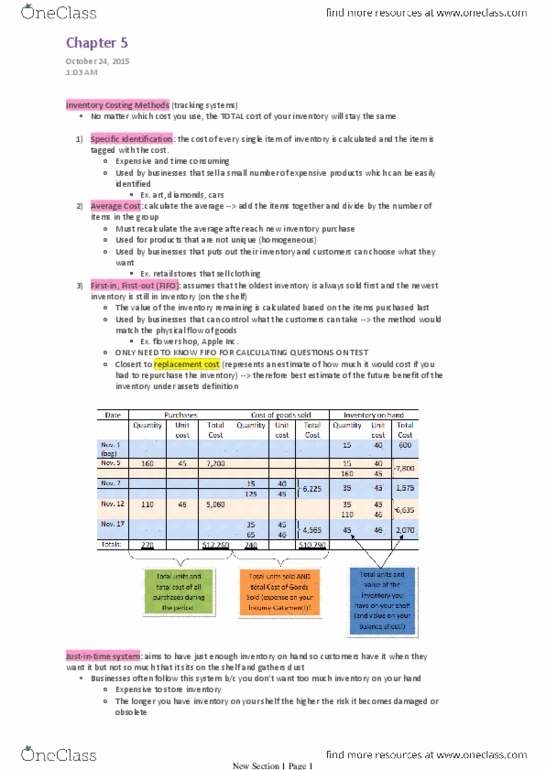

ACC 100 Chapter Notes - Chapter 6: The Beer Store, Cash Register

13 Jun 2018

School

Department

Course

Professor

ACC 100- Chapter 6

Inventory Costing & Controls

Three inventory costing methods

1. Specific Identification

2. Average Cost

3. First-in, First-out (FIFO)

Specific Identification

- the cost of every single item of inventory is calculated and the item is tagged with the cost

- when an item is sold, the cost of that specific item is moved from the Inventory account (an

asset decreases) to Cost of Goods Sold (an expense because it was used to generate revenue)

- expensive and time consuming

- used for businesses that sell a small number of expensive products which can be easily

identified, either because they are unique (original art), have serial numbers (cars) or special

markings (diamonds)

Date

Colour

Cost

February 2

Red

$10,000

February 12

Blue

$11,000

February 27

Green

$12,000

Total

-

$33,000

Average Cost

- you average out the costs of each inventory you buy

- average cost changes each time you buy new inventory

Purchases

Average cost

Red car

$10,000

Blue car

$11,000

Total cost of 2 cars

$21,000

Average cost per car*

$10,500

Purchases

Average cost

Red car

$10,000

Blue car

$11,000

Green car

$12,000

Total cost of 3 cars

$33,000

Average cost per car**

$11,000

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Three inventory costing methods: specific identification, average cost, first-in, first-out (fifo) The cost of every single item of inventory is calculated and the item is tagged with the cost. When an item is sold, the cost of that specific item is moved from the inventory account (an asset decreases) to cost of goods sold (an expense because it was used to generate revenue) Used for businesses that sell a small number of expensive products which can be easily identified, either because they are unique (original art), have serial numbers (cars) or special markings (diamonds) You average out the costs of each inventory you buy. Average cost changes each time you buy new inventory. So, when you are filling out the accounting formula, the inventory would increase by the average cost, not the cost of the specific car that you sold. Assumes that the oldest inventory is always sold first and the newest inventory is still in inventory (on the shelf)