PHYS 1061 Study Guide - Quiz Guide: Asymptotic Analysis, Independent And Identically Distributed Random Variables

Document Summary

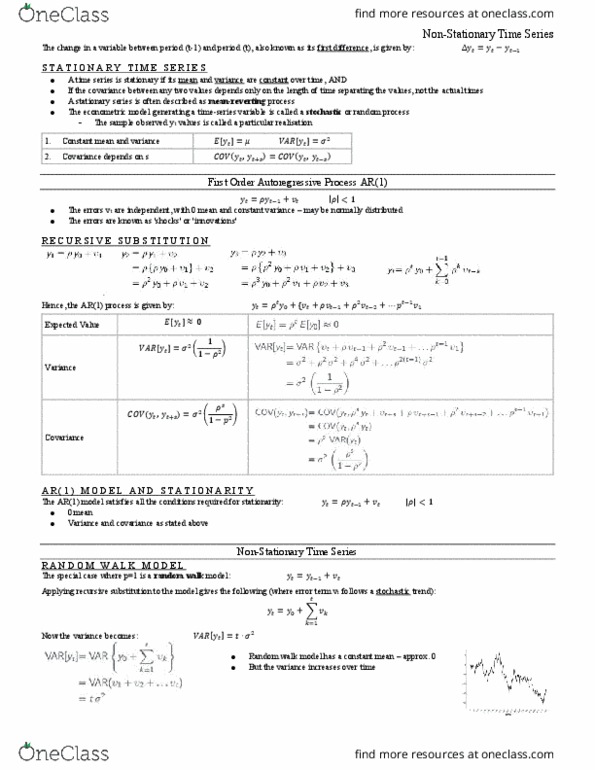

The stationarity or otherwise of a series can strongly influence its behaviour and properties - e. g. persistence of shocks will be infinite for nonstationary series. If two variables are trending over time, a regression of one on the other could have a high r2 even if the two are totally unrelated. If the variables in the regression model are not stationary, then it can be proved that the standard assumptions for asymptotic analysis will not be valid. T-ratios will not follow a t-distribution, so we cannot validly undertake hypothesis tests about the regression parameters. Value of r2 for 1000 sets of regressions of a. Value of t-ratio on slope coefficient for 1000 sets of regressions of a non-stationary. In this chapter, we are really referring to the weak form or covariance stationarity. Note that the model (1) could be generalised to the case where yt is an explosive process: yt = + yt-1 + ut where > 1.