ACCT-4021EL Chapter Notes - Chapter 7: Property Income, Dividend Tax, European Cooperation In Science And Technology

126 views10 pages

Document Summary

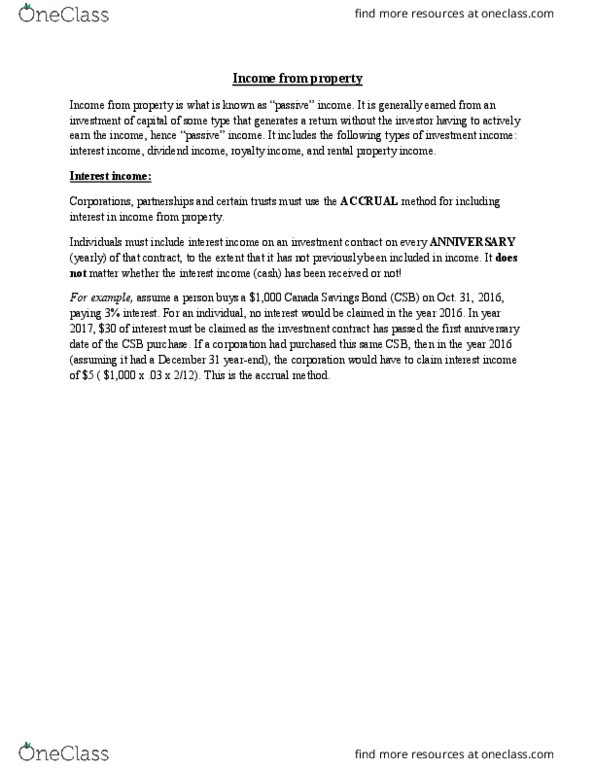

In cases where a great deal of time and effort is directed at producing interest or rents, such returns can be considered business income and the classification of such is important! There are differing views on the extent to which interest costs should be considered a deductible item . The real problem, however, is that there are such a multitude of provisions related to the special treatment of certain types of income and to the deferral of income, that the application of this concept becomes complex. In general, participating payments (ex. payments based on earnings) are not considered to be interest. However, if there is an upper limit on the applicable rate and that upper limit reflects prevailing market conditions, such payments may qualify as interest. Payments that are contingent on some future event would not generally be considered interest.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers