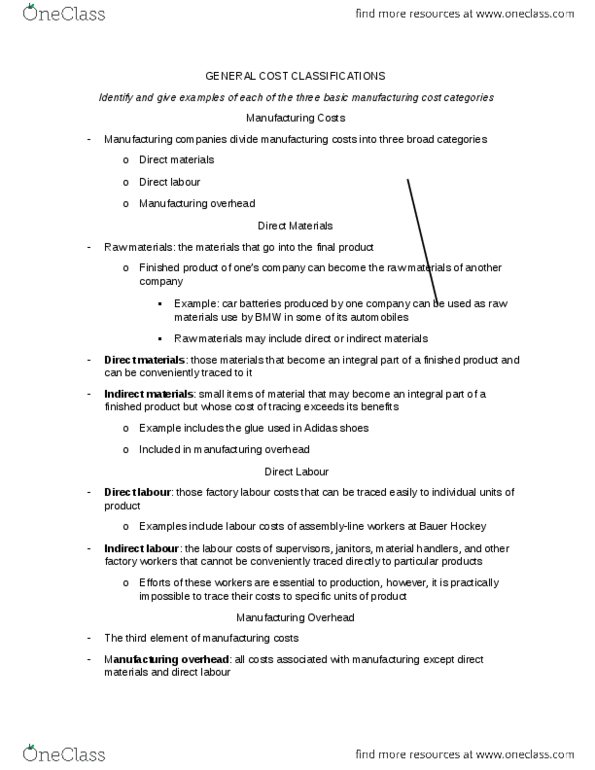

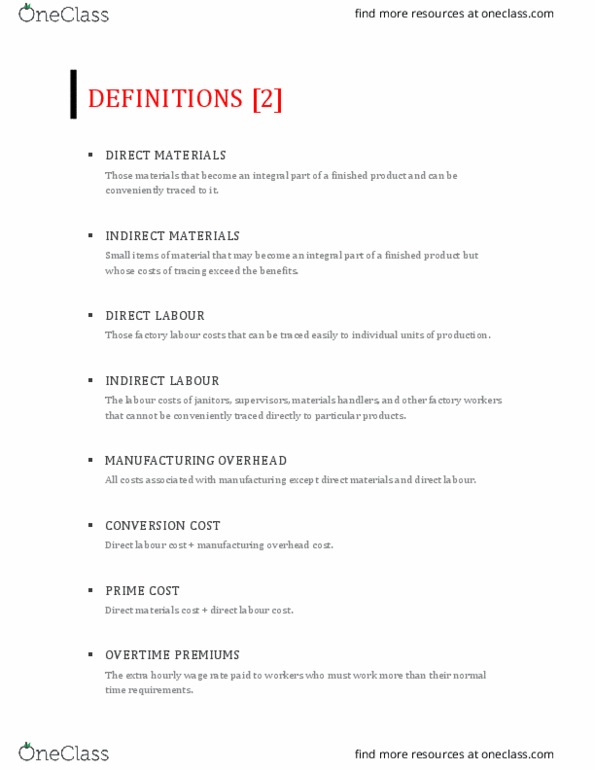

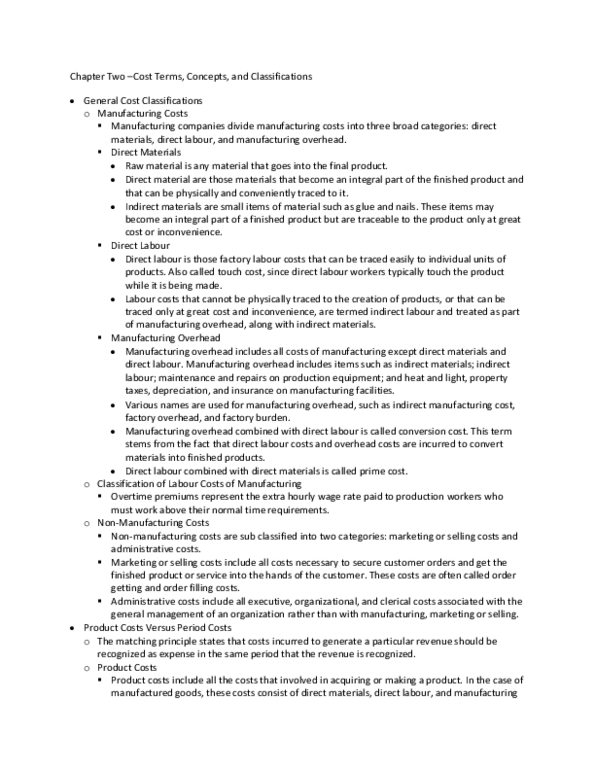

Divide manufacturing costs into three broad categories: direct materials, direct labour and manufacturing overhead. Direct materials: those materials that become an integral part of a finished product and can be conveniently traced to it. Indirect materials: small items of material that may become an integral part of a finished product but whose costs of tracing exceed the benefits. Direct labour : those factory labour costs that can be traced easily to individual units of product. Indirect labour: costs of janitors, supervisors, materials handlers, other factory workers. Manufacturing overhead: all costs associated with manufacturing except direct materials and direct labour. Only costs associated with operating the production facility (factory) Aka: indirect manufacturing cost, factory overhead, factory burden. Indirect materials, indirect labour, maintenance, repairs on production equipment, heat/light, property taxes, etc. Conversion cost: manufacturing overhead combined with direct labour. This term states stems from the fact that direct labour costs and overhead costs are incurred to convert materials into finished products.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Related Documents

Related Questions

Can anyone please help me do the step5, 6 and step 7 that are highlighted bold

| Step 1 | You work for Thunderduck Custom Tables Inc. This is the first month of operations. The company designs and manufactures specialty tables. Each table is specially customized for the customer. This month, you have been asked to develop and manufacture two new tables for customers. You will design and build the tables. This is a no nail, no screw, and no glue manufacturing ( no indirect materials used). You will be keeping track of the costs incurred to manufacture the tables using Job #1 Cost Sheet and Job #2 Cost Sheet. | |||

| The cost of the direct materials that can be used to manufacture the table are as follows. These cost are on a per unit basis. | ||||

| Table Top | $1,000.00 | |||

| Table Leg | $ 150.00 | |||

| Drawer | $ 300.00 | |||

| The company uses a job order costing system and applies manufacturing overhead to jobs based on direct labor hours. | ||||

| The company estimates that there will be 12 direct labor hours worked during the month. | ||||

| The estimated manufacturing overhead cost for the month is: | ||||

| a. | Factory supervisor salary per month | $ 2,500.00 | ||

| b. | Rent for the factory per month | $500.00 | ||

| c. | Depreciation of factory equipment per month | $600.00 | ||

| Total Estimated manufacturing overhead | $ 3,600.00 | |||

| What is the predetermined manufacturing overhead rate? | [POHR] | |||

| Step 2 | The first order you received was to manufacture a table using a table top and four legs. This is your Job #1. | |||

| Step 3 | The customer that has ordered Job #2, wants a table that is the same as Job #1, but wants to also add a drawer to the table. | |||

| Step 4 | The following is a list of transactions that need to be recorded for the company for activity in the month of December. Record those in the "General Journal" tab of the excel file using the proper format. Please use the following accounts: Accounts Receivables, Raw materials, Work in process, Finished goods, Accumulated depreciation, Accounts payable, Salaries and wages payable, Sales revenue, Manufacturing overhead, Cost of goods sold, Salaries and wages expense, Advertising expenses, and Depreciation expense. | |||

| 1-Dec | Raw Materials purchased on account, $10,000. | |||

| 5-Dec | All Raw Materials needed for Job #1 were requisitioned from the material storage for use during the month. Assume all materials are direct. (After you journalize this entry please enter the information into Job #1 Cost Sheet) | |||

| 10-Dec | The following employee costs were incurred but not paid during the month: | |||

| There are three assembly employees that spend 2 hours each, $20 per hour to make the table for Job #1. (After you journalize this entry please enter the information into Job #1 Cost Sheet) | ||||

| Salary for supervisor of the factory $3,000. | ||||

| Administrative Salary $2,000. | ||||

| 15-Dec | All Raw Materials needed for Job #2 were requisitioned from the material storage for use during the month. Assume all materials are direct. (After you journalize this entry please enter the information into Job #2 Cost Sheet) | |||

| 16-Dec | Rent for the month of December for the factory building incurred but not paid $500. | |||

| 17-Dec | Advertising costs incurred but not paid for the month was $1,200. | |||

| 20-Dec | Depreciation for the month of December was recorded on equipment was $750 ($150 for equipment used in the factory and the remainder for equipment used in selling and administrative activities). | |||

| 22-Dec | Manufacturing overhead cost was applied based on direct labor hours to Job #1 based on the POHR determined on the "Job Cost Sheet". (After you journalize this entry please enter the information into Job #1 Cost Sheet) | |||

| 26-Dec | Job #1 was completed and transferred to Finished Goods during the month. | |||

| 28-Dec | The completed table from Job #1 was sold on account to the customer for $15,000 during the month. (Hint: Make sure to account for the cost of the table that was sold using the cost from the job cost sheet.) | |||

| 31-Dec | Direct labor cost incurred but not paid for three employees to start manufacturing Job #2. The employees only worked one hour each, three hours total, $20 per hour during the month and they did not complete their work on the job. (After you journalize this entry please enter the information into Job #2 Cost Sheet) | |||

| 31-Dec | Manufacturing overhead cost was applied based on direct labor hours to Job #2 based on the POHR. Only three direct labor hours were worked on Job #2 during the month. (After you journalize this entry please enter the information into Job #2 Cost Sheet) | |||

| 31-Dec | Any underapplied or overapplied overhead for the month was closed out to Cost of Goods Sold. | |||

| Step 5 | Post the journal entries that you recorded on the "General Journal" tab to the "T-accounts" tab. This is the company's first month of business, so there will not be any beginning balances. Compute the balance for each T-account after all of the entries have been posted. | |||

| Step 6 | Prepare a Schedule of Cost of Goods Manufactured and a Schedule of Cost of Goods Sold on the "Schedule of COGM and COGS" tab for Job #1 and Job #2 that were worked on during the month by the company. Make sure to follow the format noted in your book (pg. 87). (Hint: This is the company's first month of operations and therefore the beginning balances will be zero.) | |||

| Step 7 | Prepare an Income Statement for the month using the Traditional Format on the "Income Statement" tab. | |||

| Step 8 | Answer the additional questions below | |||

| Check Figure: Cost of Goods Manufactured= $3,520, Net operating income=$6,730 | ||||

| What is the ending balance for raw materials? | [EndingRM] | |||

| What is the ending balance for work in process? | [EndingWIP] | |||

| What is the ending balance for finished goods? | [EndingFG] | |||

| What is the actual manufacturing overhead cost incurred during December before adjustment? | [ActualMOH] | |||

| What is the total applied manufacturing overhead cost during December before adjustment? | [AppliedMOH] | |||

| What is the unadjusted cost of goods sold? | [UnadjustedCGS] | |||

| Was the manufacturing overhead for the month of December overapplied/underapplied ? | [overorunderMOH] | |||

| What is the amount of Manufacturing overhead overapplied/underapplied? | [overorunderappliedMOH] | |||

| What is the adjusted cost of goods sold? | [AdjustedCGS] | |||

| What is gross margin? | [Grossmargin] | |||

| What is the total prime cost for Job#1? | [primecost] | |||

| What is the total conversion cost for job #1? | [conversioncost] | |||

| What is the total product cost for job#1? | [productcost] | |||

| What was the period cost incurred for the month of December? | [periodcost] | |||

| What is the total variable cost incurred for Job #1(assume that all selling and administrative cost and all manufacturing overhead costs are fixed.)? | [Variablecost] | |||

| What is the contribution margin for Job #1 (assume that all selling and administrative cost and all manufacturing overhead costs are fixed.)? | [contributionmarginofjob1] | |||

| What would be the actual (not applied) total fixed manufacturing overhead cost incurred for the company for the month if the order in Job #1 is for five tables instead of one table assuming this cost is with in the relevant range? | ||||

| And can you all please help me do the Job cost sheet 1, job cost sheet 2, general journal, to accounts ledger,

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Question 1

| I want answers for the questions that are in bold and italic letter. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||