ENT 210 Study Guide - Quiz Guide: Legal Personality, Accounts Payable, Net Income

Document Summary

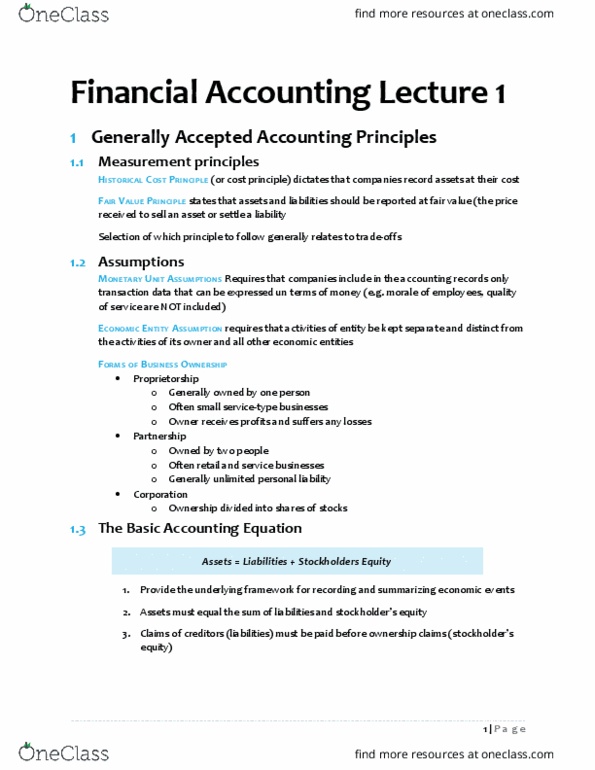

Proprietorship: owned by one person, small service-type business, personally liable. Partnership: owned by 2+ persons, retail and service-type businesses, unlimited personal liability, partnership agreement. Corporation: ownership divided into shares of stock, separate legal entity organized under state corporation law, limited liability. Creditors - party to whom money is owed. Common stock and retained earnings (stays in business) Companies record assets at their cost: fair value principle. Assets and liabilities should be reported at fair value. The price received to sell asset/settle a liability. Record only transaction data that can be expressed in terms of money: economic entity. Activities of the entity are kept separate from the activities of its owner and all other economic entities. Double-entry accounting system: each transaction must affect two or more different accounts, recording done by debiting at least one account and crediting another, debits must equal credits. If debits are greater than credits, the account will have a debit balance.