BUS-F 446 Study Guide - Midterm Guide: Wrinkle, Weighted Arithmetic Mean, Interest Rate Risk

Document Summary

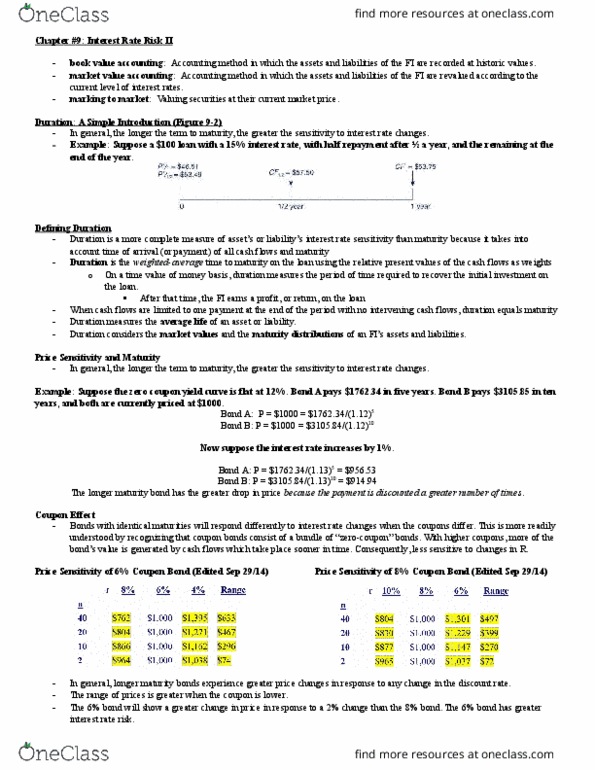

Chapter 9, interest rate risk ii the duration model, immunization. The duration model is more precise than the maturity model, and considers multiple factors. Generalization of interest rate risk: increased maturity more sensitivity, decreased coupon more sensitivity, duration: package used to describe 3 different factors: Measures effective time sensitivity and interest rate sensitivity. Formula on pages 229-230 is a sum of the pv of each bond piece, and it is the pv of each bond times t . One wrinkle in the formula is that we assume annual interest payment per year, but most bonds have 2. This means we must use formula #2 on page 230 to double the periods and halve the interest rates. However, for the purposes of this class, most bonds will be one year. How price changes when i% changes, is a convex curve. The slope of the tangent to this curve is essentially the duration.