BUSS1030 Chapter Notes - Chapter 4: Accounting Information System, Capital Account, Financial Statement

28 May 2018

School

Department

Course

Professor

CHAPTER 4: COMPLETING THE ACCOUNTING CYCLE

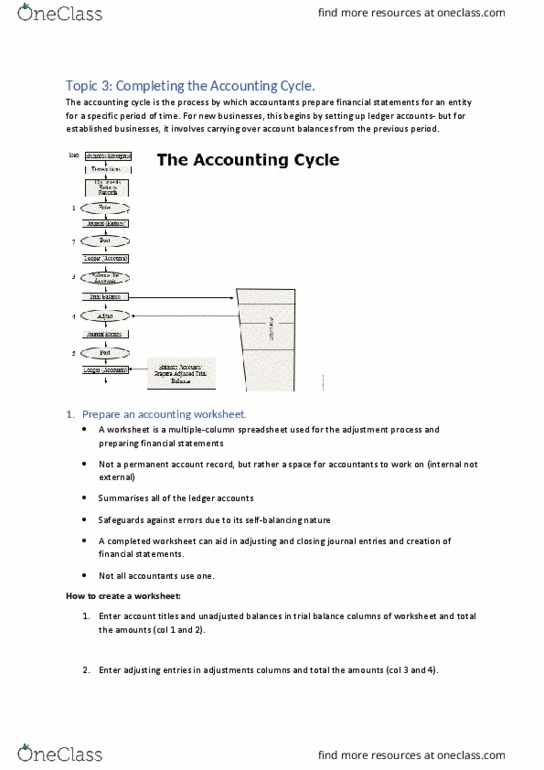

• The accounting cycle starts with the beginning A, L and OE account balances left over from the preceding period

THE ACCOUNTING WORKSHEET

• Worksheet: a tool used to assemble all information required to adjust accounts and prepare interim financial

statements à not a substitute for journals or ledgers, DOES not form part of financial statements

o Used for internal decision making

• Steps:

o Enter account titles and unadjusted balances in Trial Balance columns of worksheet + total amounts

§ Data comes from ledgers before adjustments

§ Listed in decreasing order of liquidity (cash, accounts receivable etc.)

§ Order: A, L, OE, Revenues, Expenses

o Enter adjusting entries in adjustments columns + total amounts

o Calculate each account’s adjusted balance by combining trial balance + adjustment figures à enter in

adjusted trial balance columns

o Extend adjustment balances of revenue + expense accounts to income columns and remaining items to the

balance sheet columns

o On the income statement, calculate profit or loss as total revenues – total expenses

§ Enter profit/loss as balancing amount on income statement

§ Also enter profit/loss as balancing amount on balance sheet

§ Total financial statement columns

COMPLETING THE ACCOUNTING CYCLE

• Closing the accounts (end of accounting year)

o Transfer revenue, expense + drawing balances to capital

account for next period

§ Intermediary step: Income summary account to see

profit/loss

• Post-closing trial balance (optional)

o Only A, L, Capital

• Classifying assets and liabilities

o A + L are usually classified in balance sheets as current or non-

current

o Usually list A + L in order of decreasing liquidity (how quickly an item can be converted to cash)

STEPS IN PREPARING FINANCIAL STATEMENTS

1. Prepare the worksheet

2. Adjusting entries

3. Calculate adjusted General Ledger balances

4. Identify the items to show on each financial statement

5. Calculate profit (revenue > expenses)

Steps Completed Monthly

Steps Completed at the End of Each Financial Period

- Identify (new) transactions

- Record transactions in Journal

- Post Journal to General Ledger

- Prepare a Trial Balance

- Prepare internal management reports if needed

- End-of-period adjustments

- Prepare Adjusted Trial Balance

- Prepare Financial Statements

Document Summary

The accounting cycle starts with the beginning a, l and oe account balances left over from the preceding period. Steps: enter account titles and unadjusted balances in trial balance columns of worksheet + total amounts. Listed in decreasing order of liquidity (cash, accounts receivable etc. ) Enter profit/loss as balancing amount on income statement. Also enter profit/loss as balancing amount on balance sheet. Completing the accounting cycle: closing the accounts (end of accounting year, transfer revenue, expense + drawing balances to capital account for next period. Intermediary step: income summary account to see profit/loss. Steps in preparing financial statements: prepare the worksheet, adjusting entries, calculate adjusted general ledger balances, calculate profit (revenue > expenses) Identify the items to show on each financial statement. Steps completed at the end of each financial period.