FNCE30007 Chapter Notes - Chapter 12: Arbitrage, Discount Window, Cash Flow

29 Jun 2020

School

Department

Course

Professor

Document Summary

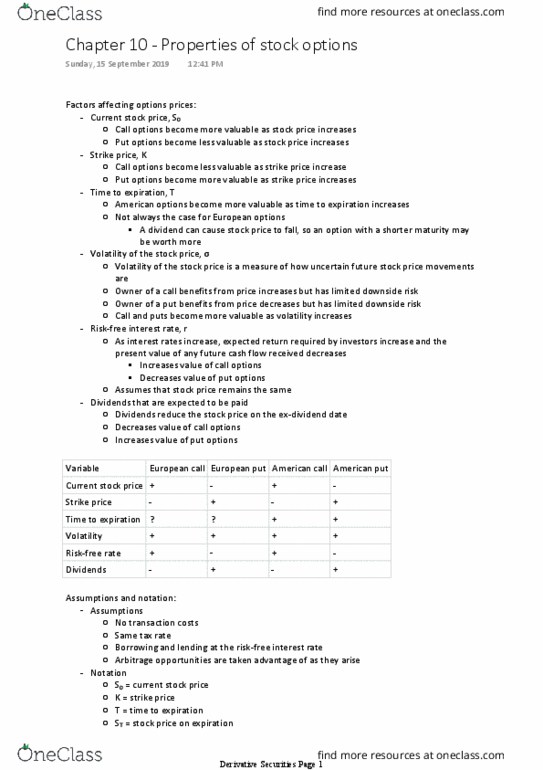

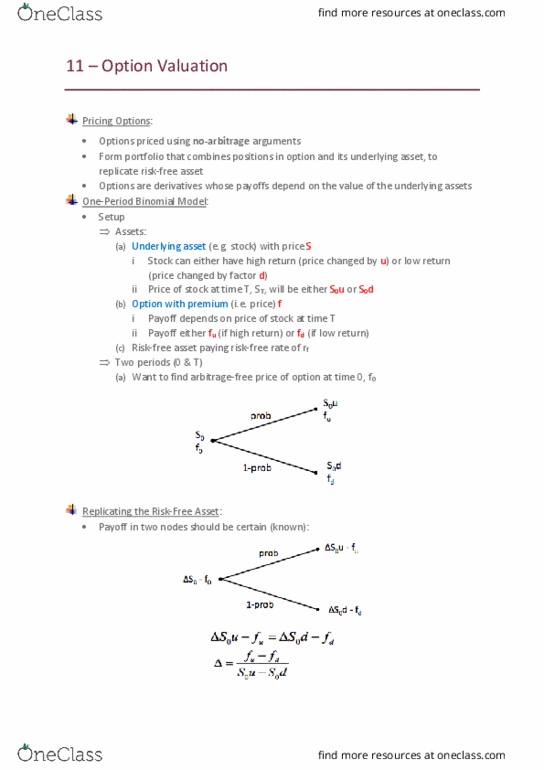

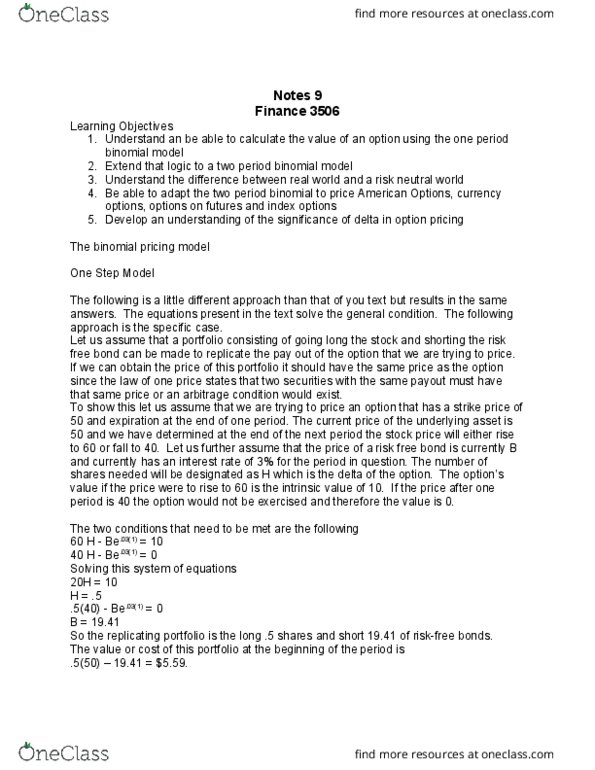

Expectation pricing framework = expected value of future cash flow streams discounted at an appropriate rate of return which compensates for the risk of that particular asset. No arbitrage = construct a replicating portfolio whose payoff replicates the payoff of the asset being valued. Assume investors are risk-neutral when valuing a derivative. Expected return on a stock is the risk-free rate. Discount rate used for the expected payoff on an option is the risk-free rate. Value at earlier nodes is the greater of. Delta = ratio of the change in the price of the stock option to the change in the price of the underlying stock.