EC249 Study Guide - Final Guide: Currency Swap, Foreign Exchange Risk, Interest Rate Risk

Document Summary

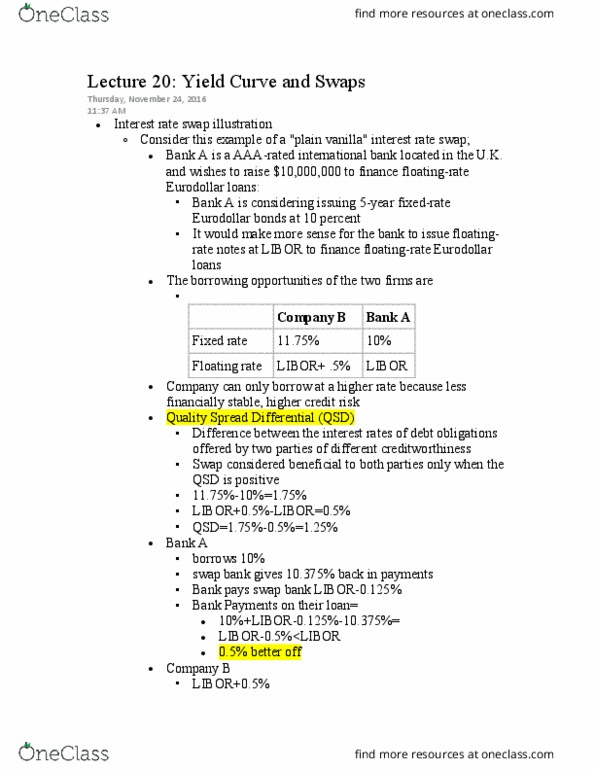

Ec249 ch 10 interest rate and currency swaps. Interest rate swaps (single and cross-currency) are widely used techniques for hedging long-term interest rate risk and foreign exchange risk. In a swap, two counterparties agree to a contractual arrangement wherein they agree to exchange cash flows at periodic intervals. Two types of interest rate swaps: single currency interest rate swap interest rate swap. One counterparty exchanges the interest payments of a floating-rate debt obligation for the fixed-rate interest payments of the other counterparty: cross-currency interest rate swap currency swap. Currency swap fixed for fixed rate debt service in two (or more) currencies: 2 - size of the swap market. The most popular currencies are: us dollar, euro, japanese yen, british pound sterling, swiss franc, 3 - the swap bank. A swap bank is a generic term to describe a financial institution that facilitates swaps between counterparties (could be an international commercial bank, investment bank, merchant bank)