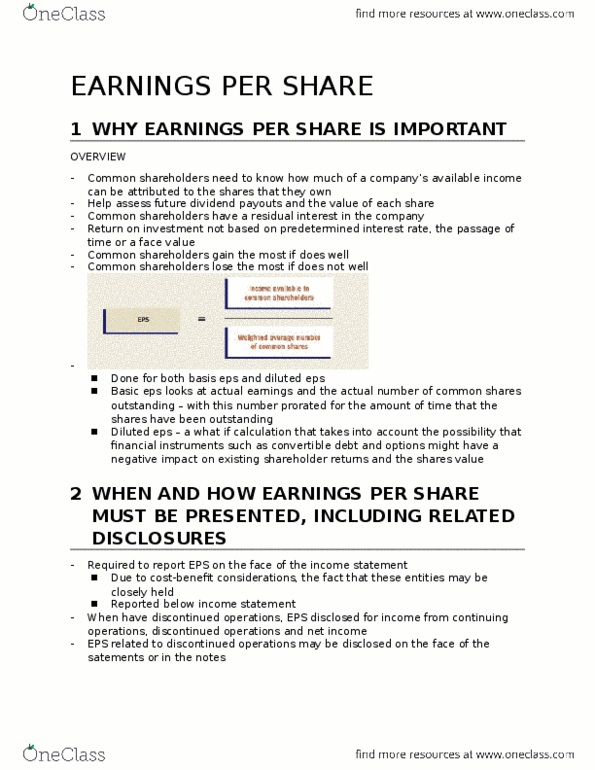

ACCT-3021EL Chapter Notes - Chapter 17: Stock Split, Income Statement, Financial Statement

Document Summary

Get access

Related Documents

Related Questions

6. Hasbrooke Corporation has 50,000 shares of $1 par value commonstock and 20,000 shares of cumulative 8%, $100 par preferred stockoutstanding. Hasbrooke has not paid a dividend for the prior year.If Hasbrooke declares a $1.50 per share dividend this year, whatwill be the total amount they must pay their shareholders?

A) $30,000

B) $320,000

C) $395,000

D) $75,000

7. Retained earnings represents:

A) Cash available for dividends.

B) The amount initially invested in the business bystockholders.

C) Cash available for expansion and growth.

D) Income that has been reinvested in the business rather thandistributed as dividends to stockholders.

8. On January 1,2006, Lane Corporation had 50,000 shares of $5 par value commonstock outstanding. On March 31, 2006, Lane issued an additional8,000 shares in exchange for a building. What number of shares willbe used in the computation of basic EPS for the year 2006?

A) 50,000.

B) 58,000.

C) 56,000.

D) 52,000.

9. Mirage Corporation's financial statements for the current yearinclude the following:

Income from continuingoperations............................................................... | $620,000 |

Prior period adjustment (increase in prior year net | 190,000 |

Cash dividends paid to preferredstockholders............................................................ | 202,000 |

Gain on sale of discontinued operations (net oftaxes)...................................................................... | 410,000 |

Operating loss on discontinued operations (net of taxes) | 320,000 |

Extraordinary loss (net of taxbenefit)................................................................... | 95,000 |

On the basis of this information, net income for the current yearis:

A) $1,007,000.

B) $ 620,000.

C) $1,445,000.

D) $ 615,000.

10. During the year 2007,Moonglow Corporation suffered a $600,000 loss when its factory wasdestroyed in a flood. Assuming the corporate income tax rate is34%, what amount will Moonglow report as an extraordinary loss onits income statement for 2007? Assume floods are not common in thisarea.

A) $600,000

B) $396,000

C) $204,000.

D) Nothing, since this does not qualify as an extraordinaryitem.

11. Galaxy Corporation was organized on January 1 and issued 500,000shares of common stock on that date. On July 1, an additional200,000 shares were issued for cash. Net income for the year was$2,160,000. Net earnings per share amounted to:

A) $4.32.

B) $3.75.

C) $3.09.

D) $3.60.

18. Kims Corporation plansto invest $100 million to earn about 20% before income taxes. Thecompany is considering whether it should raise the $100 million byissuing 10% bonds payable or capital stock. If the company issuesthe bonds, it will probably report:

A) Lower net income and lower income taxes expense than if itissues capital stock.

B) Higher net income and higher income taxes expensethan if it issues capital stock.

C) Lower net income and higher income taxes expensethan if it issues capital stock.

D) Higher net income and lower income taxes expense than if itissues capital stock.

19. The amortization of a bonddiscount:

A) Decreases the carrying value of a bond and increases interestexpense.

B) Decreases the carrying value of a bond and decreasesinterest expense.

C) Increases the carrying value of a bond and increasesinterest expense.

D) Increases the carrying value of abond and decreases interest expense.

Common Size Income statement | ||||

2017 | 2016 | |||

$M | Percentage | $M | Percentage | |

Operating revenue | 2319 | 100% | 2375 | 100% |

Operating expenses | -1666 | -71.84% | -1725 | -72.63% |

Earnings before interest, tax, depreciation, amortisation,changes in fair value of hedges and other signifcant items(EBITDAF) | 653 | 28.16% | 650 | 27.37% |

Depreciation and amortisation | -264 | -11.38% | -236 | -9.94% |

Impairment of assets | -10 | -0.43% | -4 | -0.17% |

Loss on sale of assets | -4 | -0.17% | -1 | -0.04% |

Net change in fair value of electricity and other hedges | -76 | -3.28% | -15 | -0.63% |

Operating profit | 299 | 12.89% | 402 | 16.93% |

Finance Cost | 79 | 3.41% | 80 | 3.37% |

Interest Income | 2 | 0.09% | 2 | 0.08% |

Net change in fair value of treasury instruments | 55 | 2.37% | -68 | -2.86% |

Net profit before tax | 277 | 11.94% | 256 | 10.78% |

Income tax expense | -80 | -3.45% | -71 | -2.99% |

Net proft after tax attributed to the shareholders of the parentcompany | 197 | 8.50% | 185 | 7.79% |

Earnings per share (EPS) attributed to ordinary equityholders of the parent | cents | cents | ||

Basic and diluted earnings per share | 7.7 | 0.33% | 7.2 | 0.30% |

COMPREHENSIVE INCOME STATEMENT

COMPREHENSIVE INCOME STATEMENT | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

2017 | 2016 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

$M | Percentage | $M | Percentage | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Net profit after tax | 197 | 8.50% | 185 | 7.79% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Other comprehensive income | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Intems that will not be reclassifed to profit or loss | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Asset revaluation | 428 | 18.46% | 889 | 37.43% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Defferred tax on the above item | -120 | -5.17% | -248 | -10.44% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Items that may be reclassified to profit or loss | 308 | 641 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Net gain on cash flow hedges | 2 | 0.09% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Exchange differences arising from translation of foreignoperation | 1 | 0.04% | -23 | -0.97% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Income tax on the above items | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

3 | 0.13% | -23 | -0.97% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Other comprehensive income for the year, net of tax | 311 | 13.41% | 618 | 26.02% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Total comprehensice income for the year, net of tax attributedto shareholders of parent company | 508 | 21.91% | 803 | 33.81% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Using the following financial ratiosfor 2016 and 2017 periods, and other associated information available in the publicdomain, assess the financial health of MEL from the view of an investor. Liquidity ratios b) Asset management efficiencyratios c) Profitability ratios d) Market ratios Assume you are a banker evaluating aloan request from Meridian Energy Limited (MEL) for $220 million. ConsideringMELâs recent earnings announcements and earnings forecast updates, what wouldbe your concerns in deciding on approval or denial of the loan request? Use thecompanyâs capital structure ratios for 2016 and 2017 in your explanation. |