ACCT10001 Chapter Notes - Chapter 7: Corporate Finance, Cash Cash, Operating Cash Flow

22 May 2018

School

Department

Course

Professor

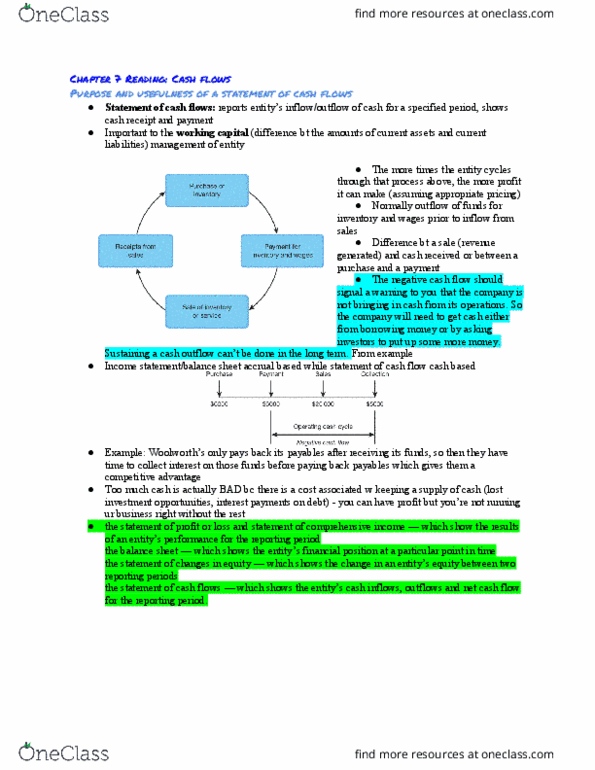

Purpose = report the cash flows of a business

Working capital is needed to fund inventory and accounts receivable while awaiting receipts

-

Flows of cash are important for working capital management

Flow of cash:

Purchase of inventory

-

> payment for inventory and wages

-

> sale of inventory or service

-

> receipts

from sales

-

> purchase of inventory

More times an entity can cycle through process

-

> more profit

Cash is important as there is often an outflow of funds for inventory and wages prior to inflow from

sales

Statement of cash flows ascertains cash generation from this cycle and whether or not entity is

collecting receipts in a timely manner

Statement of cash flows shows actual cash receipts and payments

Difference between cash and accrual accounting:

Statement of cash flows is concerned with cash receipts and payments, not timing of underlying

transaction

Prepared on cash basis (whereas statement of profit or loss and balance sheet are prepared on

accrual basis)

Importance of cash to ongoing survival of business cannot be overstated

Entity needs to have enough cash to ensure it can meet financial obligations, but not too much since

there are costs associated with keeping a supply of read cash

Ability of entity to manage flow of cash in and out of business is critical for success

Relationship of the statement of cash flows to other financial statements:

Statement of cash flows was introduced because statement of profit or loss and balance sheet did

not provide a complete picture of entity's economic activities

Statement of cash flows gives information additional to that provided by other statements

Generate cash flows

-

Meet financial commitments as they fall due, incl. servicing of borrowings and payment of

dividends

-

Fund changes in scope and/or nature of activities

-

Obtain external finance

-

Information provided should assist decision makers in assessing entity's ability to:

Operating activities

-

Investing activities

-

Financing activities

-

Cash inflows and outflows are grouped into activities:

Purpose and usefulness of statement of cash flows

Tuesday, 4 April 2017 12:59 PM

ARA Page 1

Cash refers to cash and cash equivalents

Cash = cash on hand and demand deposits

Cash equivalents = highly liquid investments and short

-

term borrowings that are subject to an

insignificant risk of change in value

Operating activities:

Operating activities = activities that related to provision of goods and services, and other activities

that are neither investing nor financing activities

Cash sale of goods or services

-

Cash received from customers

-

Receipt of interest or dividends

-

Cash inflows:

Payments to suppliers

-

Payment of salaries and wages

-

Payment of tax and interest

-

Cash outflows:

Net cash flow from operating activities is an important measure to gauge entity's ability to generate

cash, to meet obligations, to continue as a going concern and to expand

Investing activities:

Investing activities = activities that relate to acquisition and/or disposal of non

-

current assets (PPE

and other productive assets) and investments (eg. securities) not falling within the definition of cash

Cash paid for non

-

current assets and received from sale of non

-

current assets

Sale of PPE

-

Sale of shares

-

Collection of loans from other entities

-

Cash inflows:

Purchase of PPE

-

Purchase of shares

-

Lending of money to other entities

-

Cash outflows:

Allow users to analyse entity's future direction by studying major asset acquisitions and disposals

Expect net cash flow from investing activities to be negative if entity has desire to grow

Financing activities:

Financing activities = activities that change size and/or composition of the financial structure of

entity (incl. equity) and borrowings not falling within definition of cash

Cash received from issue of own shares

-

Cash from borrowings

-

Cash inflows:

Dividends paid to shareholders

-

Repurchase of shares from shareholders

-

Repayment of borrowings

-

Cash outflows:

Reconciliation of cash from operating activities with operating profit:

Reconciliation starts with profit or loss after tax and ends with cash from operating activities

Reconciliation must be disclosed in financial statements as a note

Summary of reconciliation of profit to net cash flows:

Operating profit after tax

+ depreciation/amortisation/loss on sale of asset

-

Adjustments in non

-

cash items from statement of profit or loss

Format of the statement of cash flows

Tuesday, 4 April 2017 1:33 PM

ARA Page 2

Document Summary

Purpose a(cid:374)d useful(cid:374)ess of state(cid:373)e(cid:374)t of cash flows. Pu(cid:396)pose = (cid:396)epo(cid:396)t the (cid:272)ash flo(cid:449)s of a (cid:271)usi(cid:374)ess. Flo(cid:449)s of (cid:272)ash a(cid:396)e i(cid:373)po(cid:396)ta(cid:374)t fo(cid:396) (cid:449)o(cid:396)ki(cid:374)g (cid:272)apital (cid:373)a(cid:374)age(cid:373)e(cid:374)t. Wo(cid:396)ki(cid:374)g (cid:272)apital is (cid:374)eeded to fu(cid:374)d i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) a(cid:374)d a(cid:272)(cid:272)ou(cid:374)ts (cid:396)e(cid:272)ei(cid:448)a(cid:271)le (cid:449)hile a(cid:449)aiti(cid:374)g (cid:396)e(cid:272)eipts. Pu(cid:396)(cid:272)hase of i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) -> pa(cid:455)(cid:373)e(cid:374)t fo(cid:396) i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) a(cid:374)d (cid:449)ages -> sale of i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) o(cid:396) se(cid:396)(cid:448)i(cid:272)e -> (cid:396)e(cid:272)eipts f(cid:396)o(cid:373) sales -> pu(cid:396)(cid:272)hase of i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) Mo(cid:396)e ti(cid:373)es a(cid:374) e(cid:374)tit(cid:455) (cid:272)a(cid:374) (cid:272)(cid:455)(cid:272)le th(cid:396)ough p(cid:396)o(cid:272)ess -> (cid:373)o(cid:396)e p(cid:396)ofit. Cash is i(cid:373)po(cid:396)ta(cid:374)t as the(cid:396)e is ofte(cid:374) a(cid:374) outflo(cid:449) of fu(cid:374)ds fo(cid:396) i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) a(cid:374)d (cid:449)ages p(cid:396)io(cid:396) to i(cid:374)flo(cid:449) f(cid:396)o(cid:373) sales. State(cid:373)e(cid:374)t of (cid:272)ash flo(cid:449)s as(cid:272)e(cid:396)tai(cid:374)s (cid:272)ash ge(cid:374)e(cid:396)atio(cid:374) f(cid:396)o(cid:373) this (cid:272)(cid:455)(cid:272)le a(cid:374)d (cid:449)hethe(cid:396) o(cid:396) (cid:374)ot e(cid:374)tit(cid:455) is (cid:272)olle(cid:272)ti(cid:374)g (cid:396)e(cid:272)eipts i(cid:374) a ti(cid:373)el(cid:455) (cid:373)a(cid:374)(cid:374)e(cid:396) State(cid:373)e(cid:374)t of (cid:272)ash flo(cid:449)s sho(cid:449)s a(cid:272)tual (cid:272)ash (cid:396)e(cid:272)eipts a(cid:374)d pa(cid:455)(cid:373)e(cid:374)ts. State(cid:373)e(cid:374)t of (cid:272)ash flo(cid:449)s is (cid:272)o(cid:374)(cid:272)e(cid:396)(cid:374)ed (cid:449)ith (cid:272)ash (cid:396)e(cid:272)eipts a(cid:374)d pa(cid:455)(cid:373)e(cid:374)ts, (cid:374)ot ti(cid:373)i(cid:374)g of u(cid:374)de(cid:396)l(cid:455)i(cid:374)g t(cid:396)a(cid:374)sa(cid:272)tio(cid:374) P(cid:396)epa(cid:396)ed o(cid:374) (cid:272)ash (cid:271)asis (cid:894)(cid:449)he(cid:396)eas state(cid:373)e(cid:374)t of p(cid:396)ofit o(cid:396) loss a(cid:374)d (cid:271)ala(cid:374)(cid:272)e sheet a(cid:396)e p(cid:396)epa(cid:396)ed o(cid:374) a(cid:272)(cid:272)(cid:396)ual (cid:271)asis(cid:895)