BUS 329 Chapter Notes - Chapter 11: Property Income, Small Business

6 Dec 2016

School

Department

Course

Professor

Document Summary

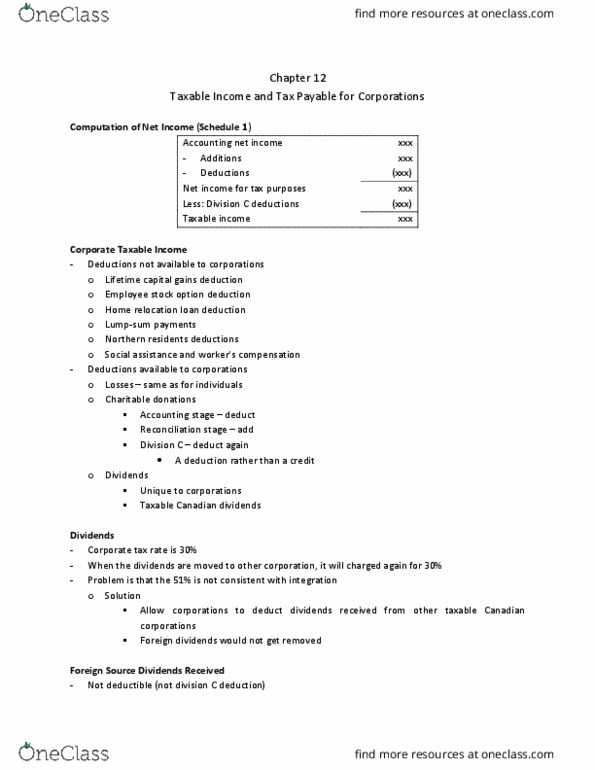

Taxable income and tax payable for individuals revisited. Other deduction from income: use these deductions first before proceeding with division c deductions, division c deductions. Carry over losses deductible: taxable income. Qualifying amounts: spousal and child support, pension benefits, and ei benefits, payments on termination of employment. Relief mechanism: qualifying amounts removed from income, alternative tax payable, notional interest is added. Allows to average out the spousal payments to each year, when you receive a lump-sum payment. Must be used in year incurred, if possible: may not have enough income, may not have the right type of income (ex. capital gains are required to use capital losses) Carry forward will result in reduced tax payable. Separate balances to be tracked: listed personal property losses. Carry back for 3 years, and forward for 7. ,(cid:882)(cid:882)(cid:882) minimum=pod=acb: non-capital losses, including business investment losses. Ca(cid:396)(cid:396)(cid:455)o(cid:448)e(cid:396) o(cid:374)l(cid:455) a(cid:448)aila(cid:271)le afte(cid:396) (cid:272)u(cid:396)(cid:396)e(cid:374)t (cid:455)ea(cid:396)"s i(cid:374)(cid:272)o(cid:373)e (cid:396)edu(cid:272)ed to (cid:374)il (cid:894)(cid:272)o(cid:396)po(cid:396)atio(cid:374)(cid:895) and ,474 (individual)