BUSI 4005 Chapter Notes - Chapter 16: Capital Loss

19 May 2018

School

Department

Course

Professor

Income deferral

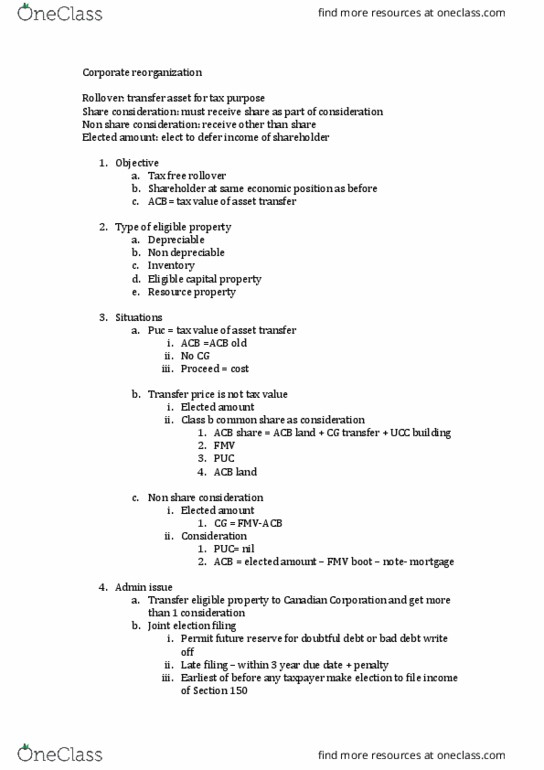

1. Section 85

a. Exchange of share- allow tax free rollover for exchange share with other

corporation

b. Vendor

i. Do’t recogize CG/ CL

ii. Prior exchage there’s ar legth deal

iii. Transfer share = capital property

c. Purchaser

i. Canadian corporation

ii. After exchange, vendor and non arm length person no control purchaser

d. Consequence

i. Cost = lesser of FMV or PUC

ii. Proceed = ACB

iii. ACB new = ACB old

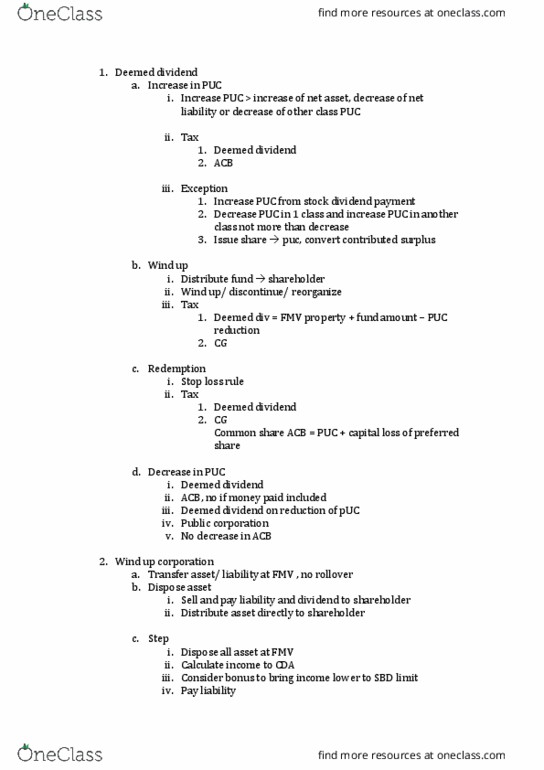

2. Section 86

a. Reorganization of capital – allow tax free rollover of share to new class of share

b. Condition

i. Shares are capital property

ii. Do’t iclude all shareholder

iii. Property receivable include other shares

iv. Total share of n class own by shareholder

c. Steps

i. Issuance of new share

ii. Redemption of old share

iii. Benefit rule on gift, proceed = lesser of FMV non share consideration gift

amount or FMV old share

3. Section 87

a. Amalgamation – tax free rollover in merger

b. Condition

i. Total property + liability belong to new corporation

ii. Exchange share get CG deferral

iii. Shareholder must get share of new corporation

c. Consequence

i. Tax value of asset = total predecessor corporation tax value of asset

ii. Deemed tax year end for predecessor

iii. Choke of new tax year end

iv. Bump in ACB

d. Major rollover provision

find more resources at oneclass.com

find more resources at oneclass.com