FINA 395 Chapter Notes - Chapter 6: Financial Instrument, Preferred Stock, Ticker Tape

25 Jan 2015

School

Department

Course

Professor

Document Summary

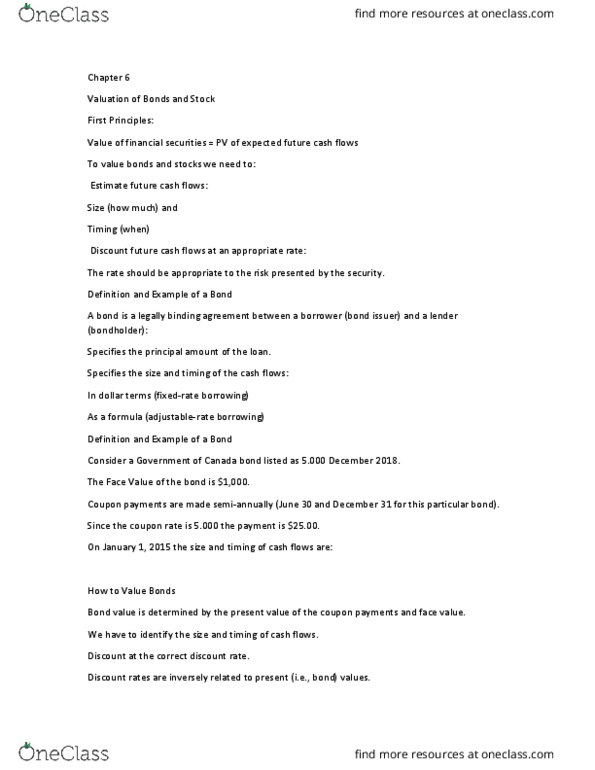

Chapter 6: how to value bonds and stocks. 6. 1 the price of a pure discount (zero coupon) bond is the present value of the par. Remember, even though there are no coupon payments, the periods are semiannual to stay consistent with coupon bond payments. So, the price of the bond for each ytm is: pv = ,000/(1+0. 05/2)20 = . 27, pv = ,000/(1+0. 10/2)20 = . 89, pv = ,000/(1+0. 15/2)20 = . 41. 6. 2 the price of any bond is the pv of the interest payment, plus the pv of the par value. The price of the bond at each ytm will be: pv = ({1 [1/(1+0. 035)]50 }/0. 035) + ,000[1/(1+0. 035)50] When the ytm and the coupon rate are equal, the bond will sell at par: pv = ({1 [1/(1+0. 045)]50 }/0. 045) + ,000[1/(1+0. 045)50] When the ytm is greater than the coupon rate, the bond will sell at a discount: pv = ({1 [1/(1+0. 025)]50 }/0. 025) + ,000[1/(1+0. 025)50]