ACCT-3021EL Chapter Notes - Chapter 16: Financial Instrument, Pork Belly, Financial Intermediary

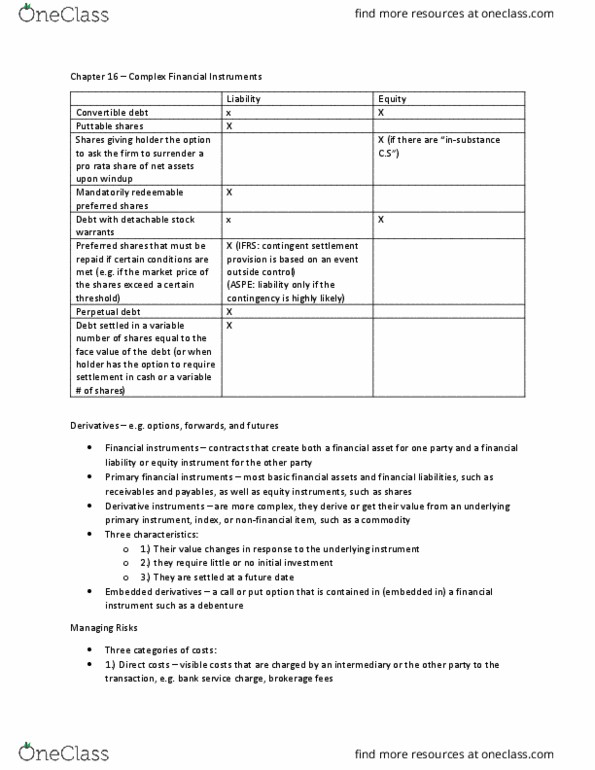

Chapter 16 – Complex Financial Instruments

Derivatives

Financial Instruments – contracts that create both a financial asset for one party and a financial liability or

equity instrument for the other party; can be primary or derivative

Primary Financial Instruments – include most basic financial assets and financial liabilities, such as

receivables and payables, as well as equity instruments, such as shares

Derivative Instruments – those that transfer risks from one party to another with little or no upfront

investment; they get their value from an underlying primary instrument, index, or non-financial item

An example of a financial derivative instrument is a forward contract to buy U.S. dollars, and an example of a

non-financial derivative instrument is a contract to buy pork bellies or potatoes

Derivatives have 3 characteristics:

1. Their value changes in response to the underlying investment

2. They require little or no initial investment

3. They are settled at a future date

They may trade on exchanges such as the Canadian Derivatives Exchange, and over-the-counter (OTC) markets

which are less formal and often involve financial institutions as the financial intermediary

EX. One risk faced by many Canadian entities is the weather. Insurance companies can face billion-dollar

payouts to policyholders after a flood, tornado, or ice storm

To help mitigate the risk of weather events causing large losses, weather derivatives were created. They derive

their value from an entity betting on a triggering weather event, such as a certain amount of rainfall or damage

MANAGING RISKS

In short, derivatives exist to help companies manage risks. While managing risk helps keep uncertainty at an

acceptable level, it also has costs. Categories of costs relating to the use of derivatives include:

Direct Costs – visible costs that are charged by an intermediary or other party to the transaction

→ Indirect Costs – less visible costs, such as the activity of researching, analyzing, and executing these

transactions, which uses a significant amount of employee time

→ Other Costs – those that could be considered “hidden”

Excessive complicated financial instruments increases the complexity of the financial statements and

reduces their transparency & understandability. Capital markets may penalize such companies by increasing

costs of capital and/or limiting or denying access to capital

Opportunity Costs are also included, because managing risk sometimes results in limiting the potential or

opportunity for gain

While derivatives often expose the company to additional risks, this only causes a problem when stakeholders

do not understand the risk profile of derivative instruments

Companies use derivatives to manage risks, and especially financial risks. There are various kinds of financial

risks, and they are defined in IFRS as follows:

1. Credit Risk – the risk that one party to a financial instrument will cause a financial loss for the other

party by failing to discharge an obligation

2. Liquidity Risk – the risk that an entity will encounter difficulty in meeting obligations associated with

financial liabilities

3. Market Risk – there are 3 types of market risk, including:

▪ Currency Risk – the risk that the FV or future CF of a financial instrument will fluctuate

because of changes in foreign exchange rates

▪ Interest Rate Risk – the risk that the FV or future CF of a financial instrument will fluctuate

because of changes in the market interest rates

▪ Other Price Risk – the risk that the FV or future CF of a financial instrument will fluctuate

because of changes in the market price (other than interest rate/currency), whether those changes

are caused by factors specific to the individual instrument or its issuer, or those that affect all

similar financial instruments being traded in the market

An entity may use hedging, a strategy where they enter into a contract with another party in order to reduce

exposure to existing risks… It is also possible to enter into derivative contracts to create positions that are

expected to be profitable. Both are acceptable and depend on the company’s risk tolerance profile

Any business that purchases or sells commodities has a market risk, those that sell on credit have credit risks,

and companies that borrow money or incur liabilities increase liquidity and interest-rate risk

Producers and Consumers as Derivative Users

EX. McCain needs 2 months to harvest potatoes and deliver them to market. The company has market risk

related to its inventory. Since they are concerned that the price of potatoes will drop, they sign a contract to sell

potatoes today, at the current market price, for delivery in 2-months

Suppose McDonalds wants to have potatoes in 2 months and is worried that prices will increase. They also have

a market risk, and therefore agree to delivery in two months at the current fixed price because they know they

will need potatoes in 2 months & can make an acceptable profit at the current price level

Speculators and Arbitrageurs as Derivative Users

Speculator – one who takes on additional risk in the hope of making future gains; goal is to generate a cash

profit from trading in the derivative instrument itself

• They will never take delivery of the product, as that is not their intention

• Unlike a hedging transaction to reduce pre-existing risk, there is no pre-existing risk for a speculator,

just a desire to take on additional risk in the hopes of increasing profits

EX. If a speculator buys the contract from McCain, they are betting that the price of potatoes will increase and

that the value of the forward contract will therefore also increase. The speculator will then sell the forward

contract to another speculator or to a company like McDonald’s. They will not take delivery of the potatoes

Arbitrageur – market players that try to take advantage of inefficiencies in different markets; try to lock in

profits by simultaneously entering into transactions in 2 or more markets

Arbitrageur’s exist because there is information asymmetry in different markets. This occurs when the same

information is not available to all market participants in the different markets

• Some markets are more efficient than others

• The arbitrageurs force the prices in the different markets to move toward each other because they create

demand & supply where previously there might not have been any, thus driving the prices up or down

EX. They may trade in a futures contract, and at the same time trade in the commodity that underlies the futures

contract, hoping to achieve small price gains on the difference between the two

Speculators and arbitrageurs are very important to markets because they keep the market liquid on a daily basis!

ACCOUNTING FOR DERIVATIVES

The basic principles regarding accounting for *derivatives are as follows:

1. Financial instruments (including derivatives), and certain non-financial derivatives, represent rights and

obligations that meet the definitions of assets/liabilities and should be recognized in FS when the entity

becomes party to the contract

2. Fair value is the most relevant measure

3. Gains and losses should be booked through net income

* Special optional hedge accounting exists for derivatives & other items that have been designated as being

part of a hedging relationship for accounting purposes. These are described in Appendix 6A

Non-Financial Derivatives and Executory Contracts

GAAP provides accounting guidance for financial instruments (including derivatives) as well as certain non-

financial derivatives

Are purchase companies’ derivatives? What separates the two types of contracts from a financial perspective?

→ Both purchase commitments and derivatives are labelled as executory contracts, meaning that they are

a contract to do something in the future

→ Purchase commitments are not structured as derivatives contracts from a legal perspective, however, and

they do not trade on commodities exchanges

Under ASPE, purchase commitments and similar commodities contracts are generally not accounted for as

derivatives unless they are exchange traded futures, meaning they trade on commodities exchanges

IFRS considers whether contracts have net settlement features, meaning that they can be settled on a net basis

by paying cash or other assets as opposed to taking delivery of the underlying product

→ For contracts with net settlement features, as long as the company intends to take delivery of the raw

materials, the contracts are designated as “expected use” and are not accounted for as derivatives

→ They are not recognized until delivery of the underlying non-financial asset takes place

Options & Warrants

Option (or Warrant) – gives the holder the contractual right to acquire or sell an underlying instrument at a

specific price within a specific term

• Exercise (Strike) Price – the agreed-upon price at which the option may be settled