ACCT10002 Chapter Notes - Chapter 4: Perpetual Inventory, Accounts Payable, Gross Profit

22 May 2018

School

Department

Course

Professor

Main source of revenues for merchandising businesses is the sale of inventory

-

sales revenue/sales

Expenses are divided into two categories

-

cost of sales and operating expenses

Cost of sales is the total cost of inventory sold during the period

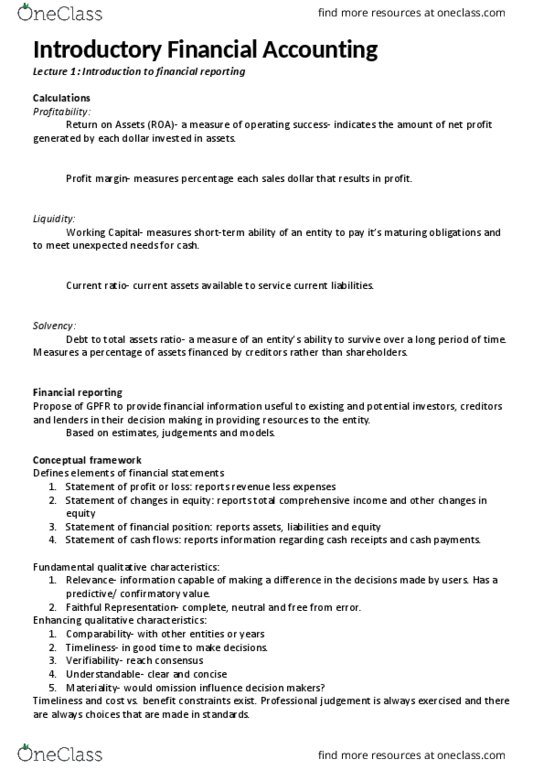

Sales revenue

-

cost of sales = gross profit

-

Gross profit

-

operating expenses = net profit

-

Profit measurement process for a merchandising business:

Sales revenue

-

operating expenses = profit

-

Profit measurement process for a service business:

The operating cycle of a merchandising business is longer than that of a service business

Perpetual inventory system:

Detailed records of the cost of each inventory purchase and sale are maintained

Use of bar codes and optical scanners to keep a daily running record

Cost of sales is determined each time a sale occurs

Periodic inventory system:

Determine the cost of goods on hand at the beginning of the accounting period

1.

Add to it the cost of goods purchased

2.

Subtract the cost of goods on hand at the end of the accounting period

3.

Cost of sales is determined only at the end of the accounting period, when a physical inventory count

(stocktake) is taken to determine the quantity and cost of goods on hand

Computerised inventory systems keep up

-

to

-

the

-

minute records

Integrated inventory systems are linked with accounts payable and purchases and with accounts

receivable and sales to record the number of units purchased, number of units sold and quantities of

goods on hand

Having the most current inventory information assists managers in making decisions about when to

replenish and re

-

order inventory

Perpetual vs periodic:

Shortages can be investigated immediately

-

Perpetual provides better control

Perpetual requires additional clerical work and additional cost, but a computerised system can minimise

the cost

Small businesses may find it unnecessary or uneconomical to invest in a computerised perpetual

inventory system

Merchandising operations

Tuesday, 22 August 2017 4:16 PM

IFA Page 1

Cash purchases are recorded by an increase in inventory and a decrease in cash

States the quantity and cost of each item supplied, the total purchase price and the terms of

payment

-

Credit purchases are supported by a supplier's invoice which evidences the supplier's claim against the

purchaser

Credit purchases are recorded by an increase in inventory and an increase in accounts payable

Credit terms of 2/7, n/30 indicate a 2% discount if paid within 7 days, otherwise full invoice amount is

due in 30 days

A purchase return occurs when the purchaser returns the goods for credit or a cash refund

A purchase allowance occurs when the purchaser keeps the inventory if the seller is willing to grant an

allowance/a deduction from the purchase price

Freight

-

in costs occur when the buyer pays the transport costs and are considered part of the cost of

purchasing inventory

Freight

-

in costs are recorded by an increase in freight

-

in and a decrease in cash

Freight

-

out costs occur when the seller pays the transport costs on outgoing inventory

Freight

-

out costs are recorded by an increase in freight

-

out and a decrease in cash

Settlement discounts permit the buyer to claim a discount for prompt payment

Discounts are recorded by the buyer as revenue

Eg. decrease in accounts payable, decrease in cash, increase in discount received

Or decrease in accounts payable, decrease in cash, decrease in inventory

Trade discounts do not depend on early payment and are not recorded

Trade discounts are disclosed on the sales invoice as a percentage reduction in the list price of the

inventories sold

Eg. trade discount for buyers who purchase in large quantities

Recording purchases of inventories

Tuesday, 22 August 2017 4:16 PM

IFA Page 2

Document Summary

Main source of revenues for merchandising businesses is the sale of inventory - sales revenue/sales. Expenses are divided into two categories - cost of sales and operating expenses. Cost of sales is the total cost of inventory sold during the period. Sales revenue - cost of sales = gross profit. Gross profit - operating expenses = net profit. The operating cycle of a merchandising business is longer than that of a service business. Detailed records of the cost of each inventory purchase and sale are maintained. Use of bar codes and optical scanners to keep a daily running record. Cost of sales is determined each time a sale occurs. Cost of sales is determined only at the end of the accounting period, when a physical inventory count (stocktake) is taken to determine the quantity and cost of goods on hand. Determine the cost of goods on hand at the beginning of the accounting period.