ECON 1B03 Chapter Notes - Chapter 13: Average Variable Cost, Marginal Cost, Marginal Product

29 Jul 2016

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

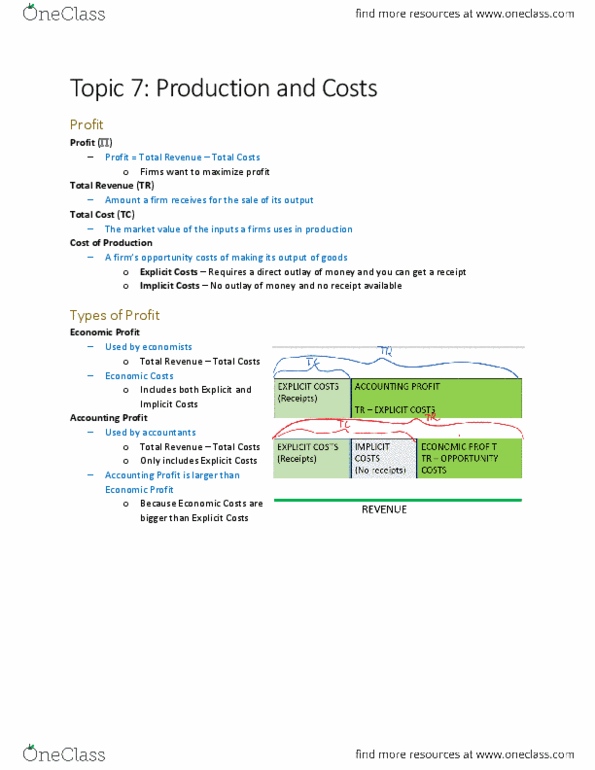

From the production function to the total-cost curve. The total product (tp) and total cost (tc) curves are inverses of each other. Marginal cost (mc): the change in total cost that arises from an extra unit of production; measures the rate of change in total costs as total product changes. Cost curves and their shapes: the costs of production. Costs as opportunity costs explicit costs: input costs that require an outlay of money by the firm implicit costs: input costs that do not require an outlay of money by the firm; time, other options. The cost of capital for firms could be considered an opportunity cost or an investment. The production function production function: the relationship between quantity of inputs used to make a good and the quantity of output of that good. Marginal product: the increasing rate of change in output that arises from an additional unit of input.