ACC 406 Chapter 4: Chapter 4

6 Feb 2012

School

Department

Course

Professor

Document Summary

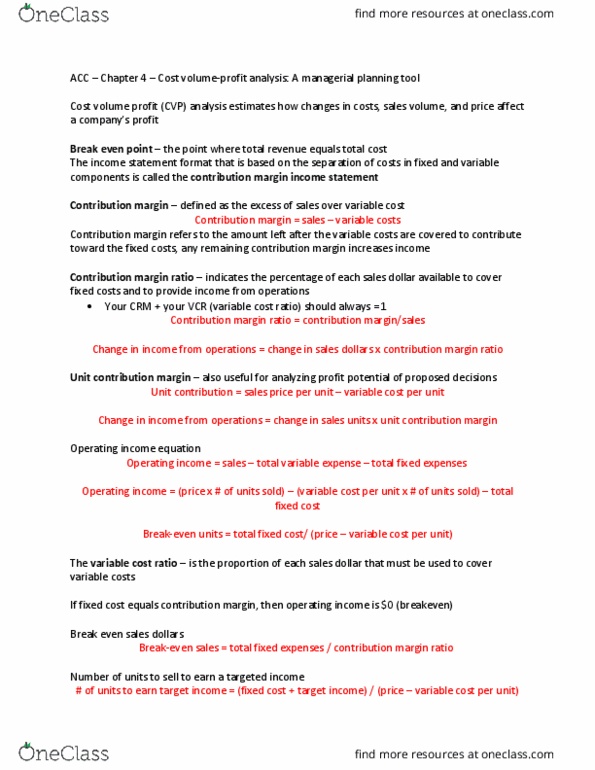

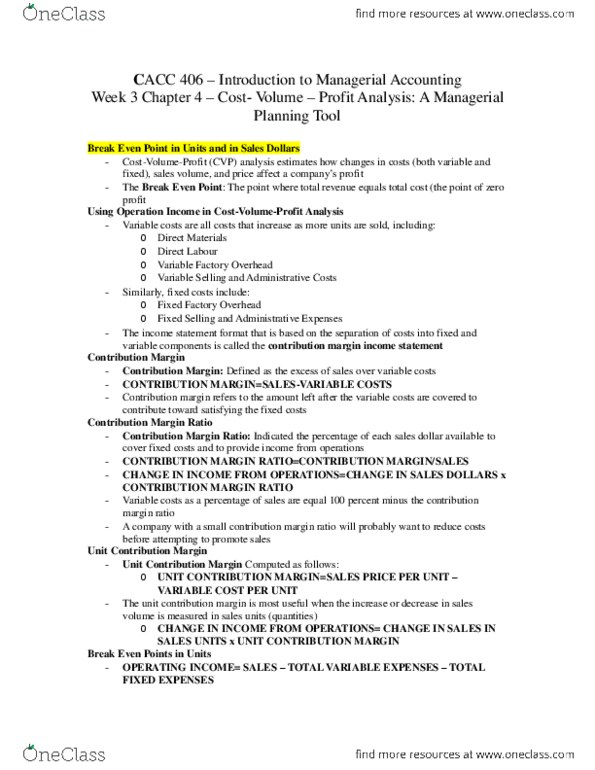

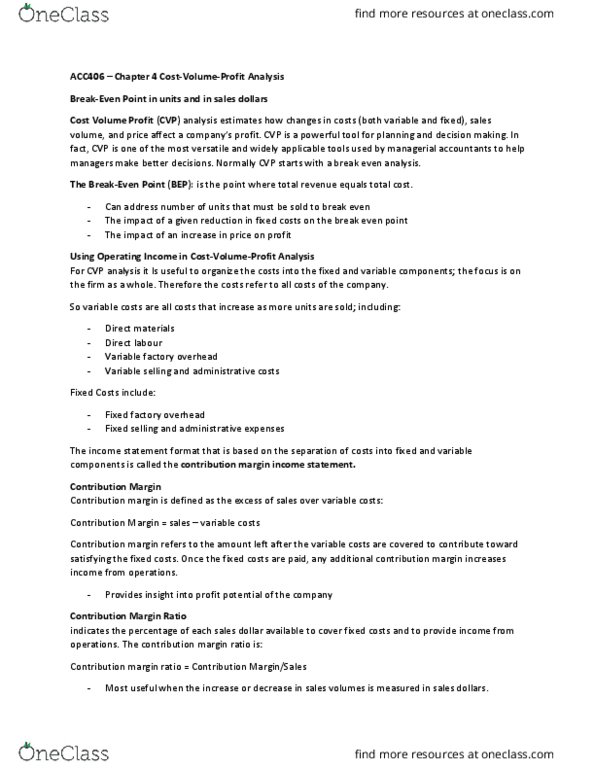

Acc 406 chapter 4 -- cost-volume-profit analysis: a managerial planning tool. Break-even point in units and in sales dollars: Cost-volume profit (cvp): estimates how changes in costs, sales volume, and prif e affect a company"s profit. Break-even profit: is the point where total revnue equals total cost (the point of zero profit) Can address: # of units that must be sold to break even; impact of a gi ven reduction in fixed costs on the break even point, impact of an increase in p rice on profit. Seperate expenses by fixed and variable, rather than by function (manufacturing expense, selling expense, etc. ) Contribution margin: difference between sales and variable expense. It is the amount of sales revenue left over after all the var exp are c overed an can be used for fixed exp. Contribution margin income statement: income statement based on seperation of c osts into fixed and variable.