ACTG 4P11 Chapter Notes - Chapter 12: Moral Hazard, Adverse Selection, Information Asymmetry

Document Summary

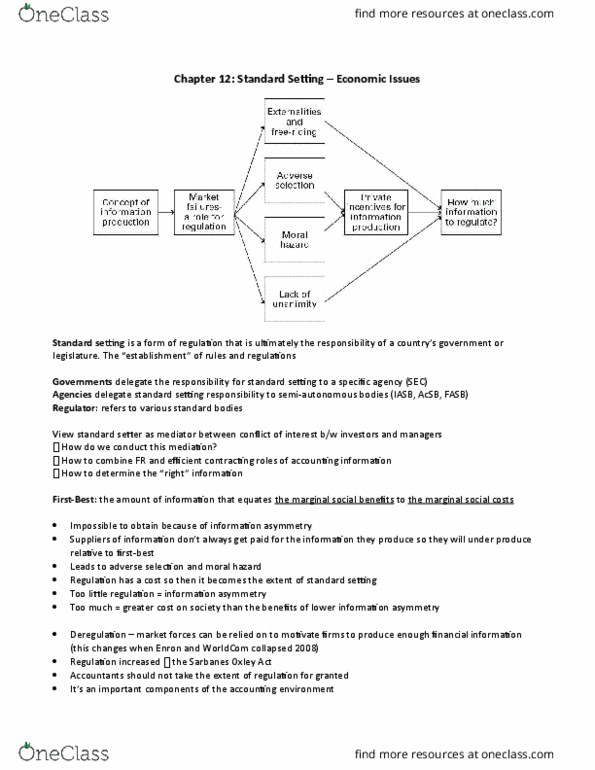

Information asymmetry between firms and investigators is mitigated by disclosure. Financial disclosure is regulated by public bodies (government agencies) and private bodies (stock exchanges, acsb, fasb) Accountants should not take the extent of regulation for granted. Information as a commodity: demand: information demanded by decision makers, supply: information supplied by firms, managers, analysts. From society"s perspective, firms should produce information until the marginal social benefit equals marginal social cost. In practice, firms face a mixture of private and regulatory incentives to produce information. Proprietary information information that, if released, would directly affect future cash flows of the firm. Non-proprietary information information that, if released, does not directly affect firm cash flows. Sources of regulation in financial report: professional accounting bodies (code of ethics, discipline committees, standard setters, gaap, securities commissions. Finer information expanded note disclosure, additional line items. Additional information current value accounting, md&a. Credible information big four audit is more credible than a non-big four audit.