BUS 426 Chapter Notes - Chapter 12: Audit Evidence, Internal Control, Financial Statement

19 Sep 2012

School

Department

Course

Professor

Document Summary

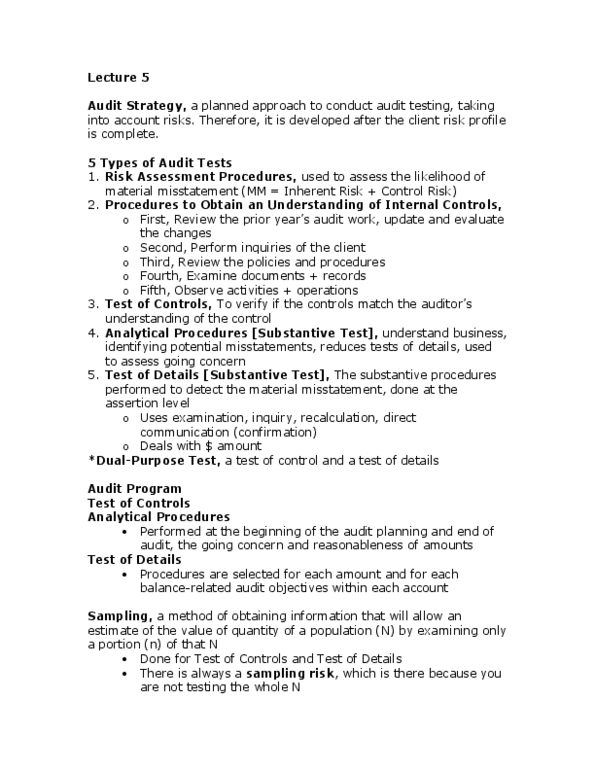

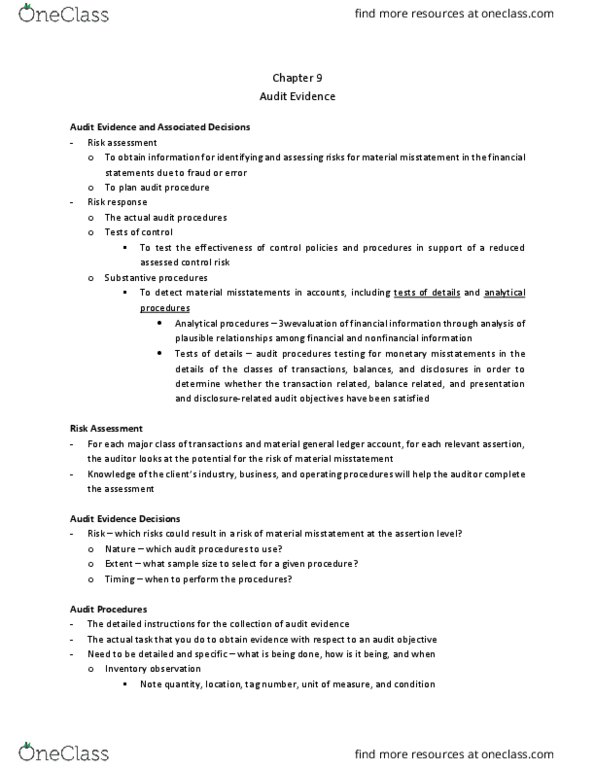

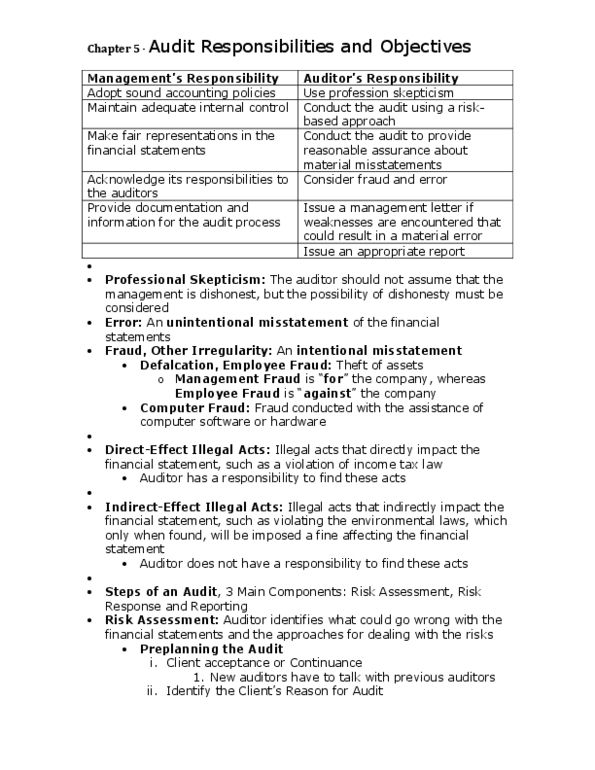

Audit strategy: a planned approach to the conduct of audit testing, taking into account assessed risks. Auditors use 5 types of tests to determine whether financial statements are fairly stated: risk assessment procedures, procedures to obtain an understanding of internal control, tests of controls, analytical procedures, test of details of balances. Substantive procedures are audit procedures that are used to quantify the amount of potential error in an account or transaction stream. Used to assess the likelihood of material misstatement (inherent risk plus control risk) in the financial statements. Audit procedures to test the effectiveness of controls in support of a reduced assessed control risk. Use of comparisons and relationships to determine whether account balances or other data appear reasonable. Procedures to obtain an understanding of internal control. Procedures used by the auditor to gather evidence about the design and implementation of specific controls.