FINS2624 Chapter Notes - Chapter 6-8: Risk Premium, Risk Aversion, Indifference Curve

Chapter 6

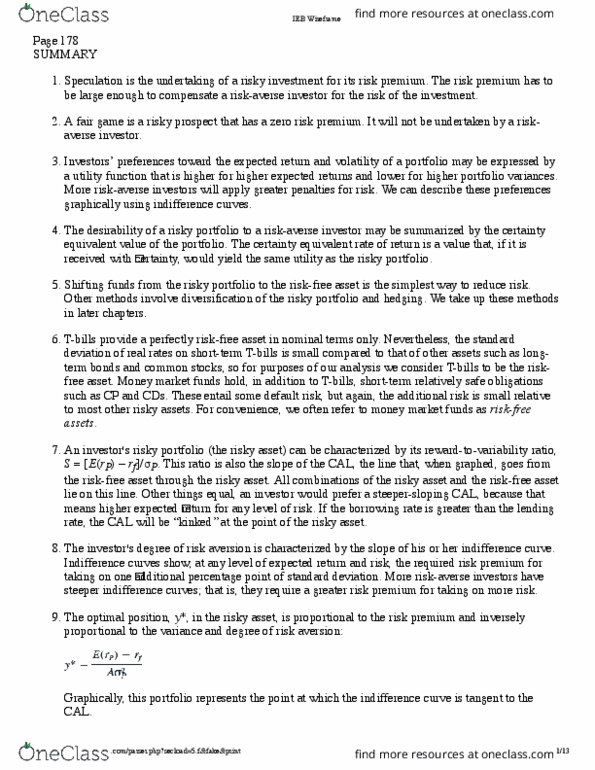

- Speculation is the undertaking of a risky investment for its risk premium. The risk

premium has to be large enough to compensate a risk-averse investor for the risk of

the investment.

- A fair game is a risky prospect that has a zero risk premium. It will not be undertaken

by a risk-averse investor

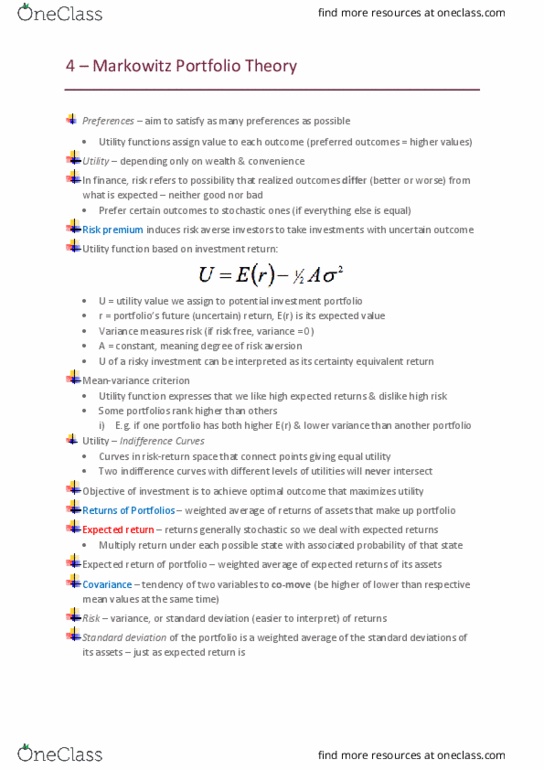

- Iestors’ preferees toard the epeted retur ad olatilit of a portfolio a

be expressed by a utility function that is higher for higher expected returns and

lower for higher portfolio variances. More risk-averse investors will apply greater

penalties for risk. We can describe these preferences graphically using indifference

curves.

- The desirability of a risky portfolio. The certainty equivalent rate of return is a value

that, if it is received with certainty, would yield the same utility as the risky portfolio

- Shifting funds from the risky portfolio to the risk-free asset is the simplest way to

reduce risk. Other methods involve diversification of the risky portfolio and hedging

- An investor’s risk portfolio risk asset a e haraterised its reard-to-

volatility, S = (E(rP) – rf)/ σP . This ratio is also the slope of the CAL, a line that goes

from the risk free asset through the risky asset. Other things equal, an investor

would prefer a steeper-sloping CAL, because that means higher expected return for

any level of risk. If the borrowing rate is greater than the lending rate, the CAL will be

kinked at the point of the risky asset

- The investors degree of risk aversion is characterised by the slope of their

indifference curve. Indifference curves show, at any level of expected return and

risk, the required risk premium for taking on one additional percentage point of

standard deviation. More risk-averse investors have steeper indifference curves-

require greater risk premium for taking on more risk

- Optimal position y* in risky asset is proportional to risk premium and inversely

proportional to variance and degree of risk aversion: y* = (E(rP) – rf/A*σP2 → point

at which indifference curve is tangent to CAL

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Speculation is the undertaking of a risky investment for its risk premium. The risk premium has to be large enough to compensate a risk-averse investor for the risk of the investment. A fair game is a risky prospect that has a zero risk premium. It will not be undertaken by a risk-averse investor. I(cid:374)(cid:448)estors" prefere(cid:374)(cid:272)es to(cid:449)ard the e(cid:454)pe(cid:272)ted retur(cid:374) a(cid:374)d (cid:448)olatilit(cid:455) of a portfolio (cid:373)a(cid:455) be expressed by a utility function that is higher for higher expected returns and lower for higher portfolio variances. More risk-averse investors will apply greater penalties for risk. We can describe these preferences graphically using indifference curves. The certainty equivalent rate of return is a value that, if it is received with certainty, would yield the same utility as the risky portfolio. Shifting funds from the risky portfolio to the risk-free asset is the simplest way to reduce risk. Other methods involve diversification of the risky portfolio and hedging.