BUS 420 Chapter Notes - Chapter 10: Forward Rate, Historical Cost, Cash Flow Hedge

14 Sep 2016

School

Department

Course

Professor

Document Summary

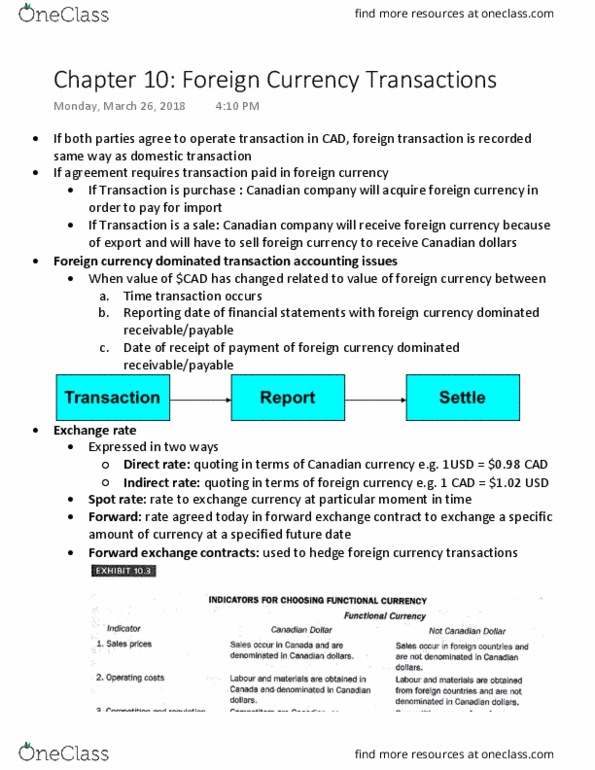

Many canadian companies conduct business in foreign countries as well as in canada. No specific accounting issues arise when the parties involved in an import or export transaction agree that the payment will be in canadian dollars. When the agreement calls for the transaction to be settled (paid) in foreign currency, this means one of the two things (foreign currency denominated transactions): If the transaction is a purchase, the canadian company will have to acquire foreign currency in order to discharge the obligations resulting from its imports. If the transaction is a sale, the canadian company will. Receive foreign currency as a result of its exports. Have to sell the foreign currency in order to receive canadian dollars. Accounting issues arise when the value of canadian dollar has changed relative to the value of the foreign currency between. The date at which the financial statements are reported with the foreign-currency- denominated (fcd) receivable or payable.