MGFC30H3 Study Guide - Midterm Guide: United States Treasury Security, Contango, Spot Contract

Document Summary

Get access

Related Documents

Related Questions

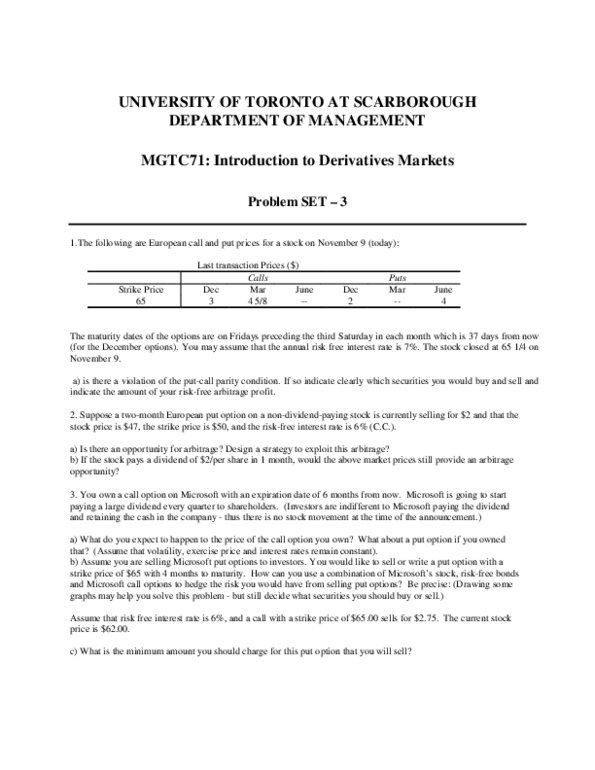

Just need the last two questions answered A and B at the bottom of the document

Youâre the chief financial officer (CFO) of Worldwide

Widget Manufacturing, Inc. The company manufactures and

sells widgets at factories in the United States and internationally.

Listed below are partial financial statements for Worldwide

Widget Manufacturing, Inc. Fill in the missing information in

each of the following financial statements. Answer spaces are

given below.

Worldwide Widget Manufacturing, Inc.

Balance Sheet as of December 31, 2015 and 2014

(in millions of dollars)

| 2015 | 2016 | 2015 | 2016 | ||

| Assets Current Assets: | Liabilities and Equity Current Liabilities: | ||||

| Cash and markatable securities | $427 | $322 | Accured wages and taxes | $309 | $257 |

| Accounts Receivable | a.? | 259 | Accounts payable | 381 | b.? |

| Inventory | 815 | 797 | Notes Payable | $492 | $421 |

| Total | $1,542 | $1,378 | Total | $1,182 | $997 |

| Fixed Assets: | Long-term debt: | $1,934 | c.? | ||

| Gross plant and equipment | d.? | $2,817 | Total | 3,116 | 2,956 |

| Less:depreciation | 368 | 254 | Stockholder's equity: | ||

| Net plant and equipment | $2,872 | $2,563 | Preferred stock ( 30 million shares) | $30 | $30 |

| Other long term assets | 521 | 487 | Common stock and paid in surplus (250 million shares) | 300 | e.? |

| Retained earnings | 1,489 | 1,142 | |||

| Total FA | f.? | $3,050 | Total Equity | $1,819 | $1,472 |

| Total Assets | $4,935 | $4,428 | Total liabilities and equity | $4,935 | $4,428 |

A. Accounts receivable for 2015_______300

B. Accounts payable for 2014_______319

C. Gross plant and equipment for 2015_______1959

D. Long-term debt for 2014_______3240

E. Common stock and paid-in surplus (250 million shares) for 2014_______300

F. Total FA for 2015_______3393

Worldwide Widget Manufacturing, Inc. Income Statement for Years Ending December 31, 2015 and 2014(in millions of dollars)

| 2015 | 2014 | |

| Net Sales | g. | $2018 |

| Less: Cost of Goods Sold | 753 | h.? |

| Gross Profits | $1,623 | $1,189 |

| Less: Other Operating Expense | 423 | 167 |

| Earnings before interest, taxes, depreciation, and amortization (EBITDA) | $1,200 | $1,022 |

| Less: Depreciation | 114 | 114 |

| Earning before interest and taxes (EBIT) | $1,086 | $908 |

| Less: Interest | i.? | 128 |

| Earnings:before Taxes (EBT) | $949 | $780 |

| Less:Taxes | j.? | 23 |

| Net Income | $664 | $546 |

| Less:Preferred stock dividends | 98 | 98 |

| Net income available to common stock holders | $566 | $448 |

| Less:Common stock dividends | 219 | 199 |

| Addition to retained earnings Per common share data: | $347 | $249 |

| Earnings per share (EPS) | k.? | $1.79 |

| Dividends per share (DPS) | $0.88 | l. ? |

| Book Value per share (BVPS) | m.? | $5.77 |

| Market Value per share (MVPS) | $23.97 | $22.47 |

g. Net sales for 2015_______2376

h. Less: Cost of goods sold for 2014_______829

i. Less: Interest for 2015_______137

j. Less: Taxes for 2015_______285

k. Earnings per share (EPS) for 2015_______1.88

l. Dividends per share (DPS) for 2014_______.73

m. Book value per share (BVPS) for 2015_______7.16

Worldwide Widget Manufacturing, Inc.

Statement of Cash Flows for Year Ending December 31, 2015

(in millions of dollars)â

| Section A: Cash Flows from operating activities | |

| Net Income | n.? |

| Additions (source of cash): Depreciation | 114 |

| Increase in accrued wages and taxes | o.? |

| Increase in accounts payable | 62 |

| Subtractions (use of cash): Increase in accounts receivable | -41 |

| Increase in inventory | p.? |

| Net Cash flow from operating activities | q.? |

| Section B: Cash Flows from investing activities subtractions: Increase in fixed assets | -$343 |

| Increase in other long-term assests | r.? |

| Net Cash flow from investing activities | s.? |

| Section C. Cash flows from financing activities Additions: Increase in notes payable | t.? |

| Increase in common and preferred stock | 0 |

| Subtractions: Decrease in long-term debt | -25 |

| Pay dividends | u.? |

| Net Cash flow from financing activities Section D. Net Change in cash and marketable securities | v.? $105 |

n. Net income_______664

o. Increase in accrued wages and taxes_______52

p. Increase in inventory_______18

q. Net cash flow from operating activities_______833

r. Increase in other long-term assets_______34

s. Net cash flow from investing activities_______-377

t. Increase in notes payable_______71

u. Pay dividends_______317

v. Net cash flow from financing activities_______-271

Worldwide Widget Manufacturing, Inc.

Statement of Retained Earnings as of December 31, 2015

(in millions of dollars)

| Balance of retained earnings, December 31,2014 | $1,142 | |

| Plus: Net income for 2015 | w.? | |

| Less: Cash dividends paid | 0 | 0 |

| Preferred stock | x.? | |

| Common Stock | 219 | |

| Total cash dividends paid | 317 | |

| Balance of retained earnings, December 31,2015 | $1,489 |

w. Plus: Net income for 2015 _______664

x. Preferred stock _______98

2. Youâll need to compare your companyâs ratios with the industryâs standards.

Worldwide Widget Manufacturing, Inc.

| Company | Industy | Comparison | |

| Current Ratio | 2.2 times | ||

| Quick Ratio | 1.1 times | ||

| Cash Ratio | 0.35 times | ||

| Inventory turnover | 2 times or 1 time | ||

| Days' sales in inventory | 135 days or 335 days | ||

| Average payment period | 110 days | ||

| Sales to working capital | 3 times | ||

| Total asset turnover | 0.6 times | ||

| Debt-to equity | 1.1 times | ||

| Profit margin | 16.5% | ||

| Gross profit margin | 48.13% | ||

| ROA | 8.78% | ||

| ROE | 19.45% | ||

| Divident payout | 32% |

A. Use the information found in Worldwide Widget Manufacturingâs financial statements

to calculate all of the listed financial ratios in the above table for your

company. Then, for each ratio, provide a comparison of the companyâs result

with the industry standards, indicating if your companyâs results are lower than,

higher than, slower than, or faster than the industry standards.

B. Calculate your companyâs internal and sustainable growth rates.

| E13-5 Matching Each Ratio with Its Computational Formula LO 13-4, 13-5, 13-6, 13-7 | |||||||

| Match each definition with its related ratios or percentages by selecting the appropriate letter in the drop down provided. | |||||||

| Definitions: | Ratios or Percentages | Definitions | |||||

| A. | Net Income (before extraordinary items) ÷ Net Sales | 1 | Profit margin | ||||

| B. | Days in Year ÷ Receivable Turnover ratio | 2 | Inventory turnover ratio | ||||

| C. | Net Income ÷ Average Stockholdersâ Equity | 3 | Average collection period | ||||

| D. | Net Income ÷ Average Number of Shares of Common Stock Outstanding | 4 | Dividend yield ratio | ||||

| E. | Return on Equity â Return on Assets | 5 | Return on equity | ||||

| F. | Quick Assets ÷ Current Liabilities | 6 | Current ratio | ||||

| G. | Current Assets ÷ Current Liabilities | 7 | Debt-to-equity ratio | ||||

| H. | Cost of Goods Sold ÷ Average Inventory | 8 | Price/earnings ratio | ||||

| I. | Net Credit Sales ÷ Average Net Receivables | 9 | Financial leverage percentage | E | |||

| J. | Days in Year ÷ Inventory Turnover Ratio | 10 | Receivable turnover ratio | ||||

| K. | Total Liabilities ÷ Stockholdersâ Equity | 11 | Average daysâ supply of inventory | ||||

| L. | Dividends per Share ÷ Market Price per Share | 12 | Earnings per share | ||||

| M. | Market Price per Share ÷ Earnings per Share | 13 | Return on assets | ||||

| N. | [Net Income + Interest Expense (net of tax)] ÷ Average Total Assets | 14 | Quick ratio | ||||

| O. | Cash from Operating Activities (before interest and taxes) ÷ Interest Paid | 15 | Times interest earned | ||||

| P. | Net Sales Revenue ÷ Net Fixed Assets | 16 | Cash coverage ratio | ||||

| Q. | (Net Income + Interest Expense + Income Tax Expense) ÷ Interest Expense | 17 | Fixed asset turnover ratio | ||||