COMM 2102 Chapter Notes - Chapter 2: Variable Cost, Fixed Cost, Income Statement

4 Apr 2016

School

Department

Course

Professor

Document Summary

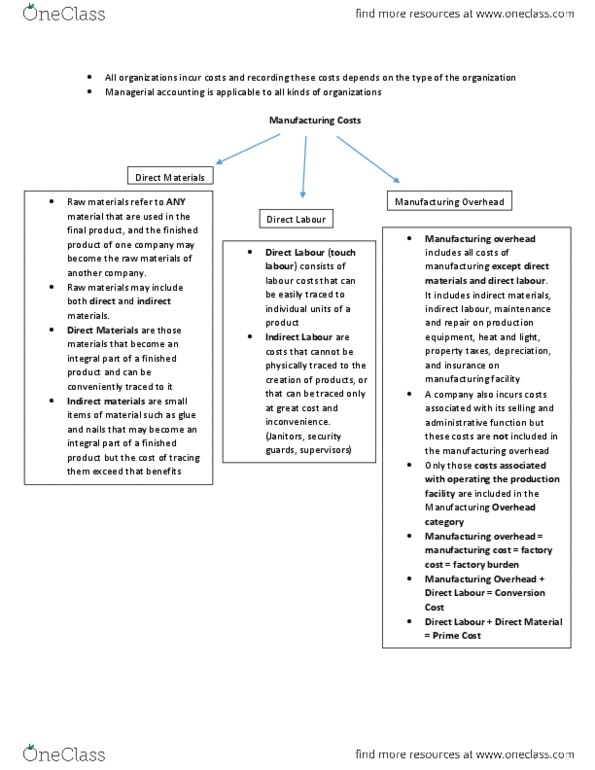

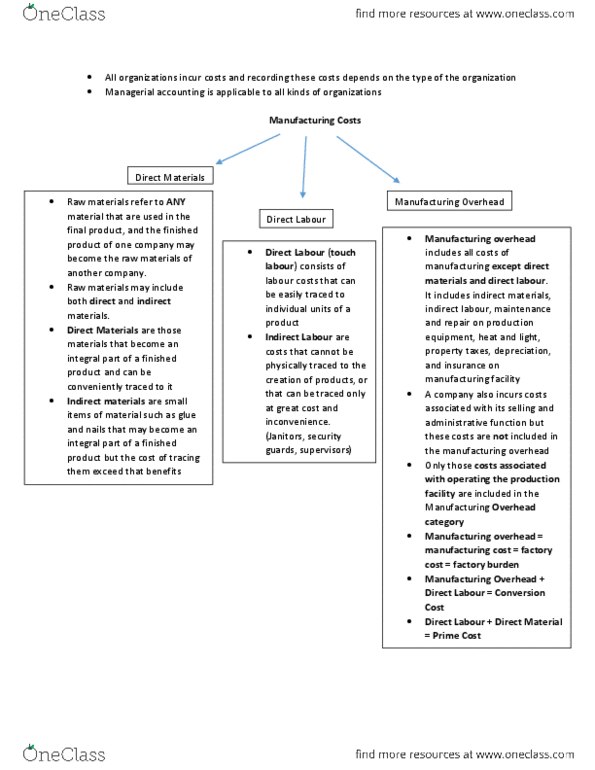

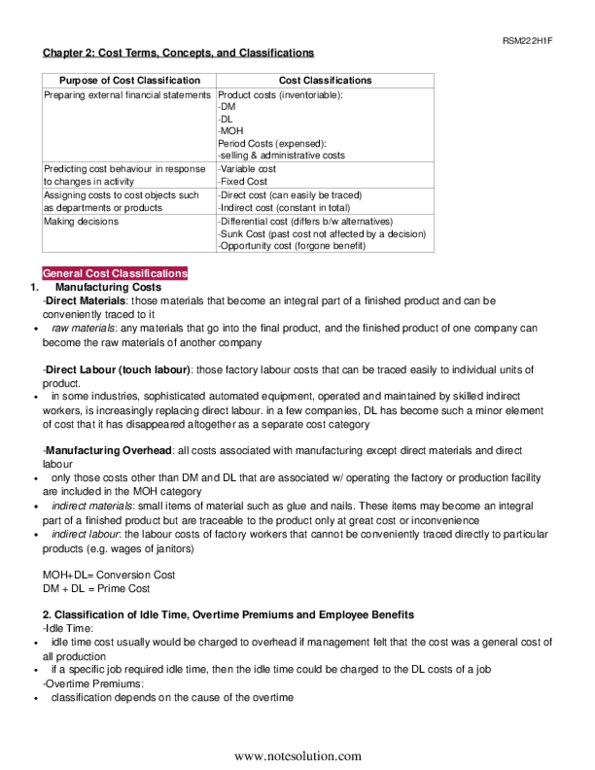

Direct materials: those materials that become an integral part of a nished product and can be conveniently traced to it. Indirect materials: small items of material that may become an integral part of a. Nished product but whose costs of tracing exceed the bene ts. Direct labour: those factory labour costs than can be traced easily to individual units of product. Indirect labour: the labour costs of janitors, supervisors, material handlers, and other factory workers that cannot be conveniently traced directly to particular products. Manufacturing overhead (moh): all costs associated with manufacturing except direct materials and direct labour. Prime cost: direct materials cost plus direct labour cost. Marketing or selling costs: all costs necessary to secure customer orders and get the. Administrative costs: all executive, organizational, and clerical costs associated with the general management of an organization rather than with manufacturing, marketing, or selling. Product costs: all costs that are involved in the purchase or manufacture of goods.