ECON1101 Chapter Notes - Chapter 7: Aggregate Supply, Marginal Utility, Marginal Cost

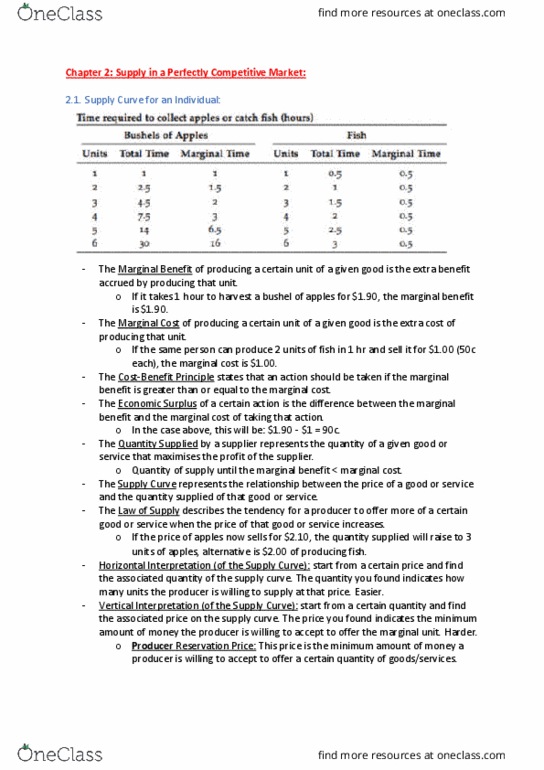

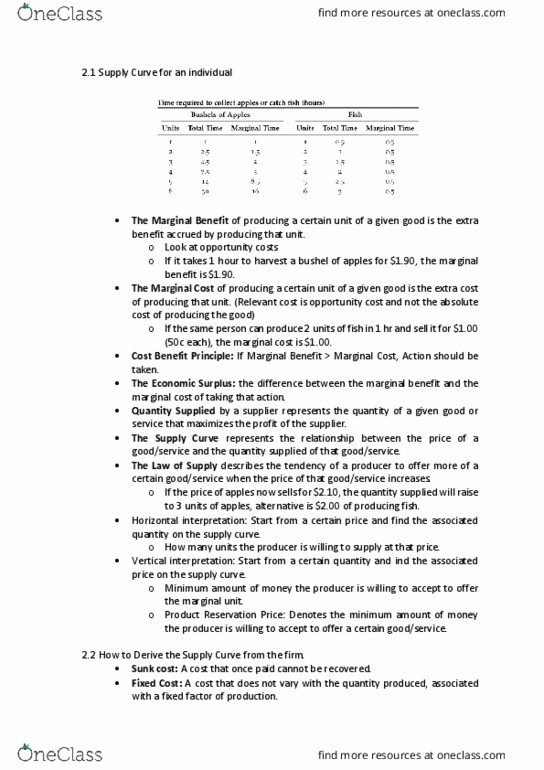

Marginal Benefit: Producing a certain unit of a given good is the extra benefit

accrued by producing that unit.

Marginal Cost: Extra cost of producing that unit (relevant cost is the "opportunity

cost")

Cost-Benefit Principle: States that an action should be taken if the marginal benefit

is greater than the marginal cost.

Economic Surplus: Difference between the marginal benefit and the marginal cost

of taking that action.

Quantity supplied: Represents the quantity of a given good or service that

maximises the profit of the supplier.

Supply Curve: Represents the relationship between the price of a good or service

and the quantity supplied of that good or service.

Law Of Supply: Describes the tendency for a producer to offer more of a certain

good or service when the price of that good or service increases.

Horizontal Interpretation (of the Supply Curve): Start from a certain price and find

the associated quantity on the supply curve. The quantity you found indicates how

many units the producer is willing to supply at that price.

Vertical Interpretation (of the Supply Curve): Start from a certain quantity (say 2

units) and find the associated price on the supply curve. The price you found

indicates the minimum amount of money the producer is willing to accept to offer

the marginal unit (in our example the marginal unit would be the 2nd unit).

Producer Reservation Price: Denotes the minimum amount of money the

producer is willing to accept to offer a certain good or service.

The period of time when at least one factor of production is fixed is denoted

as the short run.

-

Long run is the period of time when all factors of production are variable.

-

Average Variable Cost = Variable cost/ Quantity

-

Average Total Cost = Total cost/ Quantity

-

Marginal cost = Change in total cost/change in variable cost

-

Hereafter we assume that when the entrepreneur is indifferent, she decides

to produce.

-

Suppose now we are in the long run and the entrepreneur can decide whether or

not to start a new loan to rent the machinery once more ---> no sink cost --> gains

nothing but also loses nothing by exiting.

Sunk Cost: A sunk cost is a cost that once paid cannot be recovered.

Fixed factor of production: If factor of production is fixed, then the cost associated

with it does not vary with the quantity produced.

Fixed cost: A fixed cost is a cost associated with a fixed factor of production

Short run: Denotes a period of time during which at least of one factor of

production is fixed

Variable factor of production: Cost associated with it tends to vary with the

number of units produced.

Long run: Denotes a period of time during which all factor of production are

variable.

Profit: Represents the difference between the total revenues (TR) and the total

costs (TC)

Shut Down Condition (short run): In the short run, the entrepreneur should shut

down production if production < -FC. Otherwise, she should hire the optimal

number of workers and continue operations.

Exit Condition (long run): In the long run, the entrepreneur should exit the industry

if production < 0. Otherwise she should hire the optimal number of workers and

continue operations.

Supply curve for a firm can be derived by changing the price and observe the

variation in quantity produced. In the context of the firm, the supply curve is

equal to the Marginal Cost (MC) curve only for those values of the MC that

are higher than the minimum AVC (in the short run) and higher than the

minimum ATC (in the long run) --> Entrepreneur will not produce anything if

the price is below these points in short run and long run respectively.

-

The marginal cost curve eventually increases with the quantity produced. The

production process is subject to increasing marginal costs. This might be due

to the fact that adding more employees operating on a fixed amount of

machineries translates sooner or later into a productivity decline because, for

example, the employees might get in each other's way while operating the

equipment.

-

The marginal cost curve cuts the AVC curve and the ATC curve at their

minimum points. (Marginal cost = extra cost associated with the production

of the extra unit of the good) If the extra cost is smaller than the average cost,

then the average will decrease. If the extra cost is higher than the average

cost, average will increase. Average remains constant if and only if the

marginal cost = average cost. Hence, AVC and ATC curve decrease initially as

the MC curve is below them and continue to do so until the point MC curve

meets them as from that point onwards MC curve is above them, they begin

to increase.

-

A change in the market price determines the movement along the supply

curve whereas a change in some other factor than the price that affects MC

will shift the ENTIRE supply curve.

-

Factors shifting the supply curve could be: (1) Technology - more advanced

technologies reduce the unit cost of production (2) Input prices - a change in

the price of inputs will affect the productive capacity of a firm/industry,

reflecting directly in supply (3) Expectations - Expected future price will make

suppliers adjust their behaviour to take advantage of new opportunities. (4)

Change in pricing for other products - If a seller is producing two or more

goods, and one good experiences a surge in demand, the seller will shift

productive focus to it. (5) Number of suppliers - Higher the number of

suppliers entering the market, the larger the right shift in the aggregate

supply curve.

-

Supply in a Perfectly Competitive Market

Wednesday, 4 April 2018

9:09 pm