ACC 406 Chapter 3: Chapter 3

6 Feb 2012

School

Department

Course

Professor

Document Summary

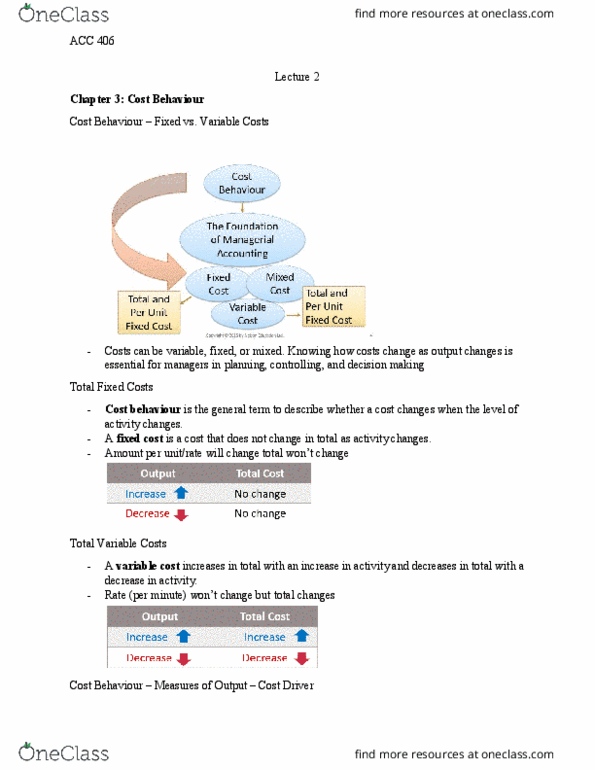

Cost behaviour: general term to describe whether a cost changes when the level o f output changes. Fixed cost: a cost that does not change in total as output changes. Variable cost: increases in total with an increase in output and decreases with a decrease in output. Driver: a causal factor that measures the output of the activity that leads (or causes) costs to change. Determine underlying business activity and figure out how it causes cos t to change (ex. Relevant range: is the range of output over which the assumed cost relationship is valid for the normal operations of the firm. Are costs that in total are constant within the relevant range as the level of output increases/decreases. Discretionary fixed costs: are fixed costs that can be changed or avoided relati vely easily at management decision. Cost that do not depend on the driver (ex. Commited fixed costs: fixed costs that cannot be easily changed.