BUS 251 Chapter Notes - Chapter 4: Revenue Recognition, Cash Flow, Retained Earnings

17 Aug 2012

School

Department

Course

Professor

Document Summary

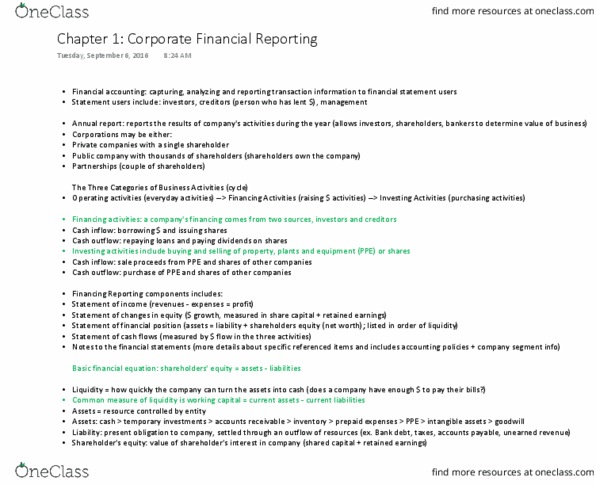

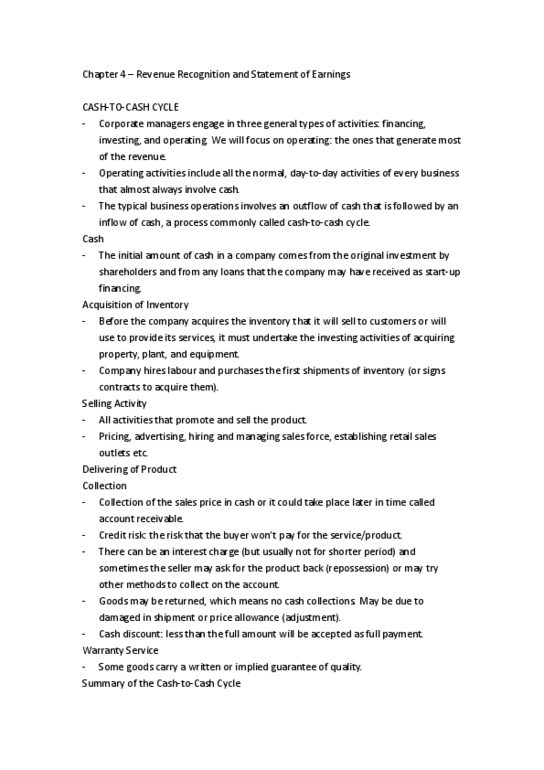

Chapter 4: revenue recognition and statement of earnings. Cash-to-cash cycle: operating cycles: all normal, day-to-day activities that mostly involve cash, buying and selling of inventory (outflow and inflow of cash) - cash to cash cycle, cash. Cash from shareholders through the issuance of shares and loans: acquisition of inventory (investing activities) buying property, plant and equipment. Filling the shelf by buying inventories and labor: selling activity. All the activities designed to promote products then sell them. Sales contract between buyer and seller is established. Payments are due at the same time they are purchase: delivery of the product. Delivery of the product depends on the contract: collection. Some of the cash collection process should almost be immediately or it can be recorded has accounts receivable and cash will be collected in another day. But there is a risk associated with the accounts receivable payment so there are interest charges (for long period of time)