BUSI 2503 Chapter Notes -Quick Ratio, Accounts Receivable, Current Yield

28 Dec 2014

School

Department

Course

Professor

Document Summary

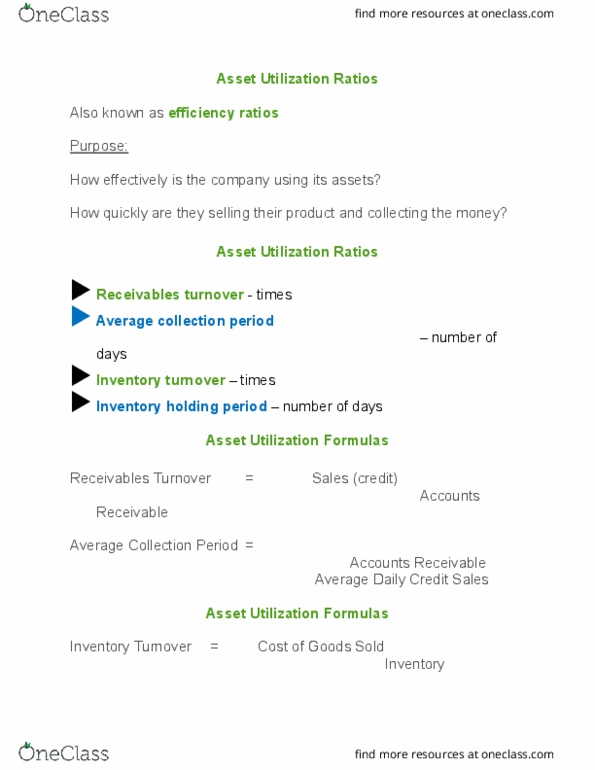

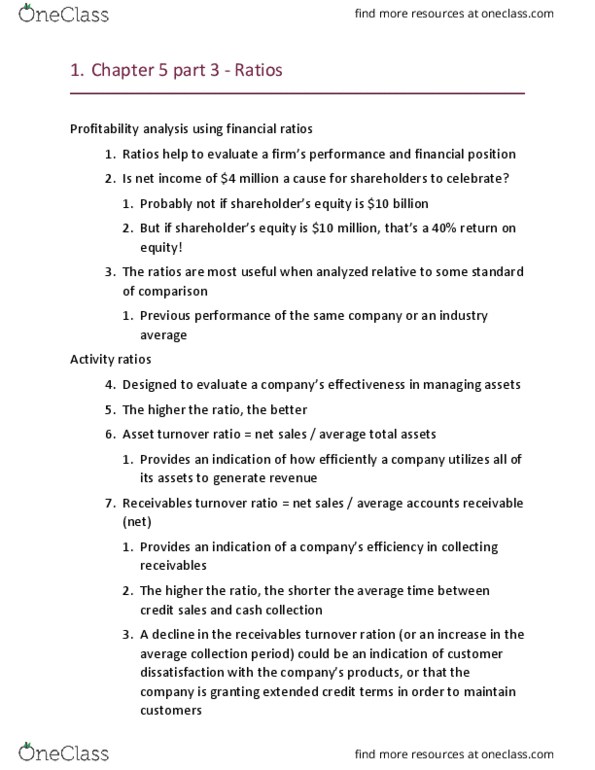

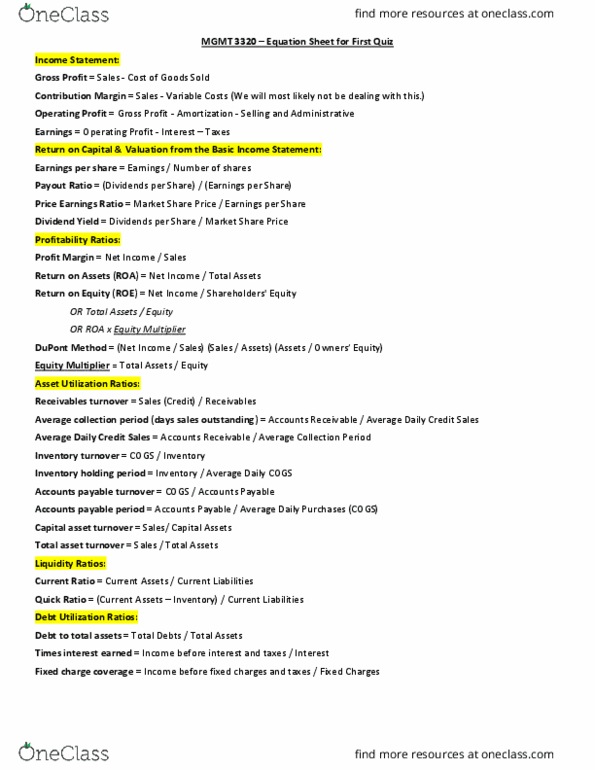

Explain why one firm can turnover its assets quicker than another. Relate the balance sheet (assets) to the income statements (sales) Firms generally want higher turnover ratios because they indicate assets are being used efficiently to generate sales. If turnover ratios slow down, inventory may become obsolete or accounts receivable may turn into bad debts. Too rapid turnover of assets may indicate a lack of capital to fund assets. Sometimes ratios calculated using an average of the balance sheet between 2 points to avoid distortions. Lowering collection period can hurt credit sales. Inventory turnover = cost of goods sold or sales . Accounts payable turnover = cost of goods sold. Deteriorating liquidity ratios often stem from weakening asset utilization ratios. Liquidity allows a business to remain flexible and meet short term obligations (i. e. bills) A current ratio of 2. 0+ and quick ratio of 1. 0+ are generally acceptable.