ECN 104 Chapter Notes - Chapter 10: Demand Curve, Creative Destruction, Economic Equilibrium

3 Feb 2017

School

Department

Course

Professor

Document Summary

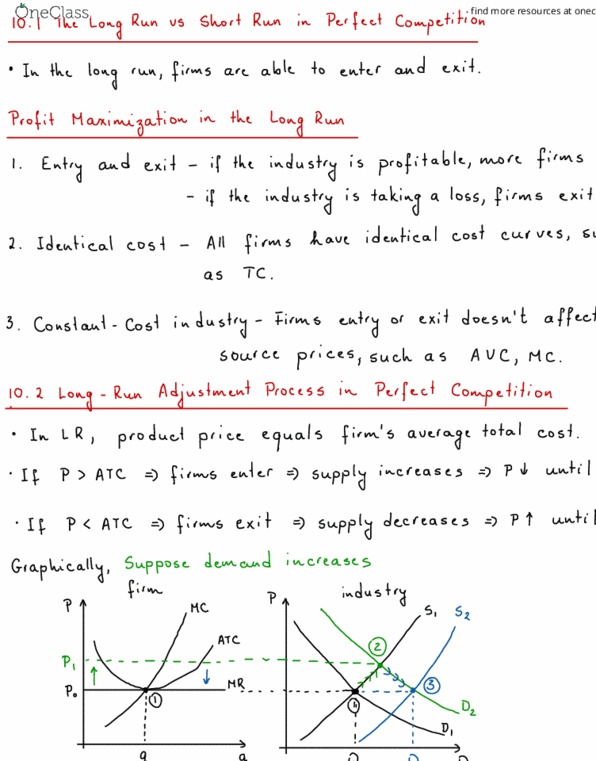

Chapter 10 perfect competition in the long run. 10. 1 - the long run vs the short run in perfect competition. Profit maximization in the long run: 3 assumptions. 10. 2 the long-run adjustment process in perfect competition. After all long-run adjustments, product price = minimum atc. Firms will leave the industry if short-run market price is less than total cost (economic loss: industry contraction decreases supply which eventually brings price back up to the minimum atc in the long run. If firms in the industry are earning a normal profit, there is no incentive for firms to enter or leave the industry. Entry eliminates economic profits, exit eliminates loss due to this behaviour^^ Interested in the effect that the entry/exit of firms has on the costs of individual firms in the industry. Long-run supply curve of constant-cost industry is perfectly elastic.