PHYS 1061 Study Guide - Quiz Guide: Unit Root, Cointegration, Cadency

Document Summary

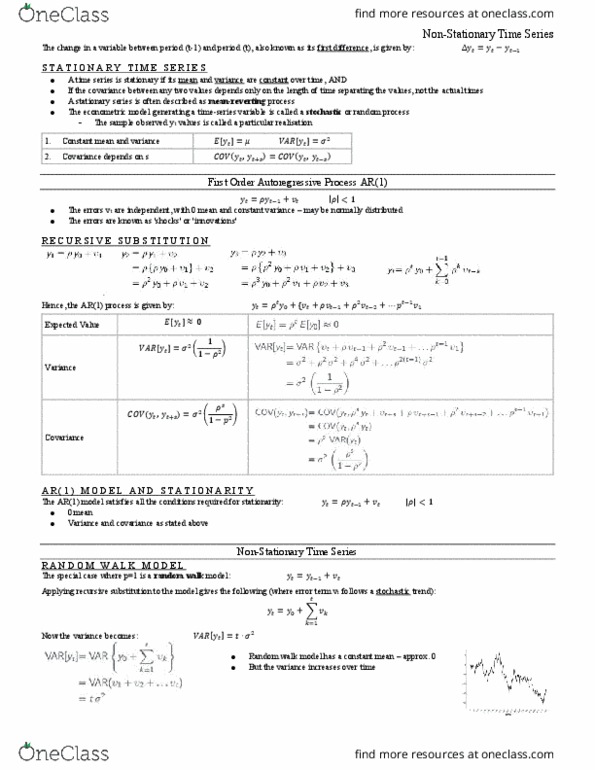

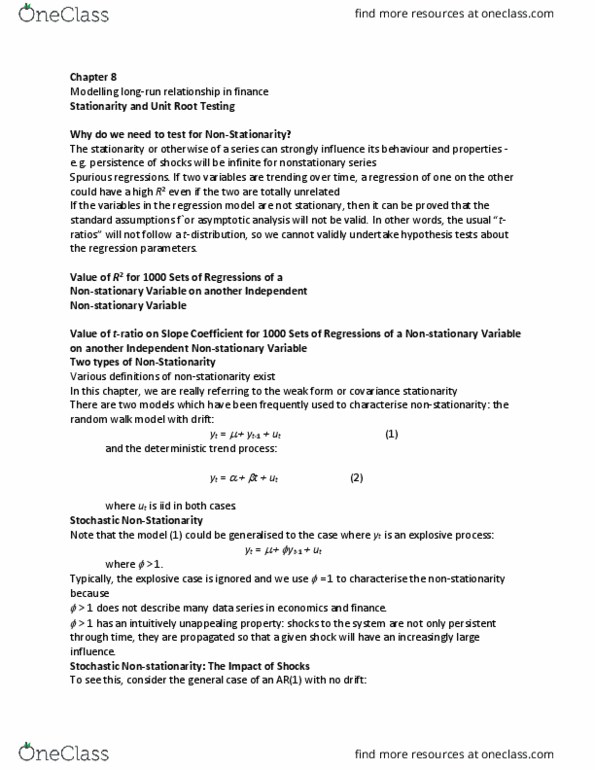

A random walk and a random walk with drift. Autoregressive processes with differing values of (0, 0. 8, 1) Consider again the simplest stochastic trend model: or yt. We can generalise this concept to consider the case where the series contains more than one unit root . That is, we would need to apply the first difference operator, , more than once to induce stationarity. If a non-stationary series, yt must be differenced d times before it becomes stationary, then it is said to be integrated of order d. we write yt i(d). So if yt i(d) then dyt i(0). An i(1) series contains one unit root, e. g. yt = yt-1 + ut. An i(2) series contains two unit roots and so would require differencing twice to induce stationarity. I(1) and i(2) series can wander a long way from their mean value and cross this mean value rarely.