COMMERCE 1AA3 Chapter Notes - Chapter 6: Barcode, Inventory Turnover, Write-Off

3 Nov 2016

School

Department

Course

Professor

Document Summary

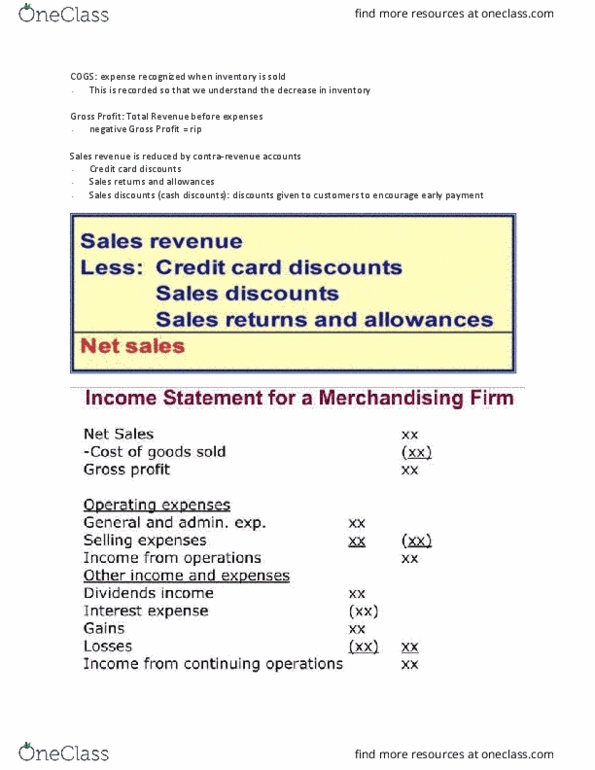

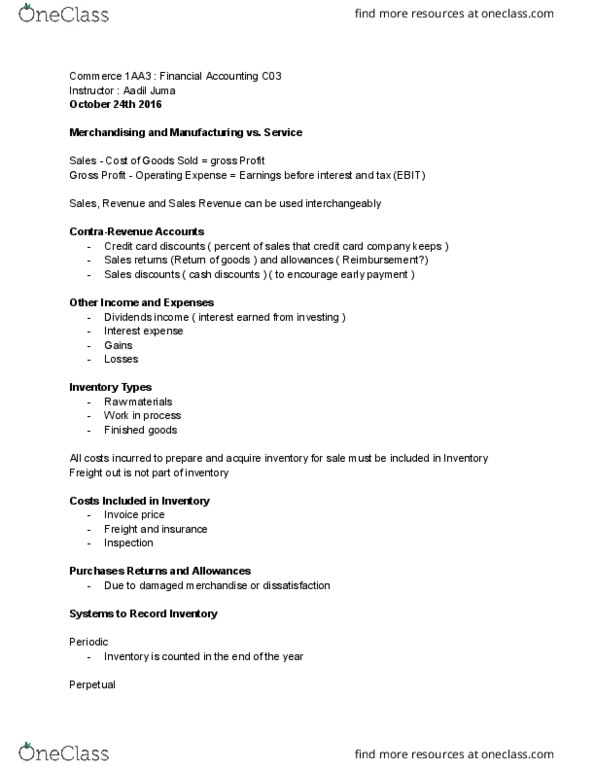

Cost of goods sold is a business"s largest expense. Merchandise inventory is the heart of a merchandising business, and the cost of goods sold is the most important expense for a company that sells goods rather than services. Account for inventory using the perpetual and periodic. Inventory is on the balance sheet and cost of goods sold is on the income statement. The value of inventory affects two financial statements. Cost of inventory on hand = inventory (asset on the balance sheet) Cost of inventory that has been sold = cost of goods sold (expense on the income statement) Inventory cost shifts from asset to expense when the seller delivers the good to the buyer. Gross profit is the excess of sales revenue over cost of goods sold. Called gross profit because operating expenses have not yet been subtracted. Inventory (balance sheet) = number of units inventory on hand x cost per unit of inventory.