ACC 100 Chapter Notes - Chapter 4: Flowchart, Cash Flow, Retained Earnings

13 Oct 2016

School

Department

Course

Professor

Document Summary

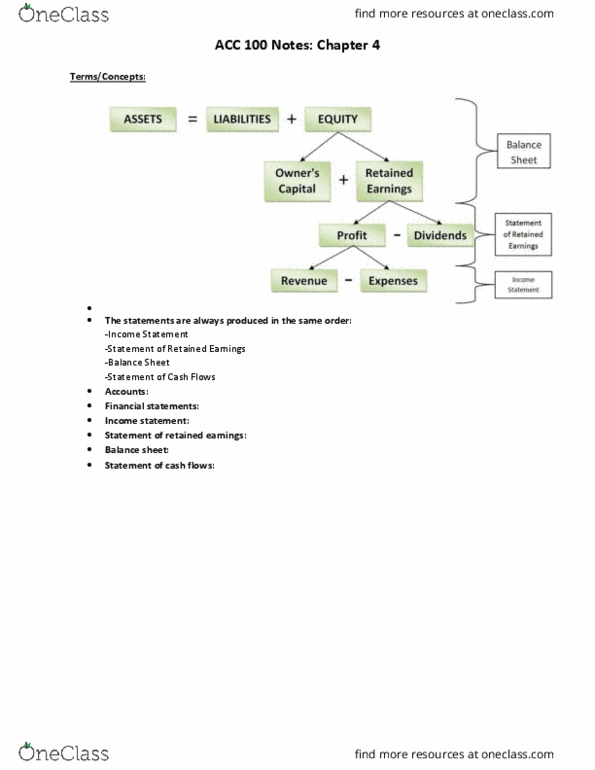

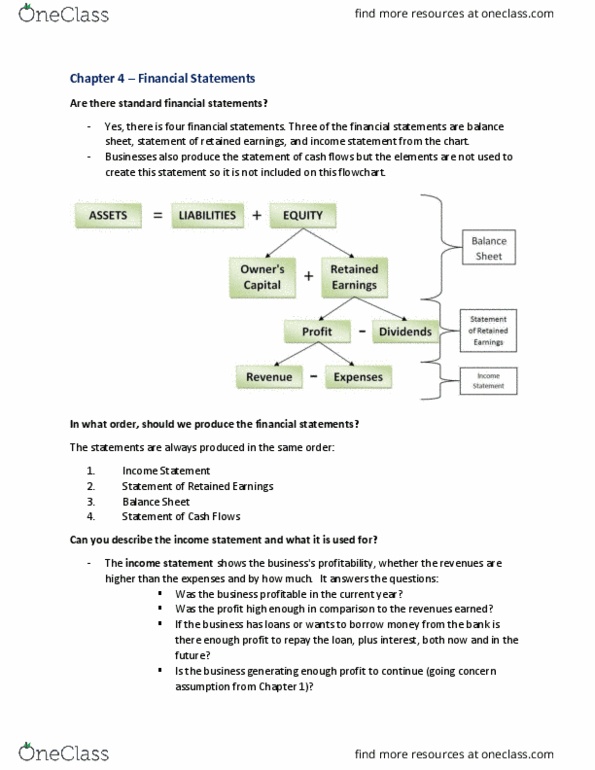

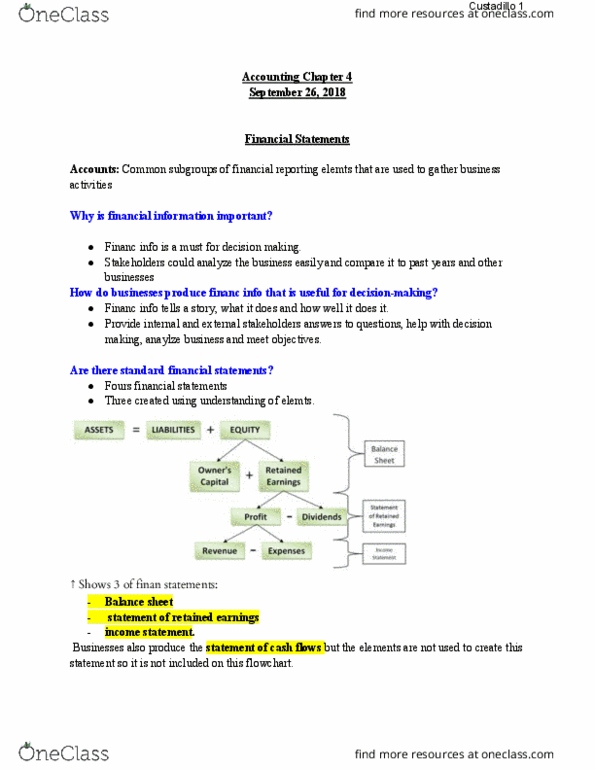

There are four financial statements, three of them are created using our understanding of the elements. The 3 financial statement showed are: balance sheet, statement of retained earnings, and income statement. This flowchart is only used when a business is in the 1st year of operations. In the 2nd year, additional info would be provided, such as opening retained earnings. In what order should we produce the financial statements: income statement, statement of retained earnings, balance sheet, statement of cash flows. The statement of cash flows is a statement which explains something rather than producing a number which is used in another statement. It describes the inflows and outflows of cash during the period. It sho(cid:449)s the (cid:271)usi(cid:374)ess"s p(cid:396)ofita(cid:271)ilit(cid:455), (cid:449)hethe(cid:396) the (cid:396)e(cid:448)e(cid:374)ues a(cid:396)e highe(cid:396) tha(cid:374) the e(cid:454)pe(cid:374)ses and by how much. The lo(cid:374)g te(cid:396)(cid:373) su(cid:396)(cid:448)i(cid:448)al of a(cid:374)(cid:455) (cid:271)usi(cid:374)ess is depe(cid:374)de(cid:374)t o(cid:374) its" p(cid:396)ofit (cid:271)e(cid:272)ause it"s the o(cid:374)l(cid:455) consistent source of cash over the long term.