ADMN 4301H Chapter Notes - Chapter 2: Financial Statement, External Auditor, Uptodate

30 Mar 2020

School

Department

Course

Professor

Document Summary

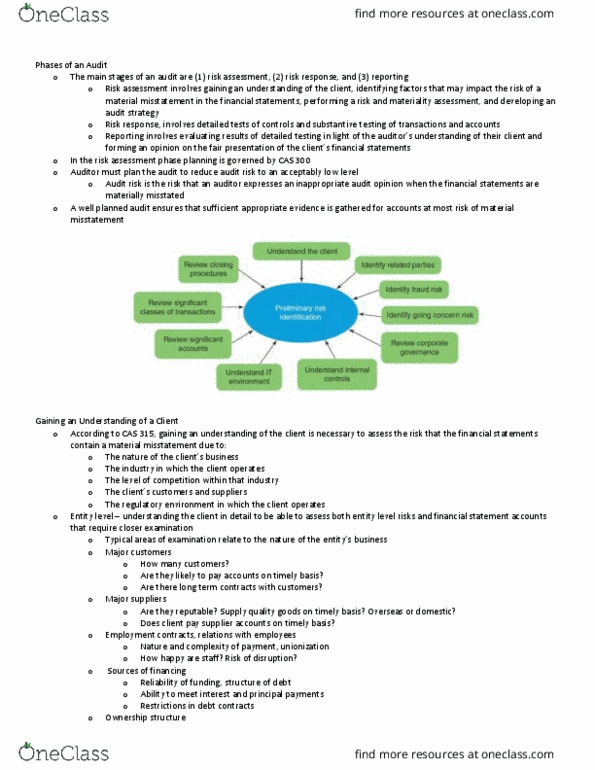

Fundamental principles of professional ethics: all professional accountants in canada must abide by a code of professional conduct, these principles are to act with, professional behaviour. Independence is the ability to act with integrity, objectivity, and with professional scepticism (questioning mind) Lack of auditor independence impacts on credibility and reliability of the financial statements: the auditor must be, and be seen to be, independent. Independence in fact: ability to act independently with integrity, objectivity and professional scepticism, ability to make a decision free from bias, personal belief, and client pressures. Independence in appearance: belief that independence of mind has been achieved, threats to independence. Self-interest threat: can occur if the audit firm or its staff have financial interest in audit client, examples, bank account held with the client. Shares owned in the client: a loan to or from the client, close business relationship with the client.