ACCT415 Midterm: Equity Method ACCT 415 Chapter 1

8 Mar 2017

School

Department

Course

Professor

Document Summary

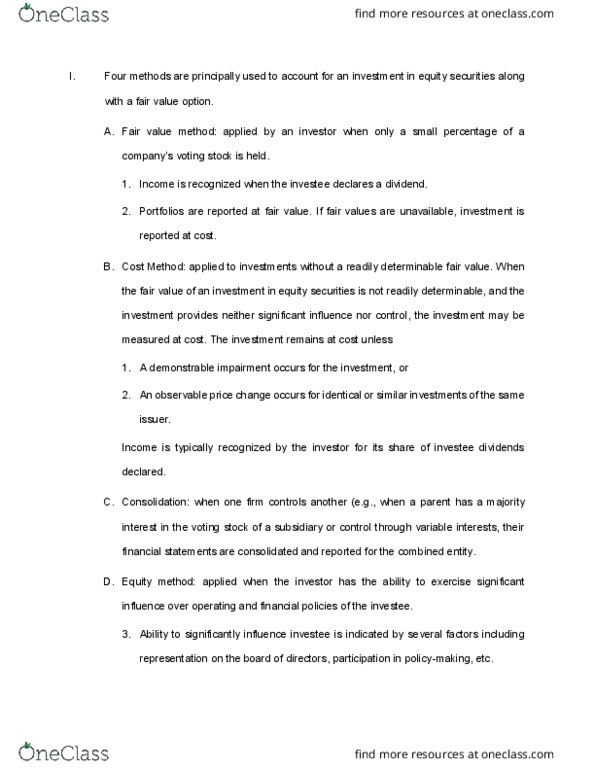

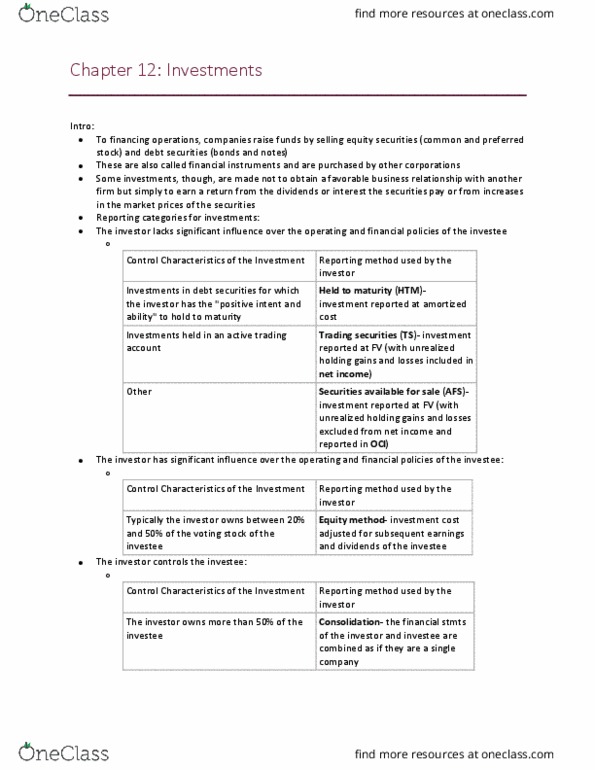

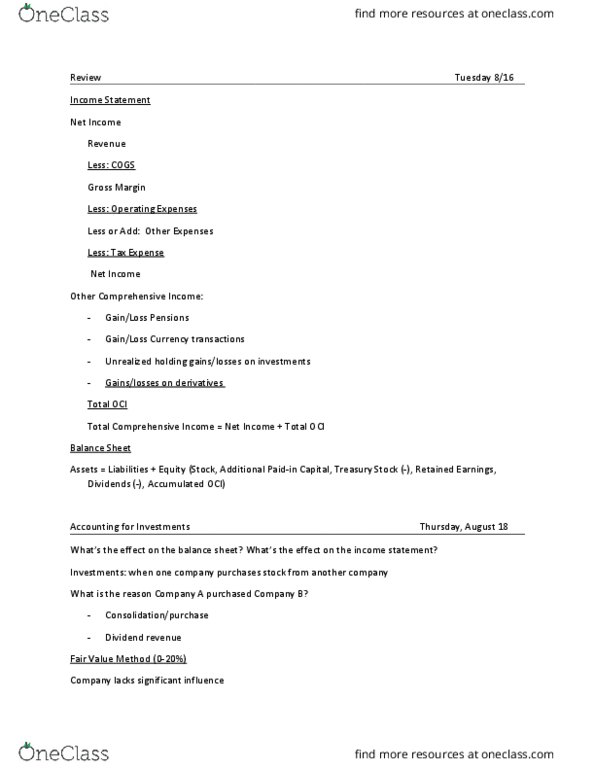

Fair-value method: when investor possesses only a small share of the invests company"s outstanding stock. These investments are recorded at cost and periodically adjusted to fair value. Includes: equity securities held for sale in the short term and classified as trading securities, equity securities not classified as trading securities called available-for- sale securities, dividends from the investments are recognized as income. Equity method: when our investment provides us with the ability to exercise significant influence over operating and financial policies of the investee (voting share majority). Not looking for control: investors share of invests dividends declared are recorded as decreases in the investment account, not as income. *if an investor holds between 20 and 50 percent of the voting stock of the invested, significant influence is normally assumed and the equity method is applied. Applying the equity method: the investors investment account increases as the invested earns and reports income.