ACCT3322 Chapter Notes - Chapter 2: Contributory Negligence, Engagement Letter, External Auditor

Document Summary

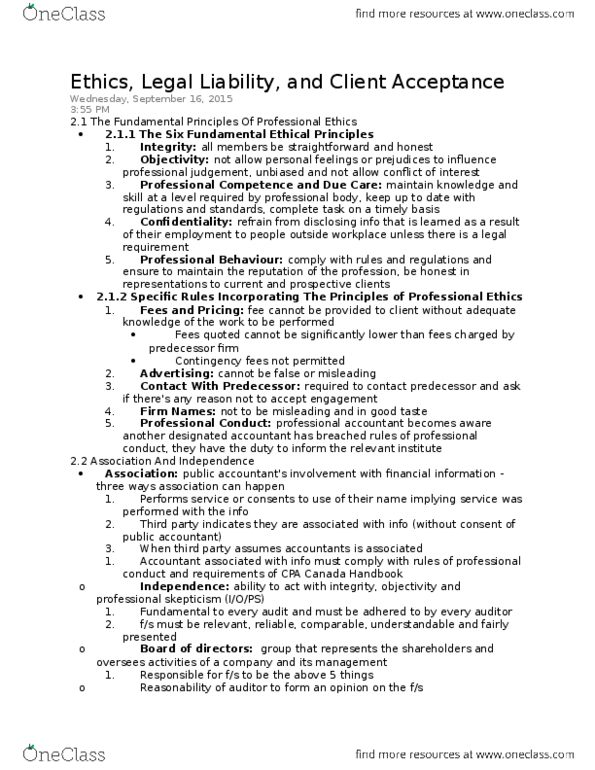

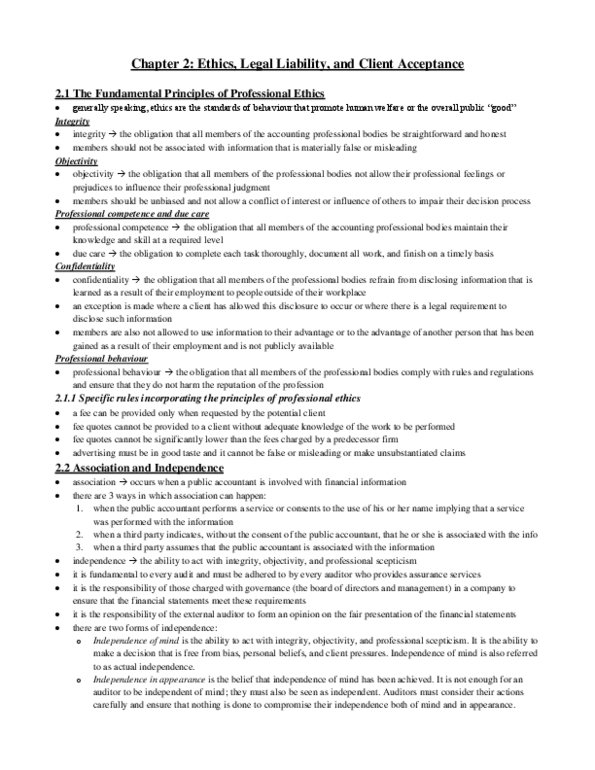

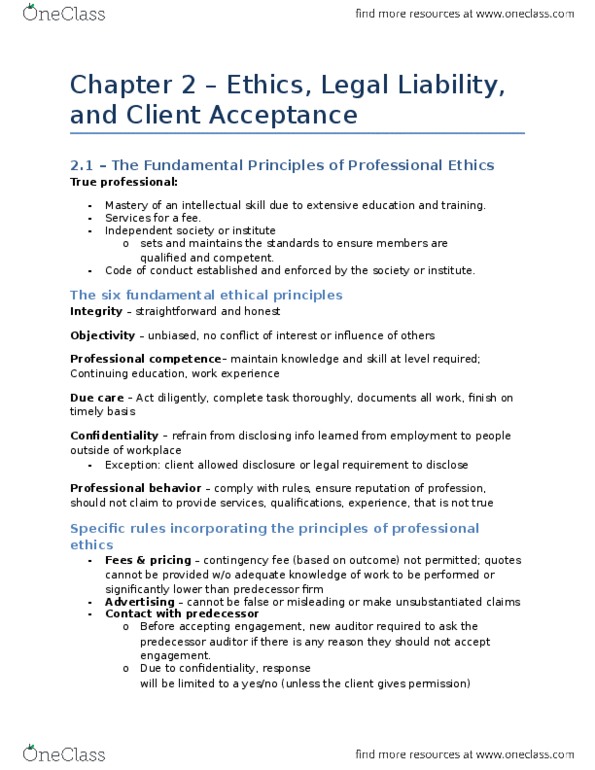

Chapter 2: ethics, legal liability and client acceptance. 2. 1 explain the fundamental principles of professional ethics. 2. 3 describe the relationship between an auditor and key groups they have a professional link with during the audit engagement. 2. 4 illustrate the auditor"s legal lia(cid:271)ilit(cid:455) to their (cid:272)lie(cid:374)t, (cid:272)o(cid:374)tri(cid:271)utor(cid:455) (cid:374)eglige(cid:374)(cid:272)e a(cid:374)d the extent to which an auditor is liable to third parties. 2. 5 categorise the factors to consider the client acceptance or continuance decision. It is the responsibility of every member of the accountancy profession to act in the public interest: this means that members should be mindful of how their actions affect others. 2. 1. 1 integrity: refers to the obligation that all members of the professional bodies be straightforward and honest, members should not be associated with information that is materially false or misleading. Acct3322, s2 2018: members should consult with senior staff in their organisation when faced with an issue that threatens their conformity with the fundamental principles.