ACCT2331 Chapter 23: Chapter 23

Document Summary

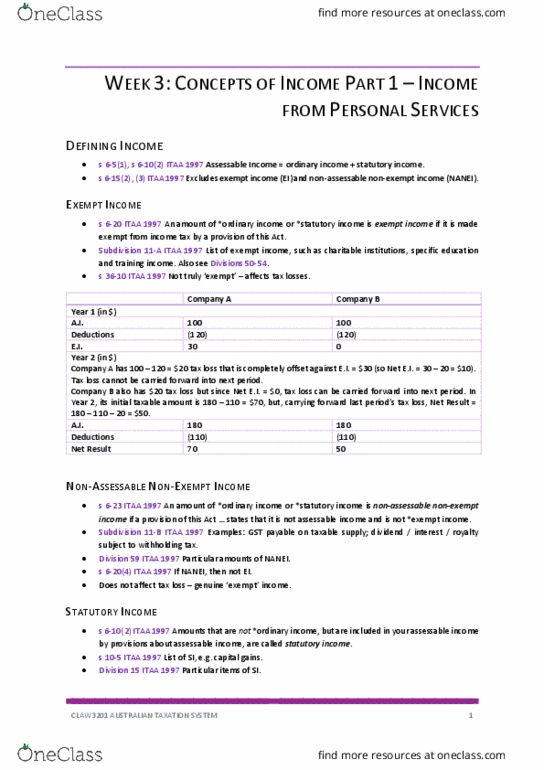

23. 1 tax losses (div 36 itaa97: a tax loss can be carried forward into subsequent income years and claimed as a. Deduction" (note: not tax offset: div 36 is subject to special restriction (div 165 and sch 2f in itaaa36) to prevent taxpayers trafficking in corporate and trust losses. Amount of tax loss [p644: calculated under s 36-10 itaa97, tax loss = deduction for income year" less (assessable income + net exempt income)". Net exempt income" is the amount by which exempt income from all sources exceed: Non capital losses and outgoings incurred in deriving their exempt income, and. Any foreign taxes payable on their exempt income. Limitation on amount of tax loss [p645: section 26-55 itaa97 prevents deductions under certain provisions from adding to the amount of a tax loss, including: Deduction of tax losses (individuals) [p645: non-corporate tax entities (eg individuals):