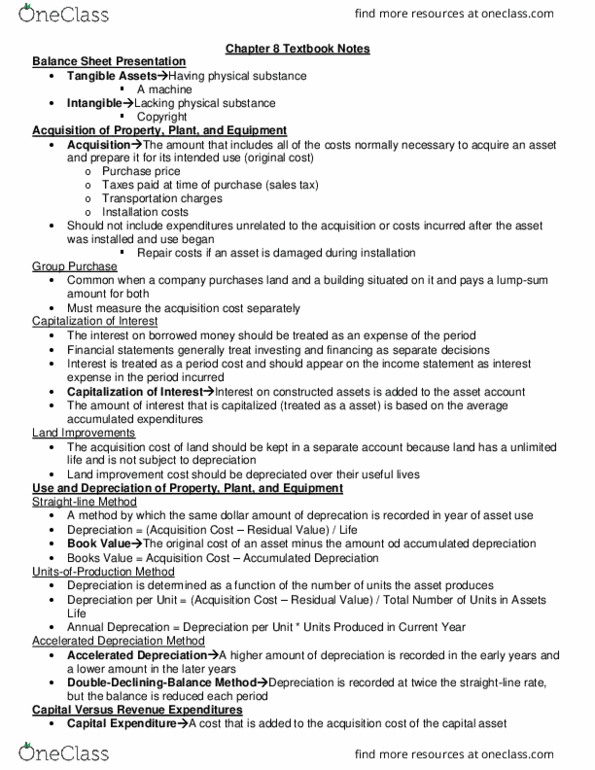

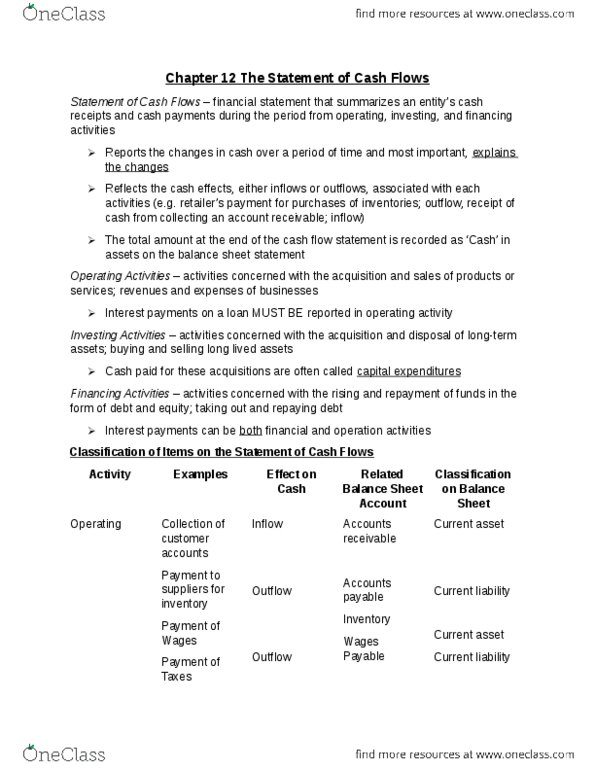

ACC 100 Chapter Notes - Chapter 8: Historical Cost, Capital Asset

Get access

Related Documents

Related Questions

Using the data in the Option 2 Spreadsheet(linked at the bottom of the page), perform the accounting requiredfor the acquisition of Little, Inc. by Big, Inc. This is an 80%acquisition, where the book value of the assets acquired is lessthan the acquisition price. Within the worksheet, you are to:

1. Select an accounting method (either cost or equity) andexplain why you selected this method

2. Perform the required journal entries

3. Complete the consolidation worksheet

4. Prepare the consolidated balance sheet in good form

| Big CompanyBalance Sheet | Which accountingmethod is most appropriate for representing an investment of thistype? | Prepare Elimination Entriesfor Stock Acquisition | ||||||||

| Assets, Liabilities & Equities | Book Value | Account | DR | CR | ||||||

| Cash | $2,100,000 | |||||||||

| AR | $10,000 | |||||||||

| Inventory | $200,000 | |||||||||

| Land | $40,000 | |||||||||

| PP&E | $400,000 | |||||||||

| Accumulated Depreciation | -$150,000 | |||||||||

| Patent | $0 | |||||||||

| Total Assets | $2,600,000 | Prepare thejournal entries for a 80% Asset Acquisition (using Big CompanyCash) | ||||||||

| AP | $100,000 | |||||||||

| Common Stock ($10 par) | $450,000 | Account | DR | CR | ||||||

| Additional Paid In Capital | $600,000 | |||||||||

| Retained Earnings | $1,450,000 | |||||||||

| Total Liabilities &Equity | $2,600,000 | Prepare thejournal entries for a 80% Acquisition by issuing 10,000 shares ofBig Company Stock | Big Company Balance Sheet (Consolidated) | |||||||

| Little Company BalanceSheet | Assets, Liabilities & Equities | |||||||||

| Assets, Liabilities & Equities | Book Value | Account | DR | CR | Cash | |||||

| Cash | $35,000 | Investment in Little | AR | |||||||

| AR | $10,000 | Common Stock | Inventory | |||||||

| Inventory | $65,000 | Additional Paid In Capital | Land | |||||||

| Land | $40,000 | Allocation of Excess Schedule | PP&E (net) | |||||||

| PP&E | $400,000 | Accumulated Depreciation | ||||||||

| Accumulated Depreciation | -$150,000 | Goodwill | ||||||||

| Patent | $0 | Patent | ||||||||

| Total Assets | $400,000 | Total Assets | ||||||||

| AP | $100,000 | AP | ||||||||

| Common Stock | $100,000 | Common Stock ($10 par) | ||||||||

| Additional Paid In Capital | $50,000 | Additional Paid In Capital | ||||||||

| Retained Earnings | $150,000 | Retained Earnings | ||||||||

| Total Liabilities &Equity | $400,000 | NCI | ||||||||

| Total Liabilities & Equity | ||||||||||

| Assumethat all noncash assets have a Fair Value that is 10% greater thanBook Value | ||||||||||

Stockholders' Equity Section of Balance Sheet

The following accounts and their balances appear in the ledgerof Goodale Properties Inc. on June 30 of the current year:

| Common Stock, $45 par | $3,060,000 |

| Paid-In Capital from Sale of Treasury Stock | 115,000 |

| Paid-In Capital in Excess of ParâCommon Stock | 272,000 |

| Retained Earnings | 20,553,000 |

| Treasury Stock | 324,000 |

Prepare the Stockholdersâ Equity section of the balance sheet asof June 30 using Method 1 of Exhibit 8. Eighty thousand shares ofcommon stock are authorized, and 9,000 shares have beenreacquired.

| Goodale Properties Inc. | |||

| Stockholders' Equity | |||

| June30, 20XX | |||

| Paid-In Capital: | |||

| $ | |||

| $ | |||

| Total Paid-In Capital | $ | ||

| Total | $ | ||

| Total Stockholders' Equity | $ | ||